Team-BHP

(

https://www.team-bhp.com/forum/)

There are many questions which come up when you are planning on buying a car. You test drive many cars, ask for a lot of opinions and decide the car which you find to be most suitable for your needs and your budget.

And when you are just about to go ahead with the well managed purchase, you see another car passing by, and all of a sudden, all the preparations go for a toss. Your heart skips a beat, you go and have a test drive of that car, you love it, your heart craves for it - and then you see the price!

You want it badly, but it is just beyond your current budget. You can no longer do a cash down purchase and start thinking about a loan!

And the question changes from WHICH CAR to WHICH LOAN?

I am enjoying the advantage of this scheme, so would like to share it with all of you.

This is FOR you if : - You are ready to wait a period of atleast 15 days for the loan to be processed.

- You are ready to deal with bank officials who might not know that there is a scheme called as the Advantage Car Loan available (among many other things)

- You are ready for a bit of efforts initially (only initially - once the loan is approved, it's a cakewalk)

- You are eligible to get a loan upto more than 5 lakhs.

- You are ready to take a loan more than 5 lakhs! (This scheme is applicable only for loans above Rs. 5 lakhs)

- You are sure that you will be able to cover the loan amount in about 2 years. (You don't actually have to pay it back - you just need to put the money in a bank account - accessible to you at all times). This is best for those who are planning an all cash purchase or are planning to plonk down a big downpayment

This is NOT for you if : - You have other ongoing loans and you may not be eligible for the loan.

- You plan on paying the EMI and continue the loan for the full or majority tenure.

- You are prone to HUGE impulsive purchases and may not be able to maintain a certain amount of balance in your account (This will be more clear when you read the rest of the post)

So now that you have decided to read it further, here goes!

The Scheme :

For those of you who know

SBI MaxGain Home Loans, this is the same thing for Car Loans. For those who don't read on!

The

SBI Advantage Car Loan is a Loan Scheme that has an

Over Draft (

OD) account linked to the loan account. If you have understood this statement, you are probably on your way to the Bank - if not, well, read on!

Normally, when you opt for a loan, you get a fixed / floating (most probably floating) interest rate. In the tenure of the loan, if the interest rate rises, either the

tenure or your

EMI increases - in the end,

the total amount of money that you pay to the bank increases!

Also, the

EMI that is paid consists of a

principal component and an

interest component. As per the amortization schedule given by the bank, you will see that the

bank tries to recover the majority part of the interest as soon as possible - this is achieved by contributing a majority percentage of your EMI towards your interest and a lesser part towards the principal.

You may ask as to how this will matter - well, in case of fixed interest rate, it does not matter - the total payable interest will remain same, but in the case of floating interest, it can kill you!! As the majority part of the EMI goes towards interest, the re-payable principal component still remains large.

Now, if the interest rate rises (which it does every few months), the interest becomes applicable on the remaining principal (which is still quite large due to the

biased amortization schedule), hence, the

tenure or

EMI rises. For large loans with big tenures, this becomes a nightmare as the cycle continues and you see that you end up paying 3-4 times the interest of the principal amount (and more than double that of the anticipated amount)

To avoid this most of us go in for a

pre-payment option, wherein we make a downpayment of a substantial amount about once or twice per year. As this pre-payment amount is directly deducted from the principal, your tenure gets reduced, hence the total payable interest too.

So for a loan, we agree upon the following

facts :

- For floating interest, longer the tenure, greater the chance of increase in interest, hence greater the risk of increase in EMI/tenure.

- Regular pre-payments beyond the EMI amount will help to cover the loan amount sooner.

- It is most beneficial to foreclose the loan as soon as possible.

The corollary :

Making pre-payments means normally

adjusting finances,

scrounging, holding back on your wishes and always worrying about what to do if you

suddenly require a chunk of money! There is

loss of liquidity and generally raises the levels of stress as well.

Now you would be wondering why I am boring you with the obvious - well that's because, after telling the obvious, I intend to ask you :

What if there is an option wherein you can

control your interest rate, make

pre-payments,

not worry about the increases in tenure and

EMI, pay

much lesser interest, and at the same time

NOT LOSE LIQUIDITY ??

Sounds incredible, almost unbelievable, but yes, there is such a magic bullet and it is called as an

Overdraft linked loan account.

Normally, when you avail of a loan, the bank opens a normal loan account in your name. That account is a bottomless pit, i.e. whatever money you put into into it never comes out again.

