Team-BHP

(

https://www.team-bhp.com/forum/)

Quote:

Originally Posted by woodstock3001

(Post 5830502)

I've just DM'd you to understand more on rolling returns.

|

Answering here for the benefit of all.

Here is a URL for calculating rolling returns -

https://www.mfonline.co.in/mutual-fu...riod=3%20Yearr

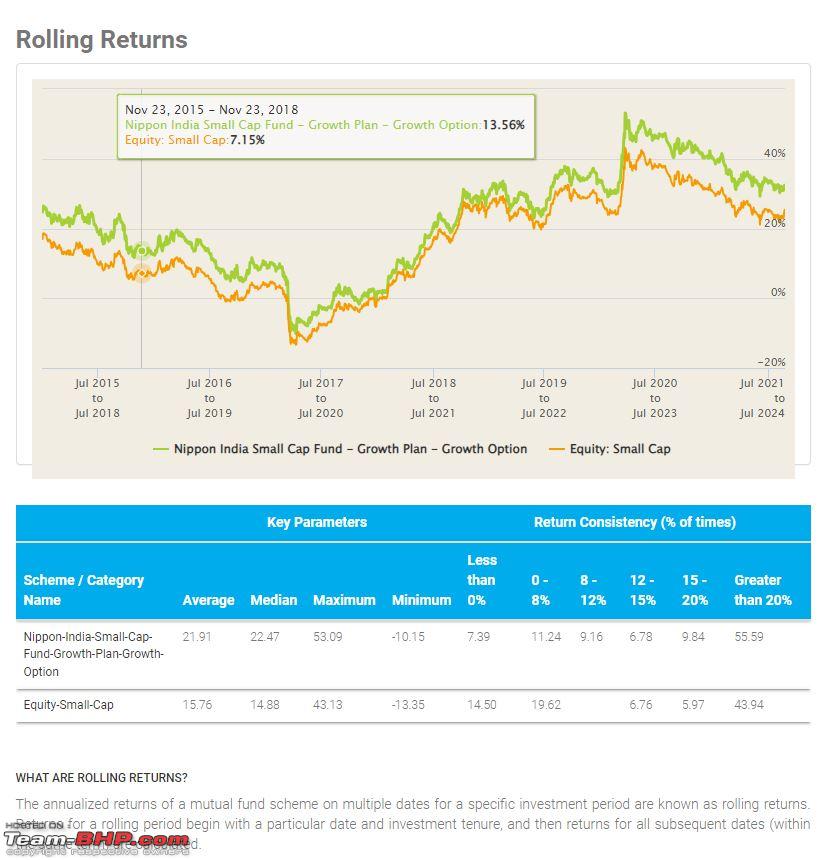

In your case for Nippon India Small cap. Since Jan 2015, the 3 year rolling return was >15% for ~66% of the time.

Quote:

Originally Posted by Naetik30

(Post 5830658)

Answering here for the benefit of all.

In your case for Nippon India Small cap. Since Jan 2015, the 3 year rolling return was >15% for ~66% of the time. Attachment 2646967

|

Thank you. This is exactly we all need to be mindful for. CAGR over a period is not the same having the consistent return equivalent to the CAGR each year. For a duration of 10 years as is the case for OP, you might end up in a phase where half of the years do not match up to the CAGR value.

Thank you for your details. The overall picture on current costs (indexed to future 10 yrs), your comfort on healthcare coverage, and partial coverage of your kids' education paints the picture better. I would leave the comfort of covering the educational expenses with you as you are best placed to assess that. My only call out would be the aggressive 15% CAGR and explanation of my concern is explained precisely by the rolling returns response shared by Naetik30.

I have a rather weird problem. I am switching jobs and new employer does not allow to trade from not approved securities company. They have shared a list of couple of them which are approved in their system. They do this so that they can track the activities in the demat account. My current demat account are in Sharekhan and Zerodha and both are not approved. While I have identified the process for transfer of shares from 1 demat account to another i.e. through CDSL easiest (which is also not so easy to implement).

