Team-BHP

(

https://www.team-bhp.com/forum/)

Customer to a Teaseller: How much the tea costs?

Tea seller: Rs 10 per cup.

C: and how much for the cookie?

T: Rs 5 each.

C: Ok, Give me a tea and a cookie.

T: That makes 20Rs.

C: How come?

T: 15 for tea and 5 for cookie.

C: But tea is for 10?

T: No, if you buy a cookie also, the tea is Rs 15.

C: What? That means the cookie costs me 10Rs.

T: No sir, the cookie is for Rs 5 only, if you buy a cookie, the tea is for 15rs.

C: Can i buy a tea and a cookie separately?

T: No sir, you can buy only the tea at 10rs but you can't buy a cookie without the tea which will then be at 15Rs.

This logic is beyond my comprehension but this is exactly what TATA AIG is doing.

I need to renew insurance for my car which is currently insured by TATA-AIG. I was looking online for the renewal quotes and this is what i found on TATA AIG official website.

www.tataaig.com

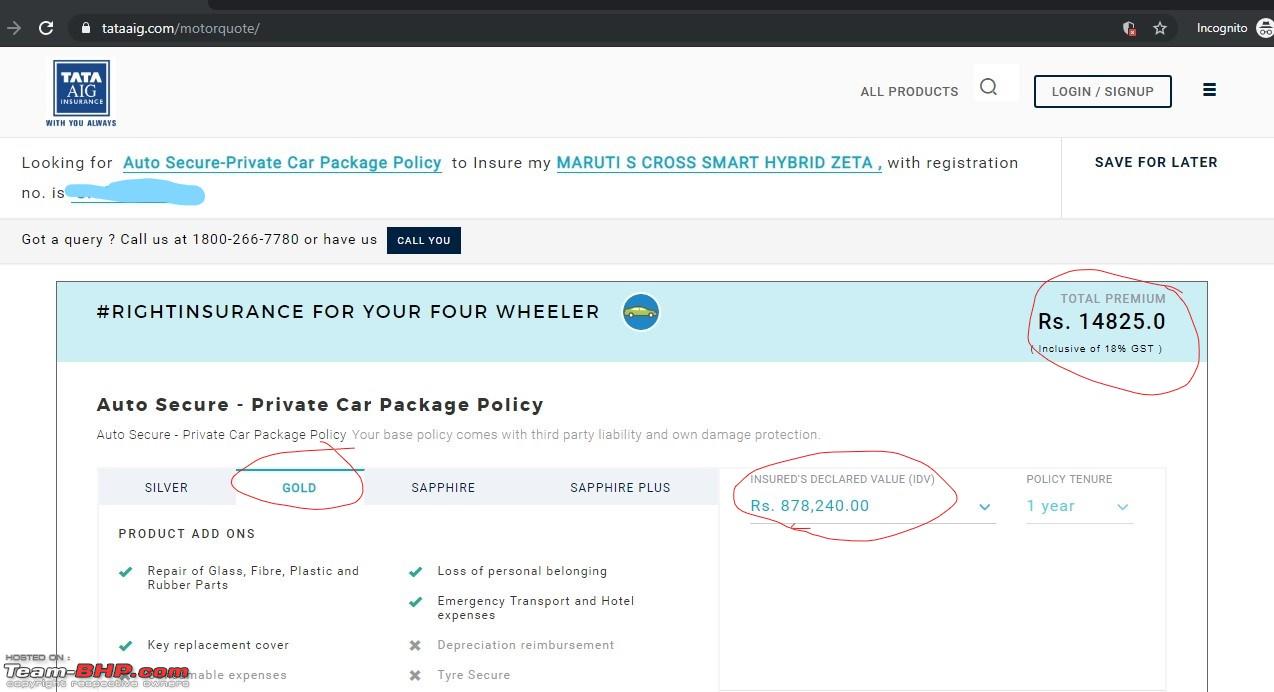

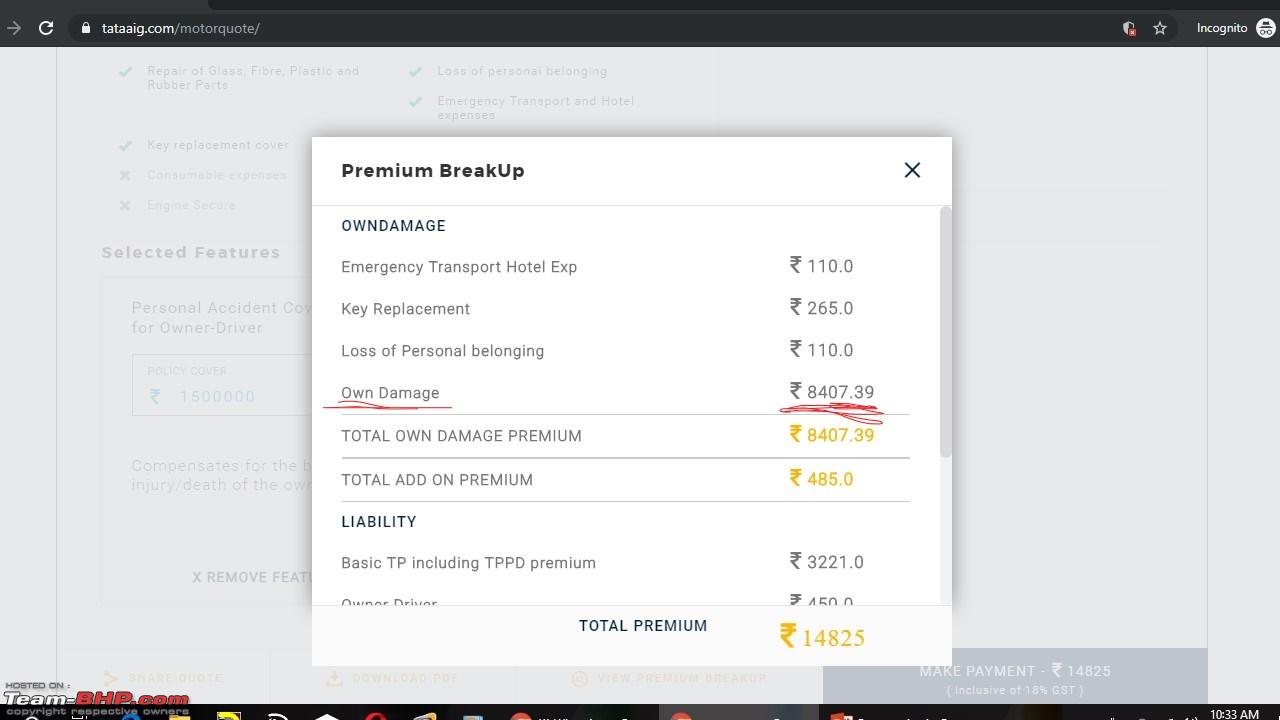

For all things the same at same IDV , when you choose Gold plan without any significant add-ons the quote comes to Rs 14825. The premium breakup for this shows the basic premium to be Rs 8407.

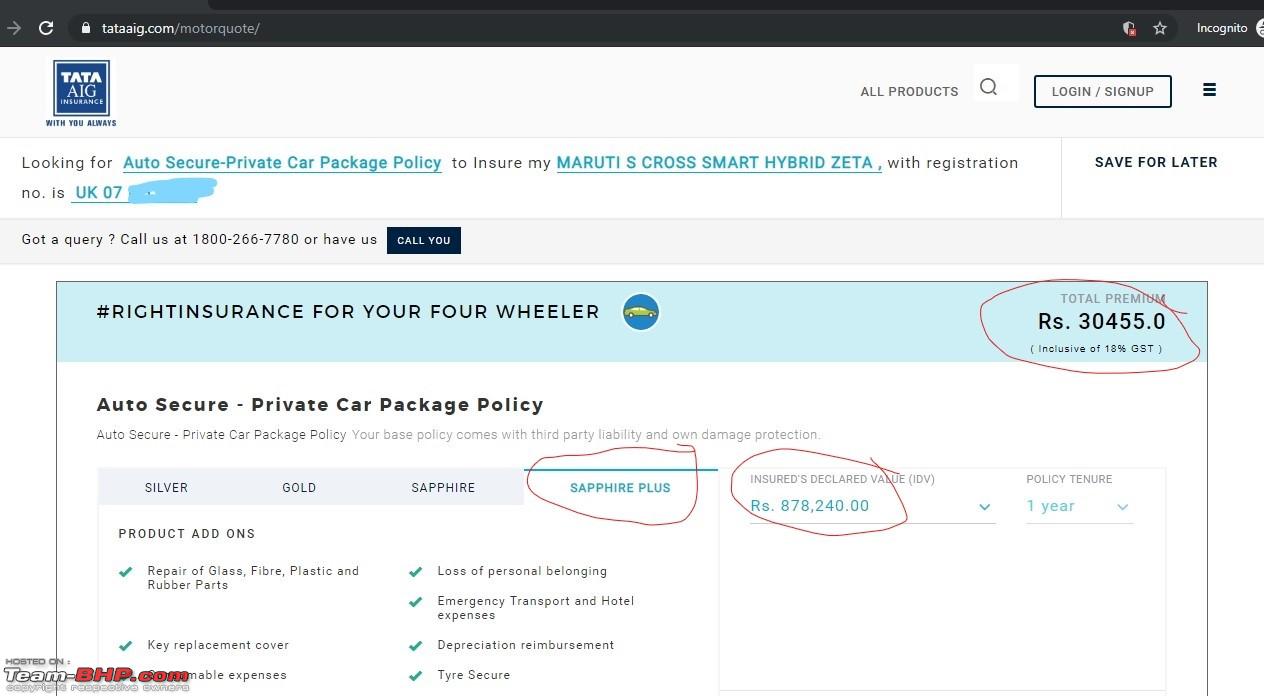

As soon as you add sapphire or sapphire plus plan, which includes various addons, the basic premium increases to 14012 and add-on premium is extra at 8125, The total premium reaching 30455.