Whenever you pay your EMI, a part of it gets paid to this account and another part to the Bank's interest account. When you make a prepayment, the entire amount goes into your loan account. Once the money goes into the loan account, you cannot withdraw it. Interest is applicable on the balance amount (Loan amount - total paid amount till date).

Now, consider such a loan account, with the only difference that you can withdraw money as well. Such an account is implemented by creating an Overdraft loan account.

Example :

You take a loan of Rs. 600000 (Six lakh rupees). An overdraft account is created with an

initial negative balance, i.e

-600000. Interest is made applicable on the

remaining negative amount. Once the balance becomes

zero or greater,

no interest is applicable.

The best part : You can deposit as much money as you want, whenever you want in that account (like a normal current account), and you can also

WITHDRAW money from that account as long as the balance does not go below -600000! The interest is calculated

only on the negative component.

So :

If you deposit 600000 in the account on day 1, your balance = -600000 + 600000 = 0. Hence interest = 0.

If you deposit 300000 in the account on day 1, your balance = -600000 + 300000 = -300000. Interest is applicable only on Rs.300000 (i.e.

half the interest rate!)

The best part : You can withdraw the money any time you want. As long as the money is there in the account, you will pay interest only for the balance amount. If you are in sudden need of money, you can

withdraw the

ENTIRE amount - you can then deposit it (or a part) back once your needs are fulfilled and the interest will be applicable for that amount for the amount of time you have used the money!

This scheme is available for Housing Loan with SBI, ICICI and Standard Chartered as far as my knowledge goes.

BUT, FOR CARS, ONLY SBI GIVES THIS OPTION, AND NOT MANY (EVEN FROM THE BANK) ARE AWARE OF THIS!!

So, you get the best of both worlds :

- You can avail a larger loan

- You can avail the loan for a much longer tenure

- You can control the total amount of interest you will pay

- You can remain agnostic of the interest rate

- You can make pre-payments without losing liquidity

- You balance the bias caused by the amortization schedule

- You lead a happy stressful life as you do not have to think about buying a diamond for your wife on her birthday (just because you have to make a prepayment) ;)

- And the best - you get the new car you have always wanted, without having to adjust on other fronts.

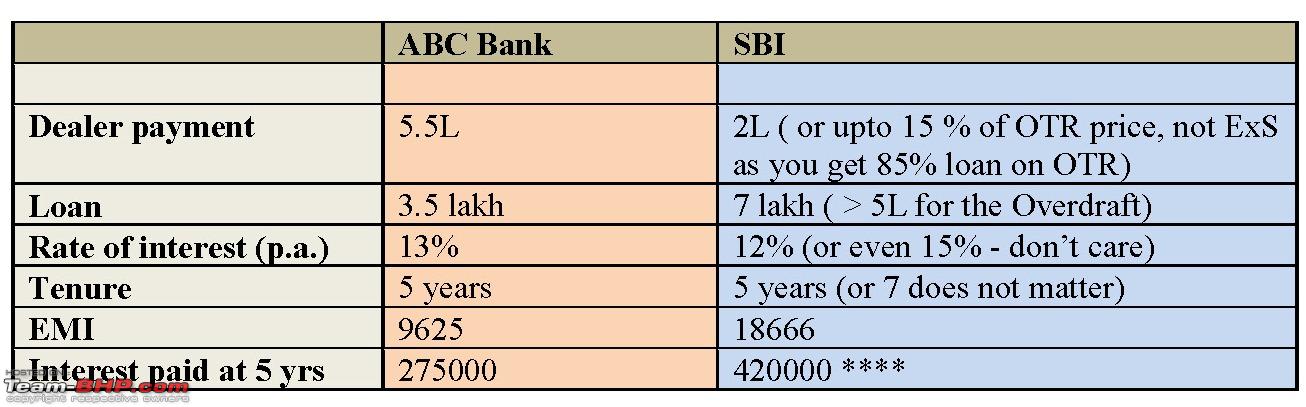

Here is a small scenario. Assume that you want to buy a car of around 9 lakh. Also assume that you have cash of 5.5 lakh with you.

You have 2 cases

- you take a minimal loan and pay the entire 5.5L to the dealer

OR- you take a maximum loan (SBI Advantage Loan)

Till here, this sounds pretty straightforward - a no brainer. There is no point in going for

SBI. ABC Bank sounds better.

