Team-BHP

(

https://www.team-bhp.com/forum/)

Quote:

Originally Posted by SilentEngine

(Post 4721802)

Sample this for incompetency: I applied for an Add-on card for my wife. Card came but not the PIN. Setting PIN from net banking or ATM isn't possible for add-on cards. It's lying unused for a year now. Nor have they sent the add-on Priority Pass after multiple requests.

|

I don't know if this is incompetency or not, but HDFC Bank doesn't send PIN mailers through snail mail nowadays unless there is an explicit request (saving paper? security concerns?).

For primary cards setting the PIN is a completely online process.

For addon cards you need to request the PIN via Netbanking. The process is:

1. Netbanking login > Cards tab > expand Request from left menu > select Credit Card ATM PIN.

2. On the right side now select the primary card from the drop down and click on PIN Request for Add on Cards.

3. Complete the process.

I believe this is documented in the documentation that came with the addon card.

Quote:

Originally Posted by Chetan_Rao

(Post 4721009)

I haven't used points to buy anything online in ages, so never been hit by the whole 'per transaction' charges.

I redeem my points lumpsum once a year, cash back to my card account (4 points = 1 rupee).

Fee: INR 25 + taxes.

|

I checked my ICICI Coral card statements for the last three years.

(BTW, the new ICICI bank site has facility to download annual card statement, which is a useful feature).

They have debited rs.75 + GST in 2016-17 as "redemption charges", rs.25 + GST in 2017-18, and nothing in 2018-19. This is probably because couple of years back, I changed to ICICI as my salary account. They have probably waived off "redemption charges", not sure though. I am not complaning :).

I redeemed part of my accumulated Payback points after a long time on bookmyshow last week. No charges

yet. Will wait and watch for the monthly statement.

Quote:

Originally Posted by binand

(Post 4722075)

I don't know if this is incompetency or not, but HDFC Bank doesn't send PIN mailers through snail mail nowadays unless there is an explicit request (saving paper? security concerns?).

|

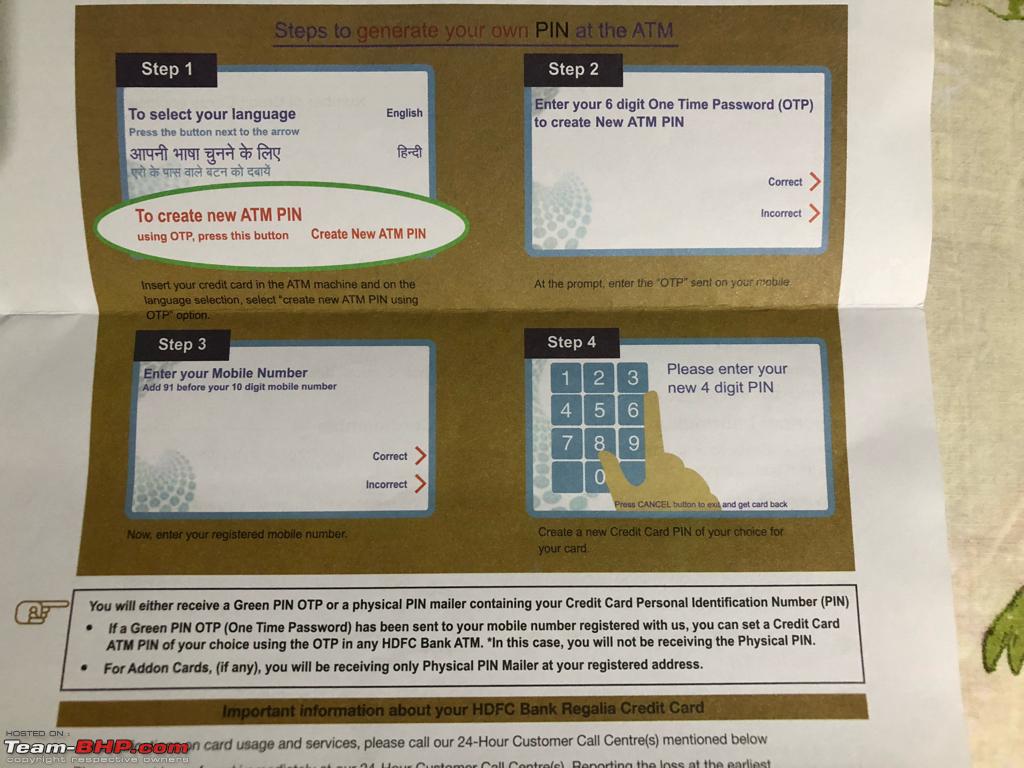

In the communication I received, it had a specific note that add-on cards will get only physical PIN. See 2nd bullet point in the attached photo. If one strictly goes by that note, there's no need to go to ATM.

I have Yes bank prosperity card which I use regularly for all my utility payments and household shopping. Seeing my usage (probably) , bank has offered to upgrade to Yes First preferred credit card which is lifetime free.

Is that a good one? Anybody using it? Quick search tells me that it provides better reward points and also complimentary lounge access.

