Team-BHP

(

https://www.team-bhp.com/forum/)

Quote:

Originally Posted by babhishek

(Post 4228329)

Get the Maxgain now. I have been on maxgain for 10 yrs, the only issue I see with SBI, is that they are lethargic and lazy as a company/bank. While paying INR1000 anytime sounds good, getting the conversion might be a pain and require umpteen follow ups.

|

Actually I wish to spend some money on a car and renovation in the flat. Any surplus cash would mostly go in these 2 areas and once I get an idea of how much amount remains I'll get it opened. Waiting a month or two isn't really that big an issue but 0.15% on 70 lakhs makes a little difference in the EMIs which I'm trying to avoid in the first year at least.

Quote:

Originally Posted by babhishek

(Post 4228329)

FYI, getting the annual repayment statement from SBI is a challenge, compared to other banks who send online statement every month/annually.

|

Wouldn't the user get to see this information when they login online in their home loan account?

Quote:

Originally Posted by maglev

(Post 4216268)

I have a query with regard to SBI's Max Gain Loan. As the EMI remains constant, and interest charged is dependent upon principle outstanding minus deposit in MaxGain. Then how is the Principle being amortized? Is it the same as a traditional home loan or not, if not, then what happens to the difference between scheduled interest payment vs. actual interest paid?

|

Quote:

Originally Posted by tejas08

(Post 4216637)

The difference of Interest gets credited to your OD Account at the end of every month.

|

Is this a separate account or the same maxgain homeloan account ? Kindly clarify

Quote:

Originally Posted by babhishek

(Post 4228436)

Is this a separate account or the same maxgain homeloan account ? Kindly clarify

|

Same Account. Can't explain anymore details since even I don't have much information on this.

I am planning to take SBI Max Gain HL and wanted some clarification on the Bank Charges over and above the HL Amount.

Below is what the SBI HL Person has quoted for Joint Loan Amount of ~75L:

8.45% - Normal Term Loan

8.60% - Max Gain

Processing Fees: 11,800 /- [Maybe negotiable to 50%]

Flat Valuation - 1000 /-

Title Search - 4000 /-

As per him, below charges needs to be paid to the Govt.:

0.20 of loan amount Mortgage Amount - 15,000 /-

1500 - Stamp Paper

1800- Intimation Mortgage

Property Insurance - Around 20,000 /- One time Payment

Can anyone validate and let me know if this looks right?

Would really appreciate if someone could clarify the below Query as i need to decide on it soon.

Quote:

Originally Posted by abhi3284

(Post 4237805)

I am planning to take SBI Max Gain HL and wanted some clarification on the Bank Charges over and above the HL Amount.

Below is what the SBI HL Person has quoted for Joint Loan Amount of ~75L:

8.45% - Normal Term Loan

8.60% - Max Gain

Processing Fees: 11,800 /- [Maybe negotiable to 50%]

Flat Valuation - 1000 /-

Title Search - 4000 /-

As per him, below charges needs to be paid to the Govt.:

0.20 of loan amount Mortgage Amount - 15,000 /-

1500 - Stamp Paper

1800- Intimation Mortgage

Property Insurance - Around 20,000 /- One time Payment

Can anyone validate and let me know if this looks right?

|

Seems right amount. Only excess seem to be the property insurance which anyway would be helpful for you. Quote for insurance seems to be alright. Insist on reducing the processing charge. There might be some reduction in interest rate if wife is made as primary applicant.

Quote:

Originally Posted by abhi3284

(Post 4239933)

Would really appreciate if someone could clarify the below Query as i need to decide on it soon.

|

Seems to be reasonable. Property insurance quote is also fine. Make your wife as a primary applicant and the interest rate will come down. Don't worry too much SBI RACPC is a streamlined mechanism. Almost all the things are standardaized for a given city/region.

Quote:

Originally Posted by abhi3284

(Post 4237805)

Below is what the SBI HL Person has quoted for Joint Loan Amount of ~75L:

8.45% - Normal Term Loan

8.60% - Max Gain

Processing Fees: 11,800 /- [Maybe negotiable to 50%]

Flat Valuation - 1000 /-

Title Search - 4000 /-

As per him, below charges needs to be paid to the Govt.:

0.20 of loan amount Mortgage Amount - 15,000 /-

1500 - Stamp Paper

1800- Intimation Mortgage

Property Insurance - Around 20,000 /- One time Payment

|

You can validate interest rates from the SBI official page

link

Processing fees offers comes on and off. I paid nothing five years back.

Valuation and Title search charges are mandatory. Charges have increased from 3k to 5k.

Charges paid to govt may be correct. You should get receipt.

Property insurance is optional.

So I took a regular SBI Home Loan recently and after 1 EMI was deducted I converted it to MaxGain.

As soon as it was converted to Maxgain I moved all my funds to the OD account and didn't leave enough in my salary account for the next EMI to be deducted. The EMI due date passed. No calls from the bank except an SMS that if you haven't paid the EMI please do so else ignore.

I realized this later that I'd not left sufficient funds for EMI deduction and called up the Branch Manager. He told me not to worry since the EMI was 69k and I'd already moved close to 700k in the OD account.

I just checked my MaxGain account statement and there is absolutely no deduction for October month except for "Debit Interest" in the month end. It is 45k.

What really happened to the EMI? I'm totally lost but the Branch Manager is telling me not to worry.

Quote:

Originally Posted by fine69

(Post 4297702)

I realized this later that I'd not left sufficient funds for EMI deduction and called up the Branch Manager. He told me not to worry since the EMI was 69k and I'd already moved close to 700k in the OD account.