But now comes in the Advantage (

OD linked car loan).

You had

5.5L in hand. You have

3.5L left with you since you paid only 2L initially.

Put this in the Overdraft account the very day you get the disbursement.

So on day one, you are overdrawn by 7 - 3.5 =

3.5L only.

So, the interest is now applied only on

3.5L for 5 years.

Interest at the end of 5 yrs becomes

210000 (

less than ABC Bank).

But - EMI remains same (double of ABC bank) – that does not change.

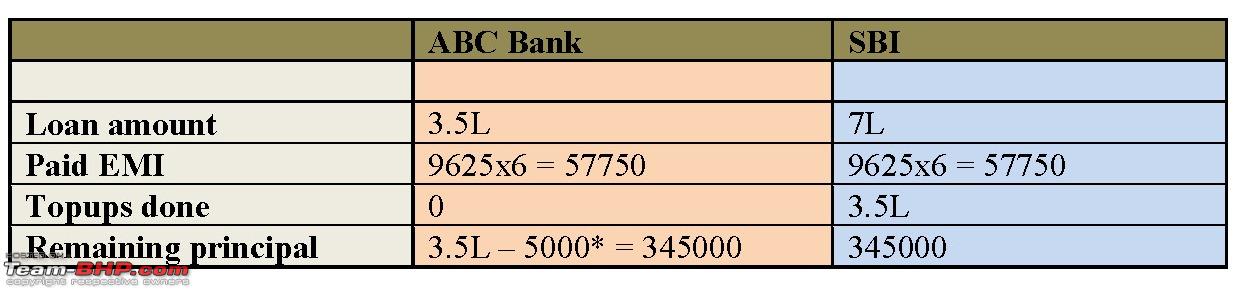

So where is the fun? Watch this :

You paid

3.5L on day 1.

Say on the 10th of every month, you have to pay

18666 to the bank. This will get debited from your account (say ICICI Bank or any other) and get credited to your SBI account.

Say you want to pay only

9625 as EMI (same as ABC Bank). So all you have to do is

transfer 9000 every month from your SBI account to your ICICI Bank account (opening another SBI instead account is recommended).This is possible because of the

OD account -

it is debitable like a normal current account - your

regular loan accounts are

NOT debitable!

So now at the end of 6 months this is the picture :

* As per your amortization schedule, for the first part, most of the EMI will go to interest recovery. So 5000 mentioned here as the principal component of the EMI is very very optimistic. It could be lesser.

In case of the OD account, as you have already paid a heap, the interest component reduces. We will still keep it same as ABC Bank to give credit.

Note that whatever topups you do to the OD directly deduct the principal, not the interest.

As you go on reducing the overdraft, the EMI component also contributes more to the principal.

The fun starts after this.

Let’s say that you have saved enough money till now and add in another lakh. The principal amount drops by another lakh.

Interest rate drops more. In the extreme case, if you put in

all the money on day one itself, you are getting the loan at

0% interest for 5 or 7 years!!!

Now, lets see the

advantage of liquidity

Lets say that one year down the line, you have paid (rather deposited) about

5 lakhs into the account. Moreover, your EMI is also resulting in more contribution to the principal.

At this point, you decide to get your car modded and buy a new LCD 56” TV. This sets you back by

1.5L. All you do is take this money out of your OD account! (or let’s say that your wife or your dad needs the money )

The balance now becomes

3.5. Interest rate increases a bit (but remember, the

EMIs you paid have already contributed to principal,

as against in ABC Bank where they are still majorly contributing to the interest) So for 3-4 months, you just pay a bit more interest and they replenish the money.

What would have happened if you had taken the ABC bank option :

If you take the ABC Bank option, the

5.5L you paid to the dealer are gone – you can’t use them. (

loss of liquidity)

If you make any pre-payment (usually at 2% fee, but lets assume its free), that money is also gone – you can’t use it. (

loss of liquidity)

Now, a step further in planning. Let’s say that you put all your salary in the OD account (and maybe your wife’s too). In a year, you have put 7L in. Now you need to route the entire EMI back to your account (as EMI still remains same). But your interest is 0.

You have 7L in your account to use at your own disposal for the rest 4 or 6 years (Though the available limit also goes on dropping proportionally as per the principal component in the amortization schedule). You have hardly paid any interest!!

