Team-BHP

(

https://www.team-bhp.com/forum/)

Quote:

Originally Posted by nagr22

(Post 5108729)

Will I face any problem due to having OD and TP insurances from different providers? If yes, what should I do??

|

No. It's completely fine to have OD and TP coverage from different insurers.

TP insurer will come into the picture when there's damage caused to a third party. In other cases such as own vehicle damage/theft, you'll need to approach OD insurer.

Hello BHPians,

I came to know today that the details of 'Own Damage' insurance could be incomplete/incorrect on DigiLocker certificate. Hence, if anyone is renewing his car insurance and needs to fill details of previous insurance policy, please refer to the policy document (hard copy/soft copy) only and do not rely on insurance certificate available on DigiLocker.

I learn about it after my current insurance provider informed me that the previous policy details are incorrect.

I'll explain the details once the fiasco is resolved.

Saw a news item that the multi-year Third Party component for new cars has been withdrawn, and we can now take TP insurance for just the first year (along with own damage component).

is this correct ?

I have a 50% NCB on my petrol car, and the Hyundai dealer tells me that it won't transfer to a Kona Electric because the cars are different - petrol vs electric.

Thoughts? I am payinng almost Rs 90,000 for the first year in insurance (via the car dealer), and would very much like to bring this down.

Quote:

Originally Posted by Car Fan

(Post 5129133)

I have a 50% NCB on my petrol car, and the Hyundai dealer tells me that it won't transfer to a Kona Electric because the cars are different - petrol vs electric.

Thoughts? I am paying almost Rs 90,000 for the first year in insurance (via the car dealer), and would very much like to bring this down.

|

Please call one of the Insurers directly and get a quote for your new car insurance. As far as I know, insurance is linked to a person for his vehicle. NCB can be transferred from say a sold Bike to a new Car, so I don't see any reason why this NCB cannot be transferred to an EV unless IRDA has allowed specific clauses for EVs.

--Kalyan

Has HDFC Ergo stopped doing cashless insurance settlements? An unfortunate incident and the car needs to be repaired under insurance. However i have now been told that HDFC Ergo has stopped doing cashless disbursements.

So the result being -

- i'll pay upfront and they'll reimburse me

- For some reason i'll have to take over the burden of GST as it is non-refundable for personal vehicles and can be claimed by corporate cars.

Has anyone faced this issue?

This was also not the case when i had taken the insurance else i would not have gone with them in the first place also can insurance companies change all these terms mid way?

Edit: This seems to be a dealer level issue for which the customers are supposed to suffer.

The dealer has offered me an insurance quote of Rs 82,000 (Reliance) for my soon-to-be-delivered Hyundai Kona. HDFC Ergo gave me a Rs 62,000 quote when I checked online. The insurance guy at the dealership says that the third party cover quantity is set by the IRDA (he has quoted Rs 20,660) and that the HDFC TP amount (Rs 8,100) is incorrect.

Is this right? Could HDFC Ergo be giving me the wrong number or is the insurance chap at the dealership misleading me? I have gone to the IRDA website but am unable to locate a TP price.

Also, to get the quote closer to the one I got online, he has dropped Return-to-Invoice (RTI) cover. Is it important to keep RTI or can I dispense with it?

Quote:

Originally Posted by Car Fan

(Post 5133642)

Is this right? Could HDFC Ergo be giving me the wrong number or is the insurance chap at the dealership misleading me? I have gone to the IRDA website but am unable to locate a TP price.

Also, to get the quote closer to the one I got online, he has dropped Return-to-Invoice (RTI) cover. Is it important to keep RTI or can I dispense with it?

|

If HDFC is giving you a quote then it must be correct, dont get misled by the dealer comments.

Have attached the 3 yr TP rates for the electric vehicles for your reference. Cross check the correct one suitable for your car.

