Team-BHP

(

https://www.team-bhp.com/forum/)

At the moment with the auto industry in the midst of a cataclysmic transformation I will avoid all auto shares. One does not know.

Remember the same happened with film manufacturers when the industry went digital Kokak was a blue chip one day and then rapidly went into the dumps.

Roads Ministry is mulling mandatory phase out of old trucks and buses and the new policy is likely in next 4-6 weeks (source: Sonia Shenoy, CNBC)

This could benefit Ashok Leyland. The company seems to be at a sweet spot. Very good fundamentals ( debt manageable, ROE is very good at 22%, dividend payout is also very good with dividend payout at more than 1% at current levels so that mitigates your downside).

Disclosure: This is NOT a recommendation and I do not own any. Just for academic purposes. I reserve the right to enter/exit at any stage.

Quote:

Originally Posted by joslicx

(Post 4335559)

Roads Ministry is mulling mandatory phase out of old trucks and buses and the new policy is likely in next 4-6 weeks (source: Sonia Shenoy, CNBC)

This could benefit Ashok Leyland. The company seems to be at a sweet spot. Very good fundamentals ( debt manageable, ROE is very good at 22%, dividend payout is also very good with dividend payout at more than 1% at current levels so that mitigates your downside).

Disclosure: This is NOT a recommendation and I do not own any. Just for academic purposes. I reserve the right to enter/exit at any stage.

|

If this becomes true, then it will also benefit Tata Motors, wouldn't it?Looks like an opportunity, but let us wait and watch what the budget holds!

Quote:

Originally Posted by AdiSolEn

(Post 4335632)

If this becomes true, then it will also benefit Tata Motors, wouldn't it?Looks like an opportunity, but let us wait and watch what the budget holds!

|

Yes, it would be right to say that such a move would benefit Tata Motors and Eicher as well.

Just that, from investment perspective Tata Motors scares me. They have huge debt on their books. We have seen what debt does to companies. Just look at the likes of Reliance Comm, Suzlon, Videocon, Essar etc. If possible, we should prefer companies with less debt or best are debt free companies. Unless we have some insider information about companies with weak fundamentals its better to avoid them howsoever appealing they may appear. Also another thing that goes against Tatas is their poor record in creating wealth. Except for TCS, not many of their group companies are known to have created substantial wealth. They have a complex structure and cross subsidizing among group companies which is not a good thing for shareholders of those companies.

Quote:

Originally Posted by joslicx

(Post 4335654)

Yes, it would be right to say that such a move would benefit Tata Motors and Eicher as well.

Just that, from investment perspective Tata Motors scares me.

|

That's correct, but leveraged companies that can grow faster than the rate of interest stand to gain higher than debt-free companies. Tata Motors is on the cusp of a potential growth story.

A large part of the debt is due to JLR acquisition which is doing well on its own. Also, Tata Motors' success or failure is largely dependent on JLR, which has benefitted from falling GBP.

However, on the domestic front, TML is already transforming itself. I don't need to explain how well received Tiago, Tigor and Nexon are. Next in line are 2 SUVs. The truck policy will be a big boost. TML is a frontrunner in EV tech in India and Niti Aayog has already announced a big push (free parking, toll waiver, separate identity through green number plates). Expect more freebies in the budget.

All this makes a strong case for investment in Tata Motors over the likes of M&M and/ or MSL.

Quote:

Originally Posted by joslicx

(Post 4335654)

Just that, from investment perspective Tata Motors scares me. They have huge debt on their books.

|

Quote:

Originally Posted by Nonstop-driver

(Post 4335668)

That's correct, but leveraged companies that can grow faster than the rate of interest stand to gain higher than debt-free companies.