This scheme is good for people who can invest well and use the overdraft wisely. If you use it like a normal loan account, and don’t do the topups fast, it turns out to be more expensive. Done wisely, you can get a larger loan amount for a larger tenure.

As we aim at topping it up in 1 – 2 years,

even if the interest rate is 20% and the

tenure is 10 years, you still pay the same amount of interest –which is

minuscule!

This is just brilliant! For someone like me who's pathetic with numbers (I still find myself using my fingers to count sometimes!!) it was so easy to understand what you're trying to tell. Thanks for taking the trouble to explain in great detail!

Quote:

Originally Posted by fash_1

(Post 2530850)

This is just brilliant! For someone like me who's pathetic with numbers (I still find myself using my fingers to count sometimes!!) it was so easy to understand what you're trying to tell. Thanks for taking the trouble to explain in great detail!

|

Thanks! We (me and my family) are reaping tonnes of benefits of this scheme, so felt I should share!

@Keyur

Not sure about the calculations you have mentioned.

1. EMI for Loan of 3.5 Lakh @ 13% for 5 years would be 7,964 (and not 9,625)

2. Total principle paid in first 6 months would be 25,719 (and not 5,000)

3. You calculations do not "accumulate" the interest amount for OD scenerio. You are using simple interest formula. However, in this loan interest is calculated daily and accumulated monthly (debited to OD account).

To compare these two loans, you need to:

1. Start with same principle amount

2. Same tenure

3. Same ROI (though ROI is 0.5% higher in case of OD loans like the one you mentioned)

And then assume same amount of pre-payment at same time interval. That would give you actual cost and benefit of these loans.

Suppose a loan is taken under this scheme for an amount of 7 lacs, and the on the same day, 7 lacs is deposited into the account, should the same EMI be paid every month?

In that case, at the end of the loan period, the amount that has been paid to the bank would be 7lac (initial deposit) + EMI x No of months.

so at the end of the loan period, the initial 7 lacs + the interest paid in EMI's can be withdrawn?

If you deposit 7 lakh next day, interest debits would stop. So, you can stop the EMI (actually standing payment instructions) too.

That is the advantage of this scheme.

Pros:

1. Flexibility, you can pay anytime you want

2. Liquidity as mentioned by OP

Cons:

1. Higher Interest rate

2. Reported as "Overdraft" to CIBIL, (other loans are reported as "Line of Credit")

@Keyur,

Thanks for the detailed information:thumbs up. I have a SBI Maxgain OD account taken for a homeloan and hence fully aware of the positives of the scheme. Till now I have been able to repay back using the OD option thereby reducing my loan tenure from 15 yrs to 4 years in 2 years of availing loan. Good that SBI has come out with a similar scheme for the car loans too. I am sure the benefits would appeal to car buyers. :)

Quote:

Originally Posted by Abes

(Post 2531261)

Suppose a loan is taken under this scheme for an amount of 7 lacs, and the on the same day, 7 lacs is deposited into the account, should the same EMI be paid every month?

|

Whats the fun in that, why take a loan then if you already have the amount?

Thanks for bringing this up.

But you know what? With car loans at around 12% and gold jewellery mortgage loans at 14% and almost no hassle involved in the processing or prepayment IMHO is it worth to spend so much effort on car loans?

And here's a trivia which is quite shocking, ppl are buying cars through agriculture loans at 7% interest!!unethical obviously but beat that!

Quote:

Originally Posted by NetfreakBombay

(Post 2531229)

@Keyur

Not sure about the calculations you have mentioned.

|

I had actually done all the calculations with the reducing interest and exact values. But it becomes too complicated for a layman to understand or grasp. The point of the illustration was to give an idea that by making the right payments, you can have your OWN ROI - irrespective of whether the actual ROI is 0.5% or 5% higher!

Quote:

Originally Posted by Abes

(Post 2531261)

Suppose a loan is taken under this scheme for an amount of 7 lacs, and the on the same day, 7 lacs is deposited into the account, should the same EMI be paid every month?

In that case, at the end of the loan period, the amount that has been paid to the bank would be 7lac (initial deposit) + EMI x No of months.

so at the end of the loan period, the initial 7 lacs + the interest paid in EMI's can be withdrawn?

|

The moment 7 lacs is deposited on the same day, your applicable interest becomes 0. So all your EMI gets added to the account

That is why I have mentioned about scheduling monthly transfers from your OD account to your savings account.