Guys,

For a pre-owned vehicle that we purchased recently, we are literally running behind the current insurer (Tata-AIG) to transfer the original owner's insurance to our name for almost a week. We have submitted documents and follow-up daily via calls and emails to the customer care team, and even tweeted about it to Tata-AIG's handle but doesn't seem to have any effect.

Any guidance/inputs on contact ids for higher up in Tata-AIG? This was a simple activity to transfer the insurance and pay the additional NCB cost, but not sure why there's such a delay.

Quote:

Originally Posted by Car Fan

(Post 5133642)

Is this right? Could HDFC Ergo be giving me the wrong number or is the insurance chap at the dealership misleading me

|

Don't let dealers steamroller you into buying their insurance if you can get better deal. Ignore their tricks!

Return to Invoice is like a

luxury insurance. Nobody can tell you whether

you want/need it. Nice thing to have: you decide.

One way to get a slight reduction on premiums is to increase the amount you have to pay towards damage repairs. If you have sufficient income/capital that you can pay 10k, 20k, etc without pain, use that to get a lower premium. This comes under my heading of

don't pay insurance for stuff you can afford anyway.

Quote:

Originally Posted by ghodlur

(Post 5133757)

If HDFC is giving you a quote then it must be correct, dont get misled by the dealer comments.

Have attached the 3 yr TP rates for the electric vehicles for your reference. Cross check the correct one suitable for your car.

|

Turns out the Hyundai dealer was right - the Kona engine is 100 kW and therefore falls in the highest Third Party band. I had been confused by the fact that the battery is 39 kWH, as had the HDFC Ergo website it seems.

Hello Folks

I generally use my car for long drives (1k-3k) kms. So once we were coming back, a dog came on the road out of nowhere and there was damage to cars right front (bumper mostly).

I was still like 700kms away from home. After few hundred kms pebbles from the truck front hits the cars windshield on the left side and now windshield is also cracked.

When we went for insurance, they said only one of side can be claimed.

Is there a rule around it? If company rejects one of the sides, is there anything I can do about it?