The Citibank IndianOil card has gotten better. No longer do we need to ask for Citibank EDC machine to accrue reward points (4 points for 150/- spent) at IndianOil bunks. We can now earn points by swiping on any banks machine.

I have a Diners black card which falls in the premium/super premium category.

However, it does not have universal acceptance.

Secondly, it's always better to have a second premium card for airport lounge access etc.

Currently, I have the Yes first exclusive card which has unlimited lounge benefits. But, the reward rate is 1.5%, which is not very attractive.

Are there any other premium cards I should be looking at which can have lifetime free option or renewal fee waiver based on spends? I looked at SBI Elite but the renewal fee is only waived if annual spend is more than 10 lakhs which is too high and the card benefits are not in sync with other premium cards.

Got this Standard Chartered world emirates card, it had two monthly access to lounge with priority pass, I went to lounge in Rome with me and my wife, which was free.

Thought will share an incident [Citibank Titanium IndianOil CC]:

Around a week back, I received a SMS that my Credit Card transaction was declined due to wrong 'end date' entry - and this transaction was attempted in New York while I'm sitting cool at my home in Bangalore!!

I immediately called Citibank Customer Care and explained them the situation. They confirmed that there were no other [successful] transactions recorded and suggested that I block the card. I placed the request block and re-issue of the card. I've covered the CVV on the new card with a thin sticker and planning to do the same on others [though bit difficult on Amex cards as it displays right on front face]. It's difficult to memorize those CVV numbers :(

Quote:

Originally Posted by somspaple

(Post 4723887)

Thought will share an incident [Citibank Titanium IndianOil CC]:

Around a week back, I received a SMS that my Credit Card transaction was declined due to wrong 'end date' entry -(

|

Exactly same happened with me on the same card

Transaction at MODELL'S SPORTING GOOD NEW YORK NY on 27-Dec-19 declined on your Credit card ending ....due to invalid expiry date entry. Retry with valid expiry date

Wonder if its a data breach at Citi end?

Quote:

Originally Posted by Turbanator

(Post 4723918)

Exactly same happened with me on the same card

Transaction at MODELL'S SPORTING GOOD NEW YORK NY on 27-Dec-19 declined on your Credit card ending ....due to invalid expiry date entry. Retry with valid expiry date

Wonder if its a data breach at Citi end?

|

Exact same place where my card was tried : MODELL'S SPORTING GOOD NEW YORK on 26th. Don't know if it's data breach or something from Citi [like we get test phishing emails from IT dept on Outlook]

Have you guys considered disabling International transactions on your Citibank card?

Takes less than a minute through Internet Banking (not Mobile banking).

When I need to do an International transaction, I enable it till the transaction is done, then disable it's International use again.

International transactions do not have a MFA cushion. So I prefer keeping it in a disabled state.

Same goes for Debit cards.

Quote:

Originally Posted by adimicra

(Post 4723821)

Are there any other premium cards I should be looking at which can have lifetime free option or renewal fee waiver based on spends? I looked at SBI Elite but the renewal fee is only waived if annual spend is more than 10 lakhs which is too high and the card benefits are not in sync with other premium cards.

|

Visa has a category of cards called Visa Signature and Visa Infinite. These cards have global lounge access and you can download the list of lounges from the visa website itself. I bank with Kotak and they have a Royale credit card which is Visa Signature, most banks should have their own version of this. Since I bank with them there is no renewal fee or minimum spend.

Quote:

Originally Posted by adimicra

(Post 4723821)

I have a Diners black card which falls in the premium/super premium category.

However, it does not have universal acceptance.

Secondly, it's always better to have a second premium card for airport lounge access etc.

Currently, I have the Yes first exclusive card which has unlimited lounge benefits. But, the reward rate is 1.5%, which is not very attractive.

Are there any other premium cards I should be looking at which can have lifetime free option or renewal fee waiver based on spends? I looked at SBI Elite but the renewal fee is only waived if annual spend is more than 10 lakhs which is too high and the card benefits are not in sync with other premium cards.

|

You already have two cards with different platforms with Unlimited Lounge access for both Primary and Addon Cardholders. Why do you want one more for Lounge Access.

There isn't any other card having similar lounge access without T&Cs. SCB Ultimate gives unlimited lounge access but has a minimum spend criteria for Lounge access.

I just got Standard Chartered Super Value Titanium card mainly for the 4% fuel cashback. To make best use of it, I understand that each transaction should be for a minimum of Rs.750 and not exceed Rs.2000 and at the same time, not spend more than Rs.4000 per month (to avoid paying 1% surcharge). I also plan to use it for making bill payments to get the 5% cashback. I have a couple of questions for those who already use it:

- Typically how long does it take for the cashback to show up?

- Do ISP bills (specifically ACT Fibernet) qualify for 5% cashback? Will it come under Utility or Telecom?

Quote:

Originally Posted by Safety is Param

(Post 4723949)

Have you guys considered disabling International transactions on your Citibank card?

Takes less than a minute through Internet Banking (not Mobile banking).

.

|

Thanks for the Tip. It works via App as well.

| All times are GMT +5.5. The time now is 02:06. | |