But my question is on the process for transfer of mutual funds since the mutual funds in Zerodha are issued in direct mode (and not in Regular mode wherein the securities company make money in the form of commission from mutual funds) so can these be converted into regular mode and be held in another demat account.

Someone in the family was misguided to transfer their direct mutual funds into the demat acount of the bank and my family member ended up paying for it (so the banker didn't tell him that the direct mutual funds will be sold and rebought as regular mode, which led to capital gains tax and increased overall cost). I obviously don't want that to happen since some of investment is as recent as this month due to SIPs wherein I will be subject exit load.

any help will be much appreciated.

Quote:

Originally Posted by youknowitbetter

(Post 5831025)

But my question is on the process for transfer of mutual funds

|

Mutual fund units (both Direct and Regular) are held in either of the two modes - SoA and Demat. In SoA format, they are held by the AMC (CAMS, KFin etc.) of the Mutual Fund that you invested in. This is the case irrespective of the platform through which you purchase(d) the units (Coin/MFU/MFOnline etc.). In Demat format, they are credited to your Demat account upon purchase/transfer.

Assuming your units are with AMC (SoA format), in case your employer insists on the MF units also to be transferred to your Demat account, then you need to work with the MF AMC and convert them from SoA to Demat format and get them credited to your Demat account. This process has nothing to do with conversion from Direct to Regular (or viceversa) and will not result in any capital gains.

You need to check with your demat provider if they let you transact Direct units on their platform (whenever you want to redeem them).

NB: Check if you can redeem Demat format MF Units in decimals.

Quote:

Originally Posted by youknowitbetter

(Post 5831025)

I have a rather weird problem. I am switching jobs and new employer does not allow to trade from not approved securities company.

|

Noob question - why does anyone needs employer approval to trade or invest their personal money or am I missing something?

Quote:

Originally Posted by drive.helios

(Post 5831044)

Noob question - why does anyone needs employer approval to trade or invest their personal money or am I missing something?

|

I think it is as per SEBI (Prohibition of Insider Trading) Regulations or otherwise some other policies applicable to Financial Sector employees.

Quote:

Originally Posted by youknowitbetter

(Post 5831025)

I am switching jobs and new employer does not allow to trade from not approved securities company.

But my question is on the process for transfer of mutual funds...

|

Generally employers monitor equity (shares) transactions of designated persons (insiders) but not mutual fund transactions. You may want to reconfirm this with your employer.

Quote:

Originally Posted by drive.helios

(Post 5831044)

Noob question - why does anyone needs employer approval to trade or invest their personal money or am I missing something?

|

Regulations. Different for different employers, sectors and level of the employee. Very common if you are working in the Financial Services industry.

Quote:

Originally Posted by skumare

(Post 5831088)

I think it is as per SEBI (Prohibition of Insider Trading) Regulations or otherwise some other policies applicable to Financial Sector employees.

Generally employers monitor equity (shaers) transactions of designated persons (insiders) but not mutual fund transactions. You may want to reconfirm this with your employer.

|

OP query is not about the limitations of holding MFs. He is asking about how to proceed and safeguard his existing MF holdings because he will be forced to close the current DMAT account and move to another one that is approved by the employer. Transfer of Shares is a well known and laid our process. Transfer of DMATed MF units is not yet clear to OP.