What really happened to the EMI? I'm totally lost but the Branch Manager is telling me not to worry.

|

I think you have nothing to worry about, as long as there are sufficient funds in OD account. My understanding is that whatever funds you have parked in OD account reduces your outstanding loan principal and thus reduces your EMI as well. The required amount will be deducted from your OD account by the bank.

I had a Maxgain HL many years back. After the cheques for EMI I gave to the bank (12, I think) ran out, the EMI was always deducted from the OD account and I never had an issue.

I don't remember exactly how it showed up in the account statement. There's an amount "Drawing Power" in your Maxgain HL. Did it come down by 45K or a larger amount?

Quote:

Originally Posted by fine69

(Post 4297702)

I just checked my MaxGain account statement and there is absolutely no deduction for October month except for "Debit Interest" in the month end. It is 45k.

What really happened to the EMI? I'm totally lost but the Branch Manager is telling me not to worry.

|

I do NOT recommend MaxGain account and suggest going back to regular home loan account from SBI. I have been fighting complaint with SBI for two years now. I had to file two RTIs to uncover the discrepancy in computing my outstanding principal. The complaint is still going on. The fact is SBI themselves have no system or reporting in place to know how any parked funds in OD account go on to save you money. It sounds nice in theory but their systems/online account doesn't tell you at any time how the OD account actually serves you. It will just show you credits and debits and with no relation to your home loan account and to your EMIs. That reason alone should be enough to turn one away! So buyers beware! and your manager just telling you not to worry rather than giving you a proper statement instead should be a reason to worry.

Quote:

Originally Posted by fine69

(Post 4297702)

What really happened to the EMI? I'm totally lost but the Branch Manager is telling me not to worry.

|

Quote:

Originally Posted by StarrySky

(Post 4297793)

I think you have nothing to worry about, as long as there are sufficient funds in OD account. My understanding is that whatever funds you have parked in OD account reduces your outstanding loan principal and thus reduces your EMI as well. The required amount will be deducted from your OD account by the bank.

|

Quote:

Originally Posted by trishul

(Post 4298211)

It sounds nice in theory but their systems/online account doesn't tell you at any time how the OD account actually serves you. It will just show you credits and debits and with no relation to your home loan account and to your EMIs.

|

There were gaps in my understanding of the product as well. Here's a

link I found which explains how Maxgain works. The example in the link assumes that you keep paying your regular EMIs. If you don't pay EMI separately, they should come from the funds you have parked in the OD account.

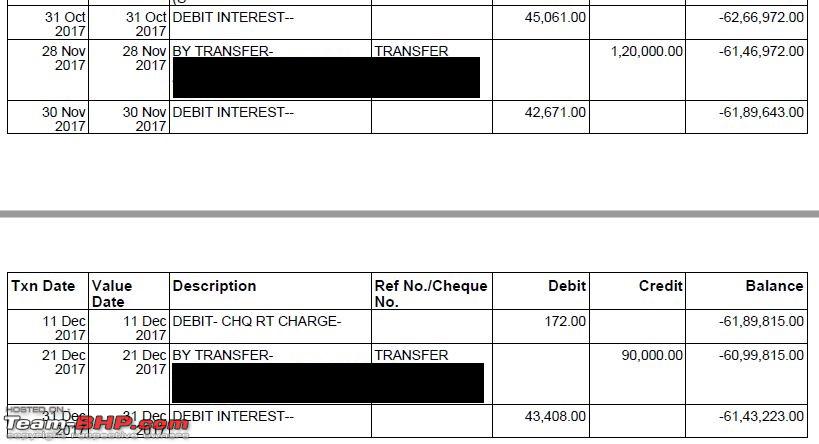

So the update on my MaxGain account is that EMIs aren't getting deducted from my salary account at all now.

The snapshot of the statement is below. I'd deposited 7-8 lacs when my EMI was 60k. As you can see it came down and I continue to deposit some money on and off and the debits are now to the tune of 42-45k.

Now I asked for the interest certificate from the bank and what I got was as follows:

Amount paid upto Dec 2017

Interest

- 92k

Principle - 445k

Total - 538k

Amount proposed to be paid till Mar'18

Interest - 30k

Principle - 148k

Total - 179k

Overall for FY 17-18

Interest - 123k

Principle - 594k

Total - 717k

I haven't really paid the amount it shows in my interest certificate so why does it say I've paid 538k when I haven't really.

Only one EMI of 60k was deducted after which the Maxgain account was activated. As per the statement I've paid more like 190k till Dec'17 instead of 538k as shown in the interest certificate.

Somebody help me figure this out please:

Hi,

HNY to all.

Any pointers on adding interior & furnishing costs to the SBI maxgain home loan? I'm looking at transferring my existing HL from LICHFL to SBI, but the principal outstanding is below the 20L threshold. Hence the thought of adding the interior cost. Any pointers much appreciated.

thanks.

V

I have an SBI home loan of 4.25 lacs outstanding. I am planning for a top up for doing up the interior. I wanted to know if I can convert this into Maxgain. When I visited the branch,they said it is only for fresh loans above 20lacs. Is it the case? Or should I visit RACPC. Reason for going for maxgain is , I have amount equal to loan which I can park in the maxgain account and pay interest free EMI.

Quote:

Originally Posted by inder

(Post 4414477)

I have an SBI home loan of 4.25 lacs outstanding. I am planning for a top up for doing up the interior. I wanted to know if I can convert this into Maxgain. When I visited the branch,they said it is only for fresh loans above 20lacs. Is it the case? Or should I visit RACPC. Reason for going for maxgain is , I have amount equal to loan which I can park in the maxgain account and pay interest free EMI.

|

As far as I know, a top up loan is a separate account. So it won't be merged with your existing outstanding home loan balance. The interest rate for the top up loan will be different as well compared to your regular home loan.

| All times are GMT +5.5. The time now is 16:10. | |