Say you pay your EMI on the 10th. You can have standing instructions to transfer the entire EMI amount back to your savings / salary account (via NEFT if other bank's account) on the 12th itself.

There is no point in keeping any more balance in the account after zeroing it off as you will not get any interest for the money.

Quote:

Originally Posted by ghodlur

(Post 2531350)

@Keyur,

Thanks for the detailed information  .

|

Glad to be of help

Quote:

Originally Posted by ghodlur

(Post 2531350)

@Keyur,

Whats the fun in that, why take a loan then if you already have the amount?

|

There is a

LOT of fun in that!

If you have 7 lacs today and you directly pay it to the dealer, you lose all the money now itself. Tomorrow, if you need 5 lacs urgently, you might not have it! (

Loss of liquidity)

By taking the loan for say 5 years, and depositing the 7 lac in-hand cash in the account the same day you get :

- The Bank pays the dealer, not you

- Your money (7 lacs) is sitting safe in your account for years, so you have that liquidity for 5 years (reducing as per the principal component of the amortization schedule)

- You get the loan at 0% interest

You MUST take this loan if you have more than 50% of the cash required.

Also, if you have about 10 lac available now (in-hand), you will think about plonking 7 lacs on a car (as the remaining 3 lacs may not be enough liquidity in today's world). But with this scheme, you can happily spend that much on a car!

Quote:

Originally Posted by kiku007

(Post 2531434)

Thanks for bringing this up.

But you know what? With car loans at around 12% and gold jewellery mortgage loans at 14% and almost no hassle involved in the processing or prepayment IMHO is it worth to spend so much effort on car loans?

|

If you invest correctly in the OD account with regular top ups, your actual interest rate over 5 years will turn out to be hardly1-2% (even lesser) or max at around 5%! It is waaaay better than a gold loan!

Quote:

Originally Posted by keyur

(Post 2531528)

There is a LOT of fun in that!

If you have 7 lacs today and you directly pay it to the dealer, you lose all the money now itself. Tomorrow, if you need 5 lacs urgently, you might not have it! (Loss of liquidity)

|

@keyur,

Agreed to your points regarding the adv of taking loan, but I was referring to @Abes post when one takes a loan and deposits the loan amount the same day or say within a week in the OD account. What benefit does this have?

The benefits of OD account can be realized if the loan is taken for atleast an year or more when you dont have the cash but are sure the flow will begin at a later date.

Quote:

Originally Posted by ghodlur

(Post 2531536)

@keyur,

What benefit does this have?

|

That is precisely what I was trying to explain above.

Let me try differently.

"The benefits of OD account can be realized if the loan is taken for atleast an year or more when you dont have the cash but are sure the flow will begin at a later date."

Here, we are

not talking about

foreclosing the loan. We keep the loan for the

FULL tenure, but top it up as soon as possible.

So, the sooner we top it up, lesser the interest we have to pay. Depositing all the money on day one is that case.

We just top up that money (instead of paying it to the dealer) on day one itself. But we keep the loan alive for 5 years.

So, instead of you losing the 7 lacs from your pocket, you put the 7 lacs in your other pocket (from your savings bank to your SBI Loan OD account). By doing so, SBI pays the dealer, and at the same time you get to use 7 lacs for 5 years at 0% interest!!

(or atleast the amount that remains after deduction of the principal components as per the amortization schedule)

At the end of 5 years, the 7 lac will get paid to the bank and the loan will get closed, but that is much better than :

1. paying 7 lac upfront today

2. paying 7 lac + 3.5 lac = 10 lac (at 10% pa for 5 years) at the end of 5 years

Quote:

Originally Posted by keyur

(Post 2531528)

I had actually done all the calculations with the reducing interest and exact values. But it becomes too complicated for a layman to understand or grasp.

|

With this your calculations are completely off the mark. E.g. 5k principle instead of 25k.

To compare benefits, its okay to round off, but numbers should still be reasonable.

Quote:

Originally Posted by NetfreakBombay

(Post 2531645)

With this your calculations are completely off the mark. E.g. 5k principle instead of 25k.

|

The 5K was not by my calculation - it was by the amortization schedule given to a friend of mine when he tried to get a car loan for 5 years from a known bank! In the first year, only about 5 or 6 k was going towards the principal, and the rest towards interest.

| All times are GMT +5.5. The time now is 10:30. | |