Hi All

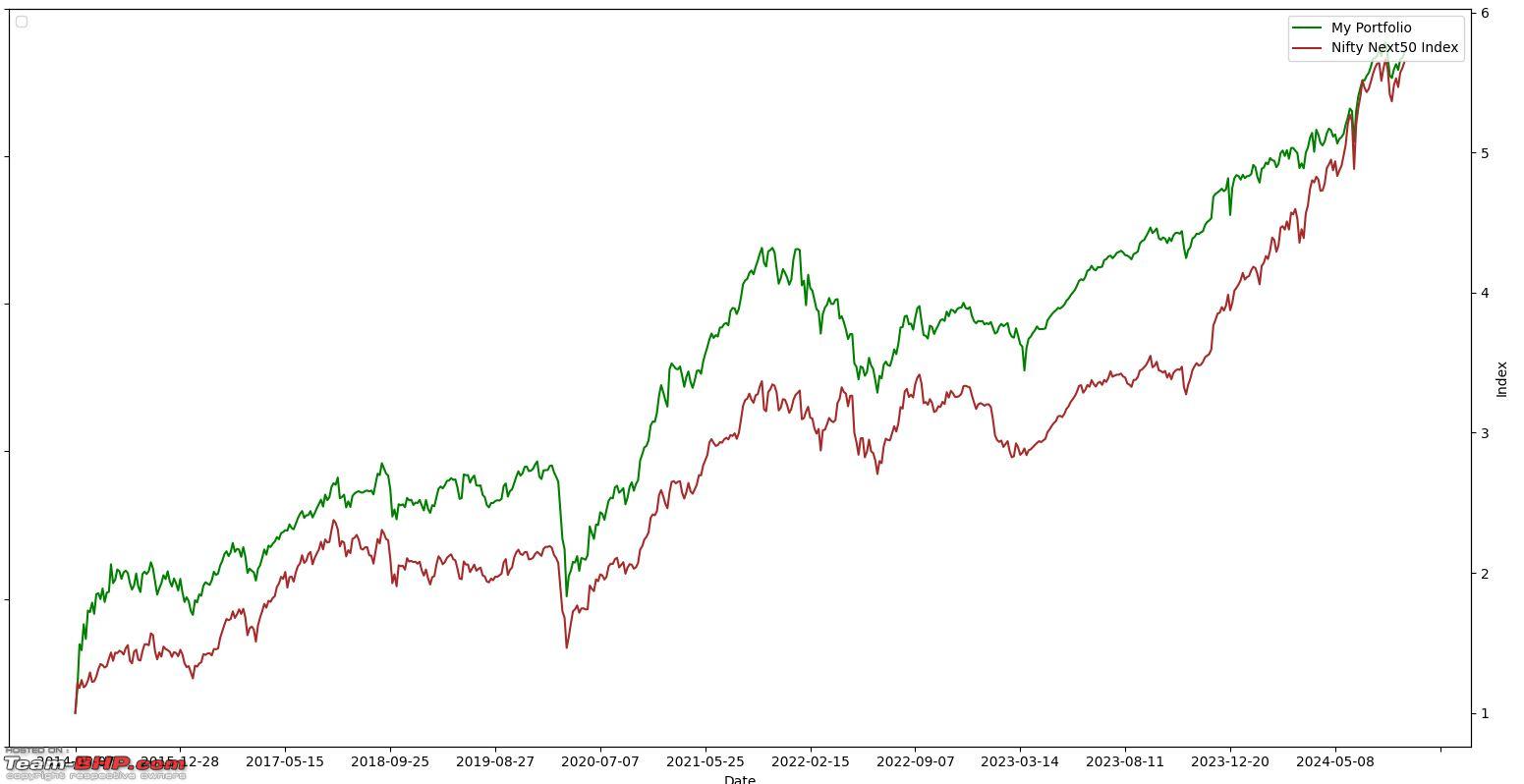

I use ETmoney for my MF investments. Have used ICICIDirect in the past for the same. I have investments in one largecap, one midcap, one nifty50 index, one flexicap and one small cap. All these fund sips were started at different times over the past 10+ years. And there are some lumpsome investments as well.

I always wanted to compare how my portfolio compares against say the Nifty50 or the NiftyNext50 etc. But didnt find any specific portal that did this.

ETmoney shows the performance of individual MFs in my portfolio. Same with other portals. But never a consolidated view of my portfolio against an index.

I wanted to analyze -

1. Performance of my entire portfolio of MFs against any given index.

2. Take into account various parameters like amount of investment, redemptions, and lot more complexities when plotting against a given index.

3. Only input would be the MF CAS Transaction statement over 10+ years in PDF format.

Last couple of weekends, I spent to develop my own algorithm (to normalize personal portfolio and benchmark nav values) and script to do what I wanted. And after about 20 hours I am happy to say I got what I wanted. Here is a sample -

My portfolio vs UTI Nifty50 index fund

My portfolio vs ICICI Nifty Next 50 index fund

Next steps -

1. Generate customized reports for (a) Annualized XIRR for my portfolio (b) Best return year, quarter (c) Worst return year, quarter.

