News

Indian Car sales trends & growth areas

The Indian car industry has grown from roughly around 2 million in 2011 to around 3.12 million in 2018 before dipping to 2.88 million in 2019.

BHPian niranjanprabhu recently shared this with other enthusiasts.

The highest growing segments of the Indian car industry

The Indian car industry has grown from roughly around 2 million in 2011 to around 3.12 million in 2018 before dipping to 2.88 million in 2019. The last year was affected by the move to the BS6 regime for pollution control and this year by the COVID crisis. The growth, if we look at it from a CAGR (Cumulative Annual Growth Rate) perspective, is a modest 6.5% till 2018 and an even more humbling 4.7% if you look at 2019 numbers. In all these numbers what hides, is the mix of certain segments that have seen a secular decline and certain ones that have shown spectacular growth.

Before going forward, I would like to humbly thank this beautiful Team-BHP forum for publishing car sales numbers over the last decade which I have used here to come to these conclusions.

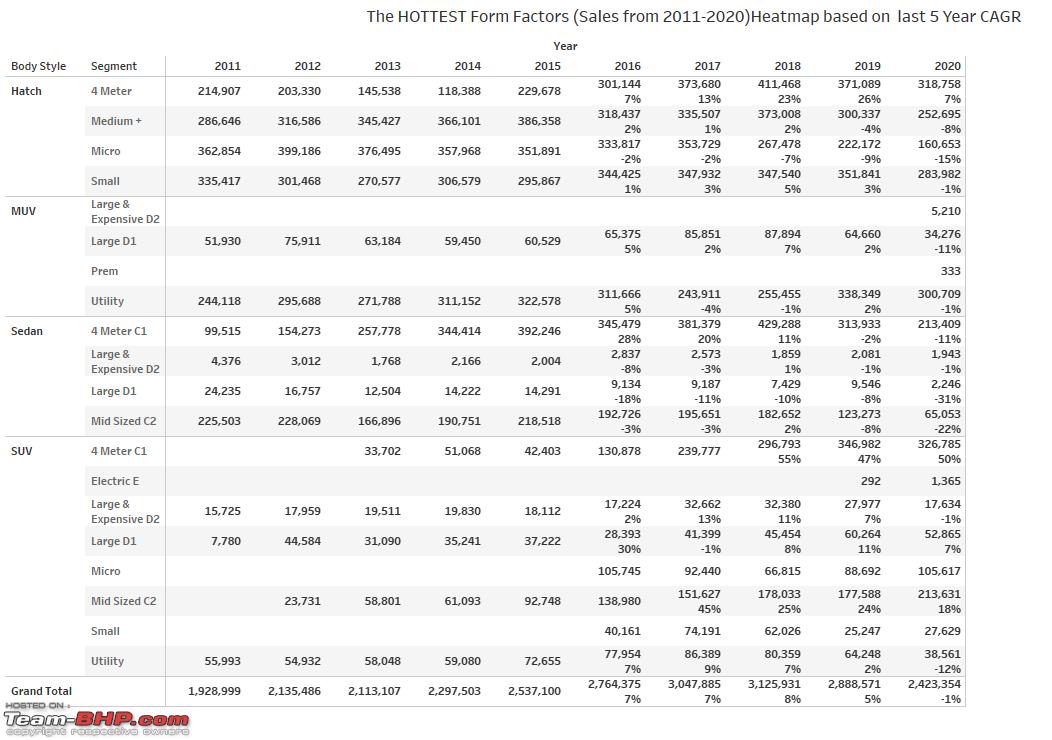

Let us break up the Indian auto sector into 4 form factors:

1. The Hatch segment which is the typical 2-box car that we have all grown up to see starting from the Maruti 800

2. The MUV (Multi Utility Vehicle) or the people movers like the popular Mahindra Bolero and Maruti's Ertiga

3. The Sedan segment that was initially popularized by the Maruti 1000/Esteem and a slew of other brands later on

4. The SUV (Sporty Utility Vehicle) that is today an international craze. I have taken the personal liberty here to recategorize even cars like the S-Presso and the Kwid as Micro SUVs and the Ignis and the KUV as Mini SUVs.

