13th August 2008, 17:00

13th August 2008, 17:00

| #31 |

| Senior - BHPian Join Date: Jan 2008 Location: Bombay

Posts: 1,466

Thanked: 1,021 Times

| |

|

| |

|

13th August 2008, 20:51

| #32 |

| BHPian | |

|

|

|

14th August 2008, 19:26

| #33 |

| Senior - BHPian | |

|

but still would like to know. I just recieved a call from a Guy in Kotak mahindra and regarding the car loan i inquired about for Swift Vdi. he said the waiting period is 3 months but he can ge me that for a premium in a week. I was surprised and asked how come.

but still would like to know. I just recieved a call from a Guy in Kotak mahindra and regarding the car loan i inquired about for Swift Vdi. he said the waiting period is 3 months but he can ge me that for a premium in a week. I was surprised and asked how come. |

18th August 2008, 16:50

| #34 |

| Team-BHP Support  | |

|

|

|

6th October 2008, 22:09

| #35 |

| BHPian Join Date: Oct 2008 Location: Mumbai

Posts: 78

Thanked: 4 Times

| |

|

|

|

6th October 2008, 22:22

| #36 |

| Senior - BHPian Join Date: Dec 2007 Location: Bangalore

Posts: 4,106

Thanked: 537 Times

| |

|

|

|

6th October 2008, 22:22

| #37 |

| BHPian Join Date: Sep 2008 Location: Bavaria Germany

Posts: 190

Thanked: 8 Times

| |

|

|

|

6th October 2008, 22:27

| #38 |

| BHPian | |

|

|

|

6th October 2008, 22:44

| #39 |

| Senior - BHPian Join Date: Feb 2004 Location: DL XX XX XXXX

Posts: 1,634

Thanked: 1,011 Times

| |

|

|

|

6th October 2008, 22:46

| #40 |

| Senior - BHPian | |

|

|

|

6th October 2008, 23:37

| #41 |

| BHPian Join Date: Oct 2007 Location: Dubai

Posts: 53

Thanked: 2 Times

| |

|

|

| |

|

7th October 2008, 02:04

| #42 |

| Senior - BHPian Join Date: Feb 2004 Location: DL XX XX XXXX

Posts: 1,634

Thanked: 1,011 Times

| |

|

|

|

7th October 2008, 08:49

| #43 |

| Senior - BHPian | |

|

|

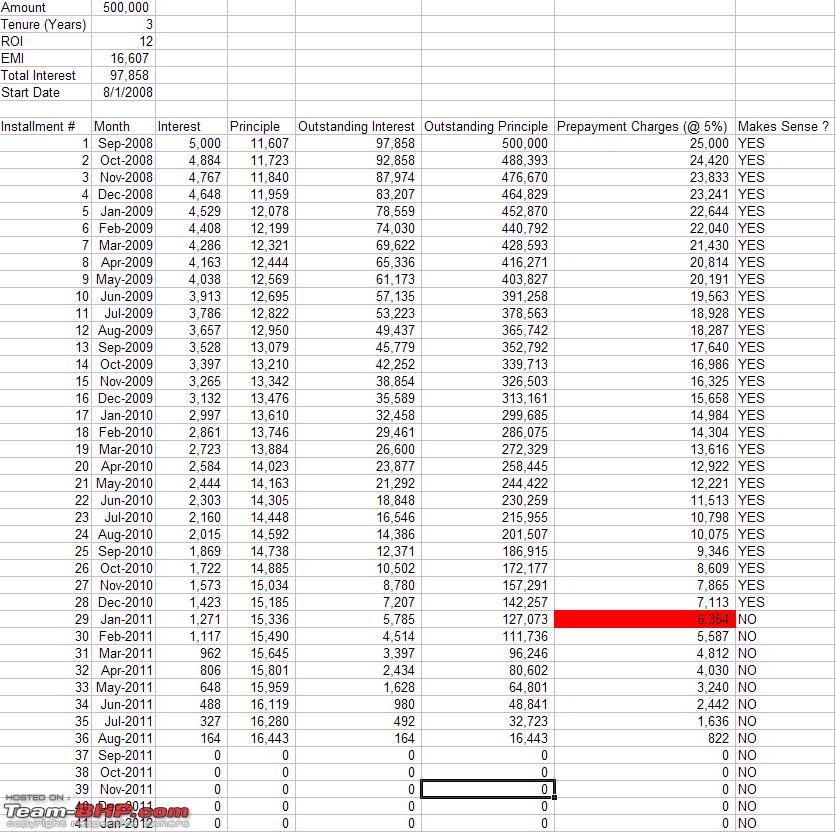

yes you read that right. If you close the loan with your own funds(meaning, not from another loan), there are no foreclosure charges. My love hate relationship with SBI continues. It is a case of losing a bit of self esteem and gaining in blood pressure to save some money !

yes you read that right. If you close the loan with your own funds(meaning, not from another loan), there are no foreclosure charges. My love hate relationship with SBI continues. It is a case of losing a bit of self esteem and gaining in blood pressure to save some money !

|

7th October 2008, 10:32

| #44 |

| Senior - BHPian Join Date: Feb 2007 Location: Delhi

Posts: 1,356

Thanked: 24 Times

| |

|

|

|

7th October 2008, 20:06

| #45 |

| BHPian Join Date: Oct 2008 Location: Mumbai

Posts: 78

Thanked: 4 Times

| |

|

|

|

Most Viewed