2. Some more in the thought process.

If any one wants their portfolio to be analyzed, please post your portfolio here and I'll reply. Feedback welcome :).

Quote:

Originally Posted by youknowitbetter

(Post 5831025)

But my question is on the process for transfer of mutual funds since the mutual funds in Zerodha are issued in direct mode (and not in Regular mode wherein the securities company make money in the form of commission from mutual funds) so can these be converted into regular mode and be held in another demat account.

any help will be much appreciated.

|

This is an interesting situation I'm coming across, but my assumption is that your employer is taking active steps to avoid potential insider trading, understandable.However, you might just wanna check with your employer again if this covenant applies for mutual funds also?

In my personal experience, coin is a seamless platform to invest in mutual funds.Only flip side I have noticed is that it works well as long as you are only interfaced with coin, meaning if you directly try logging in to the AMC (fund house) portal and try redemption, reinvestment , etc, it is not possible since the mutual funds are in demat form and the folio is not directly accessible by the AMC.

However, in your case I understand all your securities have to be transferred from one demat to another demat of a broker recognised by your employer. So I think you should be able to transfer these in similar way as your other scrips in the demat account, without having to worry about conversion of direct to regular. However the question will arise after transferring it out of coin, how would you redeem it, etc?

Eitherways, I suggest you contact the Zerodha helpline 080 4718 1999 (They ask for a 4 digit support code before connecting, which is easily available from your profile section on kite/console). There are no long waiting times and generally you are attended by fairly professional/knowledgable people, who will definitely sort out this issue, if not resolved already.

Hope it helps!

Cheers!

Hello All,

Need Suggestion for Investment! - Lumpsum / Index Funds

Background :

I am currently Working in the IT profession, 5 YOE and earning a decent amount.

I have been reading this thread for quite a while now and got some good information too.

I have been maintaining 2 bank accounts that include 1 salary account and the other personal account. Every month I transfer X amount from my salary amount to my in savings amount. As soon as my savings account hits 6 digit figure I immediately opt for FD.

My current investment Includes

1. Nippon India multi-cap fund SIP.

2. I Already have 2 FDs worth the starting 6-digit number.

Suggestion needed for

1. 1 Lumpsum scheme. ( Also planning for index funds)

2. 1 new SIP scheme.

3. Good banks that offer great FD interest.

PS - I'm a newbie and still in my mid-20s, so kindly consider the same.

Thanks and Regards

Tanvesh !

Quote:

Originally Posted by TPunchKZA

(Post 5833490)

Need Suggestion for Investment! - Lumpsum / Index Funds

PS - I'm a newbie and still in my mid-20s, so kindly consider the same.

|

If you go through the previous posts, you will know why Debt Funds are better than FDs. Considering you are in your 20s, I suggest you take help of a good financial planner and chart your goals.

With just few details, it is difficult for anyone to suggest investment ideas.

If you looking to convert your current FDs, you may do so to SGBs whenever they are made available by RBI. Or go for simple debt funds or liquid funds which give marginally better profits over FDs. It is simpler from Tax calculations as well.

If I was your age and had this wiseness of investments, then would do some percentage of SIP in Small Cap Funds and be invested for really long.

I would suggest that you first start with the objective of the investment, how much is needed in your mind for that purpose and by when. That should give you an idea of what products - MFs, bank FDs or others are best suited for your purpose.

If you are not clear on the goal yet and keen to invest into MFs then one simple option could be to invest the lumpsum into a Sensex or Nifty 50 index fund. I would suggest doing the SIP also into the same fund.

And don't start any new FDs, but instead redirect that towards the SIP. I expect that you've EPF which takes care of the debt portion of your portfolio for now.

Other than the index fund, the only category I would recommend is a flexi-cap or multi-cap once you read up on both and can decide on one amongst them.

I know I've not mentioned any specific fund names, but that is conscious. I feel you need to align to the thought process first before picking the funds.

Quote:

Originally Posted by TPunchKZA

(Post 5833490)

Hello All,

Need Suggestion for Investment! - Lumpsum / Index Funds

...