When we see the market share of these 4 segments over the last decade, what shows up is very interesting

The picture that emerges can be summarized as below

1. The SUV market has increased from a measly 4% in 2011 to a whopping 32% in 2020

2. This has happened at the cost of both the Sedans and the Hatchback segments. The MUV market has maintained its share pretty well

3. In terms of volumes, the SUV Segment has contributed to most of the growth (30% CAGR 2011-20)

4. Of all the different kinds of SUVs categorized based on size (not on price, so you will see a Creta priced at the point as the XUV500 but then the Creta is a Medium-Sized SUV and the XUV500 a Large SUV), the ones that are making a massive difference are the 4 Meter SUVs (called also as the sub 4 meter SUVs) like the Maruti Vitara Brezza, Hyundai Venue, Kia Sonet and the like which are growing in volume terms at a massive 47% YoY since 2013-2019. The medium-sized SUVs dominated by the Hyundai Group (Hyundai + Kia) today comprises of 30% of the SUV market and is growing at a very impressive 33%. The small SUVs (I call these SUVs as customers tend to bunch all high ground clearance 5 seater cars as SUVs at some level of perception) like the Maruti Ignis and the Mahindra KUV100 have not really done as well and the mini SUVs like the Renault Kwid and the Maruti S-Presso seem to be holding steady, though the Kwid has been beaten fair and square by the Maruti S-Presso here.

The Hatch Breakup

5. In the downward spiral of the Hatches, the 4 Meter hatches like the Elite 120, Baleno, and the Altroz are growing at positive rates of 7% the remaining hatches have grown at negative rates as seen below.

The Sedan Breakup

6. In the downward spiral of the Sedans, Sub 4 Meter Sedans like the Maruti Dzire and the Honda Amaze have shown a 5 year negative CAGR of 11% , Mid Sized Sedans like the Honda City and Maruti Ciaz have degrown at -22% (2019), Large Sedans like the Skoda Octavia and the Toyota Corolla have degrown at -22% (2019) and Super Premium Sedans like the Toyota Camry and the Skoda Superb have degrown at -1%.

The MUV Breakup

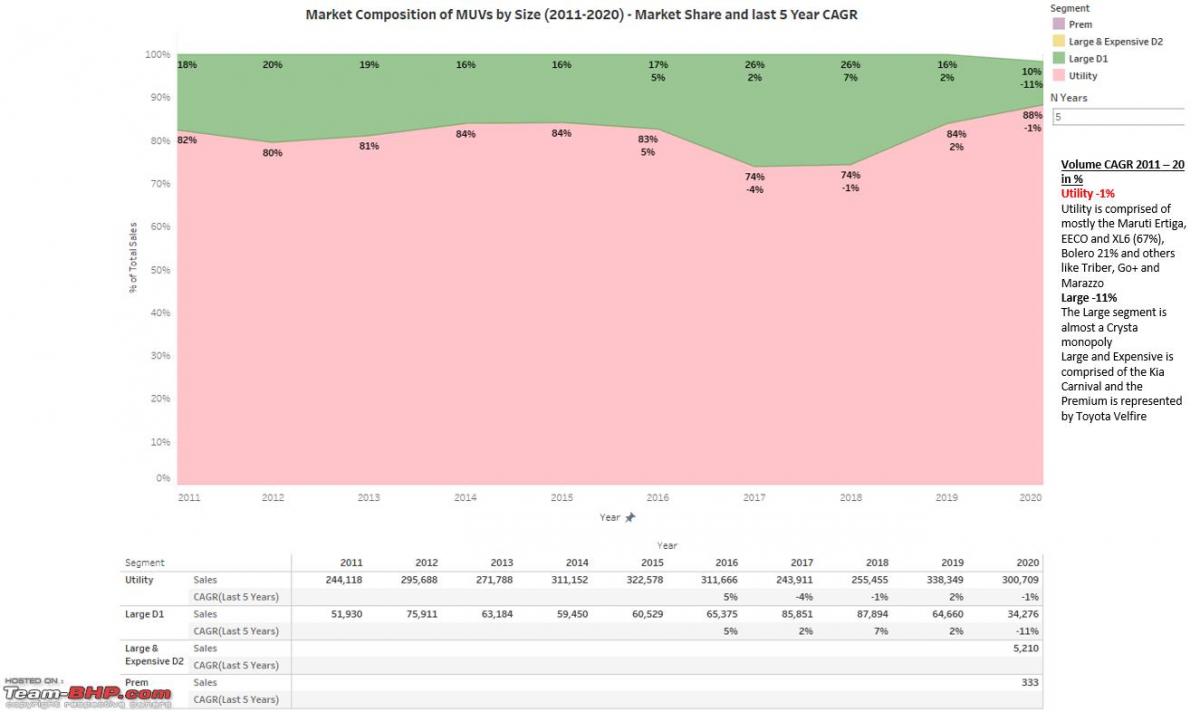

7. In the MUV market, essentially there are only 2 types. The Utility segment comprised of mostly the Maruti Ertiga, EECO and XL6, Bolero 21%, and others like Triber, Go+, and Marazzo totaling 88% and the Large segment ruled completely by the Toyota Innova Crysta (10%) and the new segments of the Extra large represented by the Kia Carnival and the Premium which is the Toyota Velfire comprising the remaining 2%.