When the addon is charged separately, how can it affect the basic own damage premium cost? They are effectively charging me approx 16000 for the add-ons which they claim to be priced at Rs. 8125. :Frustrati

Quote:

Originally Posted by car-dent

(Post 4640701)

When the addon is charged separately, how can it affect the basic own damage premium cost? They are effectively charging me approx 16000 for the add-ons which they claim to be priced at Rs. 8125. :Frustrati

|

Insurance business is tricky. What might be happening is that on the basic plan, the premium must have been discounted on the higher side, while on the other one, discounts on premium must have been low.

This happens when too much maths is done by the company. Someone must have told them claims from the basic plans are on the lower side (as the customer ends up paying Lot more from his pocket) compared to the all inclusive plans. Case in point the just the zero dep insurance vs zero dep + consumable cover + NCB loss cover will cost the insurance company a lot more.

When I was using Future Generalli insurance, my premium was discounted by over 80%. I'm pretty sure this figure would be lower on the higher plans.

What you can do is approach a different insurance provider. I'm sure there will be companies happy to take your business. :D

I think you can checkout other websites like policybazar,coverfox etc and from there you can see the details of the creakup when you find TATA-AIG. Maybe that might help you to understand things better. I myself have had issues with TATA AIG in the past and so strict nowadays stick to Bajaj Allianz and I am happy with it. Hope that you are able to get a clearer picture with that through other websites. Cheers :)

This is indeed a rip-off strategy from Tata AIG.

I faced the same conundrum with them when I tried to renew the insurance for my motorcycle from their website.

They were not ready to show zero dep option online; but were willing to do it over the phone via their customer care. They were also charging an increased ratio when in-fact I had a 25% NCB due to no claims in the past.

Finally gave my business to Universal Sompo as they offered zero dep + cashless (first for a normal non-premium motorcycle) at almost half the price quoted by Tata AIG for the same IDV.

The ratio of calculating the basic own damage premium is simple. As per IRDA, it is defined at 3.28% of the target IDV value (as explained by Royal Sundaram team). Insurance agents usually play around this value with their own discounts on this base value.

Any add-on covers are charged as a % of the base premium + expected claim ratio of that particular cover (this will vary for each insurer).

What I have observed is that the overall premiums are expensive in the order of insurers as below (i'm talking of full blown add-on covers):

ICICI Lombard > HDFC Ergo > Tata AIG > Bajaj Allianz > Other private insurers (all within relative margins) > Govt Insurers (like new india/ united india)

I have been using Royal Sundaram for all my car insurance needs since the past 4 years and they have one of the best coverage in the insurance market for cars. When I got my new car in March 2017 (Ford Ecosport Titanium); I paid a total of 31k for the following items:

1. Zero Dep

2. Return to Invoice

3. Lifetime Tax Cover

4. Key Protection

5. Windshield Protection

6. Engine & Gearbox Cover

My price for the same coverage of this year's renewal cost me 23k.

I have not been in an incident to make claims (*touchwood*) so far. And their yearly charges keep coming down by 3.5-4k every year. I have total peace of mind even with the worst case scenario.

A friend of mine who managed to make 4 large value claims (each > 75k) on his car (with similar coverage as mine) within 1 year of new car purchase was provided full coverage each time and he had to pay only around 1k each time. So, I now know that I am covered for similar risks as well.

Instead of worrying about hassles later; I would prefer to pay a marginally higher value upfront for total peace of mind later on.

Just shared mt 2 cents on this topic.

Cheers & Safe Driving

I have also ditched TATA AIG and have renewed my insurance with Royal Sundaram. they gave me a cheaper Deal by approx 5,000 Rs with similar IDV and similar/slightly better coverage. I just hope they provide a good service if ever needed.

Quote:

Originally Posted by Surya-TJet

(Post 4642802)

As per IRDA, it is defined at 3.28% of the target IDV value (as explained by Royal Sundaram team). Insurance agents usually play around this value with their own discounts on this base value.

|

+1 to this; for cars, I've seen the OD Basic vary from 1% to approx 3% of IDV in the same insurance company based on who issues the policy - the agent or the company direct.

| All times are GMT +5.5. The time now is 17:23. | |