Suggestion needed for

1. 1 Lumpsum scheme. ( Also planning for index funds)

2. 1 new SIP scheme.

3. Good banks that offer great FD interest.

PS - I'm a newbie and still in my mid-20s, so kindly consider the same.

Thanks and Regards

Tanvesh !

|

I would suggest consulting a SEBI registered fee only planner. While investment strategy can be easily done if you are financially savvy it is a better idea to have a complete picture and link all investments to goals.

A third party can help here.

Note that such financial planners cannot make you rich fast but will typically recommend dull boring products depending on your goals and more important your risk profile.

A list of planners here:

https://www.feeonlyindia.com/

Quote:

Originally Posted by drive.helios

(Post 5831044)

Noob question - why does anyone needs employer approval to trade or invest their personal money or am I missing something?

|

Two main reasons:

- To prevent insider trading

- To prevent conflict of interest

There are regulations to prevent insider trading in most countries. As part of compliance, companies (especially financial companies) have an obligation to track their employees' investments to assess whether anyone is using any insider information for personal benefit in the stock markets.

Even if you weren't directly working in the finance arm of a company, you may still be subjected to similar regulations and restrictions. For example, even if you were to work in a Big 4 company in their Indian technology consulting division on a project for a client that sells pizzas in the US, you would still have to comply with such financial disclosure regulations. The implication is that there may be a

chance that you had access to insider information and the company will want to ensure that they don't get mired in lawsuits for

perceived infringements as well.

Conflict of interest may arise when you're invested in some securities or fund houses but you end up working for their competition with your employer's projects. Crude example: You own stocks of Pizza Hut but work at Domino's. Therefore there's a chance you might sabotage Pizza Hut somehow so that Domino's gains and you gain as well by association.

Quote:

Originally Posted by youknowitbetter

(Post 5831025)

I have a rather weird problem. I am switching jobs and new employer does not allow to trade from not approved securities company...

But my question is on the process for transfer of mutual funds since the mutual funds in Zerodha are issued in direct mode (and not in Regular mode wherein the securities company make money in the form of commission from mutual funds) so can these be converted into regular mode and be held in another demat account.

Someone in the family was misguided ... I obviously don't want that to happen since some of investment is as recent as this month due to SIPs wherein I will be subject exit load.

|

You should check with your new employer about expectations and understand them thoroughly before taking action.

You will be granted a reasonable time to comply with the regulations for your existing investments.

I have had to deal with this and here is an over-simplified version of my experiences:

- If you are using Mutual Funds (MFs) bought directly from MF AMCs, then you can continue in direct mode as usual. You may only need to report the fund name and perhaps the amounts in SIP/Lump Sum. This is because you are only buying MF units and not directly trading in the stock market. Therefore as you have no control over what securities are bought and sold in the underlying scheme, you neither have a conflict of interest nor can you indulge in insider trading.

- There may be a case where investments in a Mutual Fund AMC (a fund house such as HDFC, Kotak etc.) may be a potential conflict of interest. In such cases, your employer would generally have a clause that says that as long as you get your involvement pre-approved/approved, you can continue with such fund houses with the approval.

- Any stocks that you were directly trading in via Demat accounts can be subjected to the rules of your new employer. They are within their rights to give you notice to switch your demat account provider and you would have to comply.

Generally, you are in safer territory with Mutual Funds (bought directly from AMCs) as you have no direct involvement in their activities. Quite simply, declarations and approvals, if applicable, suffice and you can live with peace of mind that you're not inadvertently putting the company and yourself at any kind of regulatory or legal risk. You do lose the convenience of seeing all your investments in a single demat account, but I prefer peace of mind from regulations than the convenience of visibility.

Regarding upcoming SIPs, you can cancel the SIPs and start fresh ones directly with the MF AMCs. Again, do this after you're very clear on the actions to be taken after consulting the new employer.

Having said all that, since your question piqued my curiosity, I did some digging.

Posting a couple of links that may be useful:

https://support.zerodha.com/category...ds-out-of-coin

Something for your new employer:

https://support.zerodha.com/category...roker-employer

| All times are GMT +5.5. The time now is 11:17. | |