| |||||||

| View Poll Results: Have you taken a car loan or gone the full down-payment way? | |||

| Full down-payment | | 304 | 38.19% |

| Couldn't buy without a loan | | 329 | 41.33% |

| Loan taken for any other reason | | 163 | 20.48% |

| Voters: 796. You may not vote on this poll | |||

|

| Search this Thread |  167,971 views |

13th April 2022, 09:21

13th April 2022, 09:21

| #151 |

| BHPian Join Date: Feb 2015 Location: Kochi

Posts: 50

Thanked: 136 Times

| |

|

| |

|

13th April 2022, 11:16

| #152 |

| Senior - BHPian | |

|

|

|

13th April 2022, 17:05

| #153 |

| BHPian Join Date: Jul 2010 Location: 12.97N, 77.59E

Posts: 845

Thanked: 2,289 Times

| |

|  (1)

Thanks (1)

Thanks

|

|

17th April 2022, 00:12

| #154 |

| Newbie Join Date: May 2013 Location: Mumbai

Posts: 2

Thanked: 2 Times

| |

|

| (2)

Thanks

|

|

13th September 2022, 22:47

| #155 |

| BHPian Join Date: Mar 2021 Location: Bangalore

Posts: 27

Thanked: 26 Times

| |

|

| (1)

Thanks

|

|

25th September 2022, 23:14

| #156 |

| BHPian Join Date: Aug 2014 Location: DEL, SFO

Posts: 901

Thanked: 2,838 Times

| |

|

|

|

26th September 2022, 08:14

| #157 |

| BANNED Join Date: Apr 2008 Location: Bangalore

Posts: 11,368

Thanked: 23,150 Times

Infractions: 0/2 (8) | |

|

|

|

26th September 2022, 11:52

| #158 |

| BHPian Join Date: Mar 2017 Location: Bangalore

Posts: 901

Thanked: 2,655 Times

| |

|

| (1)

Thanks

|

)

) |

26th September 2022, 11:57

| #159 |

| BHPian Join Date: Dec 2021 Location: Bangalore

Posts: 155

Thanked: 549 Times

| |

|

| (1)

Thanks

|

|

26th September 2022, 12:01

| #160 |

| BHPian Join Date: Jan 2009 Location: Bangalore

Posts: 138

Thanked: 35 Times

| |

|

| (1)

Thanks

|

|

19th January 2023, 14:28

| #161 |

| BHPian | |

|

| (9)

Thanks

|

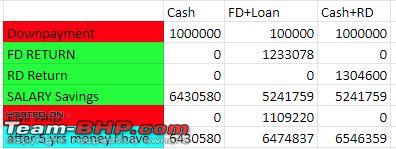

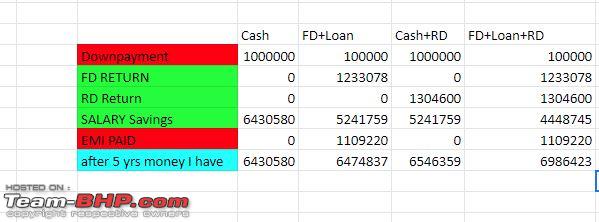

what do you guys say?

what do you guys say?| |

|

22nd January 2023, 14:15

| #162 |

| BHPian Join Date: Aug 2014 Location: DEL, SFO

Posts: 901

Thanked: 2,838 Times

| |

|

| (2)

Thanks

|

|

22nd January 2023, 18:36

| #163 |

| BHPian | |

|

| (3)

Thanks

|

|

22nd January 2023, 21:53

| #164 |

| BHPian Join Date: Apr 2021 Location: Mumbai

Posts: 245

Thanked: 1,222 Times

| |

|

| (1)

Thanks

|

|

23rd January 2023, 01:18

| #165 |

| BHPian Join Date: Feb 2021 Location: Pune

Posts: 68

Thanked: 119 Times

| |

|

| (8)

Thanks

|

|

Most Viewed