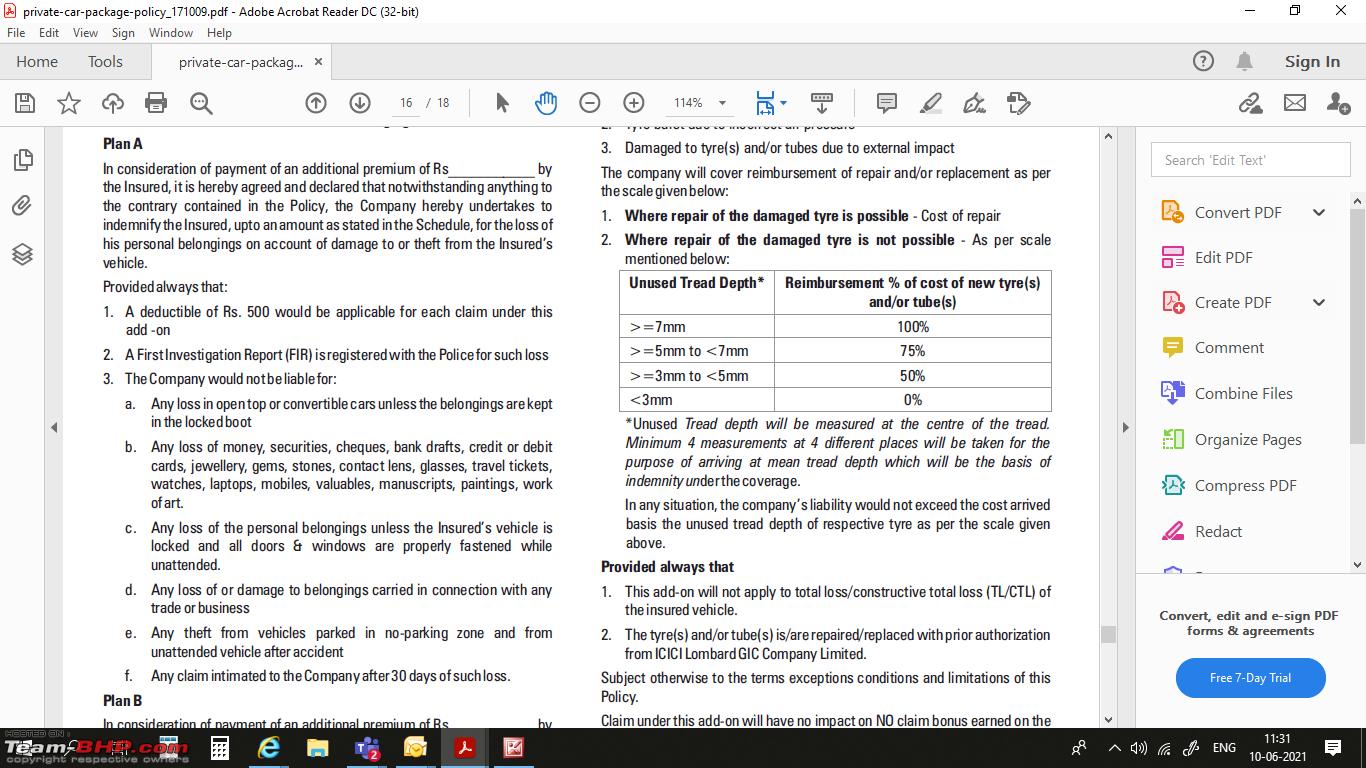

Recently, when one of my car was met with an accident, my sisters laptop bag was picked. We immediately got 2 separate FIR done from the nearest Police Station, one for the car and another for the laptop stolen from the accident spot.

My car insurance was from ICICI Lombard which covered Loss of Personal Belongings, which, while paying a premium the agent did say that it covers expenses up to ₹50,000 if the tax invoice of the same can be produced. We did hand over FIR copy and Tax Invoice to the authorised service centre which has a cashless claim facility after a lot of hassle (earlier it was stated to get another claim number by calling ICICI Lombard toll-free number, but executive on call abruptly denied and said the claim will be rejected, who knew they were correct). But, on the second half of the day, received an email regarding that claim for Loss of personal belongings has been rejected, a quick call to ICICI Agent handling my case he shared below picture for the email and said to adhere to Plan A.

Now it makes me think with these clauses in place, this add-on is far from being useful when the contingency arises.

Quote:

Originally Posted by utsav

(Post 5135174)

Is there a rule around it? If company rejects one of the sides, is there anything I can do about it?

|

If you can prove to the Insurance surveyor that both the damages are co related then one claim can be used to get the repairs done on the damages. If not then 2 separate claims need to be raised for the damage repair.

For eg you could say the dog hit the car which went over gravel and flying stones hit the windshield damaging it.

Quote:

Originally Posted by GautamJ

(Post 5135675)

Now it makes me think with these clauses in place, this add-on is far from being useful when the contingency arises.

|

The pic which you shared is that for the add on cover wordings? Since it is clearly mentioned that laptops will not be applicable for claim under loss of personal belongings, you will need to live with it. What does the Plan B say? What plan did you opt for?

Quote:

Originally Posted by ghodlur

(Post 5135754)

The pic which you shared is that for the add on cover wordings? Since it is clearly mentioned that laptops will not be applicable for claim under loss of personal belongings, you will need to live with it. What does the Plan B say? What plan did you opt for?

|

No, the picture shared is what ICICI Lombard Claim agent emailed upon loss of personal belongings claim being rejected. The plans for loss of personal belongings were neither mentioned in quotation nor was it informed by the agent while renewing insurance. The insurance policy mentions only Plan A of ₹50,000 with regards to the loss of personal belongings.

| All times are GMT +5.5. The time now is 10:55. | |