|

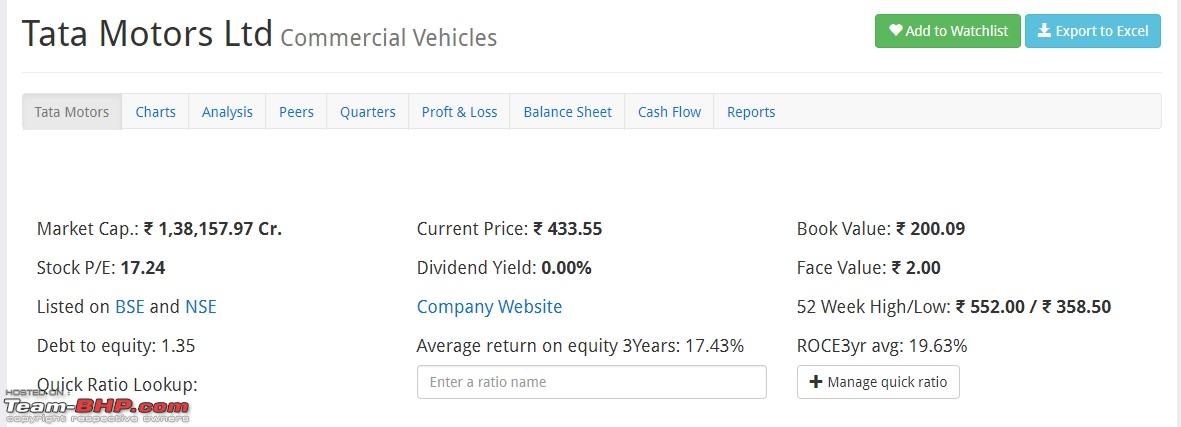

An important parameter that will help you decide if a debt laden company is worth investing or not is

Return on Capital Employed or RoCE. If RoCE is consistently higher than cost of capital (8%), then it is worth looking at.

You can get average RoCE numbers from screener.in - enter "ROCE" in 'Enter a ratio name' field and select last year, last 3 years or 5 years RoCE number

Note that Tata Motors has a 3 year average RoCE of 19.63%. It means the debt taken on to buy and run JLR was a good decision.

Quote:

We have seen what debt does to companies. Just look at the likes of Reliance Comm, Suzlon, Videocon, Essar etc

|

Now look at the 3 yr avg RoCE numbers of these companies -

RCom: 2.11%

Videocon: 7.28%

Suzlon: 16.94% (quite high, could mean Suzlon is turning around its business)

However,

a world of caution. RoCE numbers are based on past results and does not predict the future. For example: If there is a global recession, sales of JLR will drop and so will the operating profit. But the debt levels and interest costs will remain the same. Tata Motors will quickly swing into losses.

So what I do is look at interest costs and compare it with operating profits. My danger mark is interest costs crossing 25% of operating profits. For Tata Motors (last column mentions interest costs, below other income) -

Quote:

Originally Posted by Nonstop-driver

(Post 4335668)

That's correct, but leveraged companies that can grow faster than the rate of interest stand to gain higher than debt-free companies. Tata Motors is on the cusp of a potential growth story.

All this makes a strong case for investment in Tata Motors over the likes of M&M and/ or MSL.

|

I'd agree with your arguments and the inference that there is a strong case for Tata Motors. Probably I have a much lower risk appetite and I like companies that have lesser debt or no debt on their books while still maintaining their growth. I've burnt my fingers with wrong type of companies (your RelComs and Aban Offshores) in the past :) I still have them in my portfolio and cannot even sell as the value is almost nil.

Quote:

Originally Posted by smartcat

(Post 4335693)

An important parameter that will help you decide if a debt laden company is worth investing or not is Return on Capital Employed or RoCE. If RoCE is consistently higher than cost of capital (8%), then it is worth looking at.

You can get average RoCE numbers from screener.in - enter "ROCE" in 'Enter a ratio name' field and select last year, last 3 years or 5 years RoCE number Attachment 1714233

Note that Tata Motors has a 3 year average RoCE of 19.63%. It means the debt taken on to buy and run JLR was a good decision.

Now look at the 3 yr avg RoCE numbers of these companies -

RCom: 2.11%

Videocon: 7.28%

Suzlon: 16.94% (quite high, could mean Suzlon is turning around its business)

However, a world of caution. RoCE numbers are based on past results and does not predict the future. For example: If there is a global recession, sales of JLR will drop and so will the operating profit. But the debt levels and interest costs will remain the same. Tata Motors will quickly swing into losses.

So what I do is look at interest costs and compare it with operating profits. My danger mark is interest costs crossing 25% of operating profits. For Tata Motors (last column mentions interest costs, below other income) - Attachment 1714242

|

This is as usual great post with lot of important information. Yes, I now check at least three parameters. Apart from PE and DE, the ROCE/RONW is important criteria as well. Another thing I check is the cash flow. A company generating healthy cash flow is now must for me.

Theres a very valuable resource of information on investing compiled by one Dr. Vijay Malik (

http://www.drvijaymalik.com/) This has a series of articles on complete analysis of companies and I have found them very useful. Interested people can go thru at least some of the articles on this site. Could be hugely beneficial in long run.

What is the general opinion on investing in AIS (Asahi glass) ?

ROCE is my primary filter for even starting to look at any company. If you are in business unless you earn lot more than the cost of capital either the industry is not profitable or you are a badly run company.

I tend to stay away from Leveraged company as it just adds to the overall risk. As retail investors we are just playing with probabilities so just avoid things that have more chance of failing. As buffet says tell me where I will die and I will not go there. Exceptions can be made where debt is in control and is being actively paid off. Reducing debt levels will also reduce interest costs and increase margins so profit growth will be more than sales growth

Quote:

Originally Posted by rayjaycleoful

(Post 4336310)

What is the general opinion on investing in AIS (Asahi glass) ?

|

Just took a quick look. Unjustifiable valuations. It is trading at 60 times earnings and 17 times net worth.

Quote:

Originally Posted by neeravnaik

(Post 4336343)

ROCE is my primary filter for even starting to look at any company. If you are in business unless you earn lot more than the cost of capital either the industry is not profitable or you are a badly run company.

|

RoE (Return on Equity) is more popular filter because RoCE is applicable only for companies in manufacturing and other capital intensive sectors. And not for companies in service industries (IT, finance etc). The crappiest PSU Bank will have RoCE of 20 or 30%. Because their only capital expenditure is opening of branches, and that doesn't cost lot of money when compared to their overall balance sheet.

Quote:

Originally Posted by smartcat

(Post 4335693)

An important parameter that will help you decide if a debt laden company is worth investing or not is Return on Capital Employed or RoCE. If RoCE is consistently higher than cost of capital (8%), then it is worth looking at.

You can get average RoCE numbers from screener.in - enter "ROCE" in 'Enter a ratio name' field and select last year, last 3 years or 5 years RoCE number Attachment 1714233

Note that Tata Motors has a 3 year average RoCE of 19.63%. It means the debt taken on to buy and run JLR was a good decision.

Now look at the 3 yr avg RoCE numbers of these companies -

RCom: 2.11%

Videocon: 7.28%

Suzlon: 16.94% (quite high, could mean Suzlon is turning around its business)

However, a world of caution. RoCE numbers are based on past results and does not predict the future. For example: If there is a global recession, sales of JLR will drop and so will the operating profit. But the debt levels and interest costs will remain the same. Tata Motors will quickly swing into losses.

So what I do is look at interest costs and compare it with operating profits. My danger mark is interest costs crossing 25% of operating profits. For Tata Motors (last column mentions interest costs, below other income) - Attachment 1714242

|

Thanks a lot Smartcat! Your analysis and thought process is of great value to all of us. I am taking my baby-steps in equities, and this thread is something that I always look to when in doubt :)

I personally am very cautious as of now, as I feel that a lot of shares are overvalued. I do not know when a correction will happen, but since this is my first attempt at direct equities, I'll be very cautious!

Wow, you are really a "Smart cat". I'm very new to this, rather scared of investing in equities. I'm looking for long term investments of 3 to 5 years. What is your opinion on Castrol & Welspun. Screener shows good ROE & Interest vs Operating Profits are negligible. I want to gamble with low price and more stocks options. What is your take on this?

Quote:

Originally Posted by Ramsagar

(Post 4339770)

I'm very new to this, rather scared of investing in equities. I'm looking for long term investments of 3 to 5 years. What is your opinion on Castrol & Welspun. Screener shows good ROE & Interest vs Operating Profits are negligible. I want to gamble with low price and more stocks options. What is your take on this?

|

Invest, not gamble :)

For gambling, you could check out

www.zebpay.com

For the first time nervous investor, Castrol is a good pick.

- It is a market leader

- Huge brand recognition

- Tax free 3% dividend yield, expected to rise every year

- Steady, almost guaranteed 10% CAGR growth in revenues and profits

- Very low volatility (doesn't go down a lot during corrections)

EV bogeyman will not hurt Castrol for atleast a decade or more.

I've been invested mostly in the Auto ancilliaries. In the past i've had multi baggers on Mayur Uniquoters. My current holdings are the Munjal twins (Munjal Auto and Munjal Showa), both of whom are on the cusp of giving me 3x returns in 4 years of holding.

Having said that, I am in the process of re-evaluating my positions in them for a possible churn in the next month or so. Will keep you guys posted :)

Quote:

Originally Posted by smartcat

(Post 4339980)

Invest, not gamble :)

|

True that!

My dad has 500 shares of Blue Dart from the original allotment in 1994. They were dematerialized in 2010 and have been lying in the depository since.

Over the years, the shares have grown many folds and have seen a high of nearly 8k in 2015. Currently they are trading around 4.5k.

Now the question is, will it be a wise move to trade them for another equity (with better earning potential and dependability) like say, Maruti Suzuki and forget about them for say like another 5yrs?

Or should he hold on to them for some more time?

| All times are GMT +5.5. The time now is 16:34. | |