Analysis by Price Brackets/Segments

The other way to slice and dice the Indian Car Market is by looking at them from the view of price brackets. For the sake of simplicity, I have created price brackets in ranges of 5 lakhs (100,000 is a lakh). The median price of the range in which the car comes in is used to slot a car in a particular price range. For example, if the latest i20 for example is available from 8-11 lakhs, the car would be put in the 5-10 lakh basket. The Maruti Vitara Brezza for example is available from less than 10 lakhs but goes all the way to 12+ lakhs, so it gets into the 10-15 lakh basket and so on.

When we look at the way the Indian Car Market has grown over the years, it is not just the sheer numbers that are impressive but the way the customer is growing up the ladder in terms of the price segments that she/he desires. Here we see that the lower-priced segments of up to 10 lakhs that comprised 80% of the market a decade ago, today are around 60%. The markets for the 10-20 lakhs segment that comprised around 16% a decade ago are today at 36%.

Let us analyze further what each of these price segment comprises of in terms of form factors.

1. The 5-10 Lakhs market today comprises of hatches some of which are doing very well like the sub-4-meter hatches like the Baleno, the Swift, and the i20. The Baleno, Swift, WagonR, Dzire, Grand i10, and i20 are the top-selling models in this segment. The Baleno/Glanza has shown maximum growth in this segment growing by 24% YoY from 2016 to 2019. Other models mentioned grew in single digits or degree.

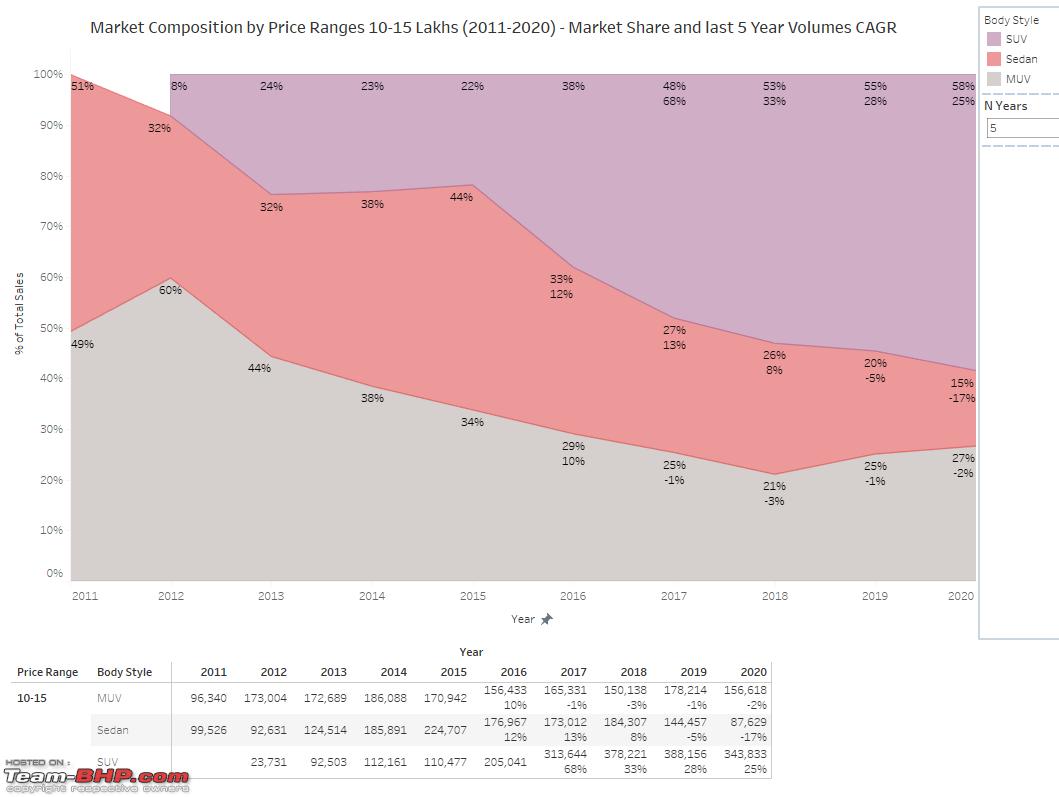

2. A massive 58% of the 10-15 lakh segment today is ruled by SUVs, almost of them the 4-meter variety like the Maruti Vitara Brezza, Hyundai Venue, Tata Nexon, Nissan Magnite, Renault Kwid, and the Kia Sonet. The Renault Duster and the Nissan Kicks too feature in this price bracket. The SUV segment has grown here at a CAGR of 25% in volume terms.

3. The SUVs rule this price band and in 2020, the shares have been a massive 93%.

4. This had been the domain of the Innova for a long time till we saw the advent of the SUVs like the Jeep Compass and the Tata Harrier recently.

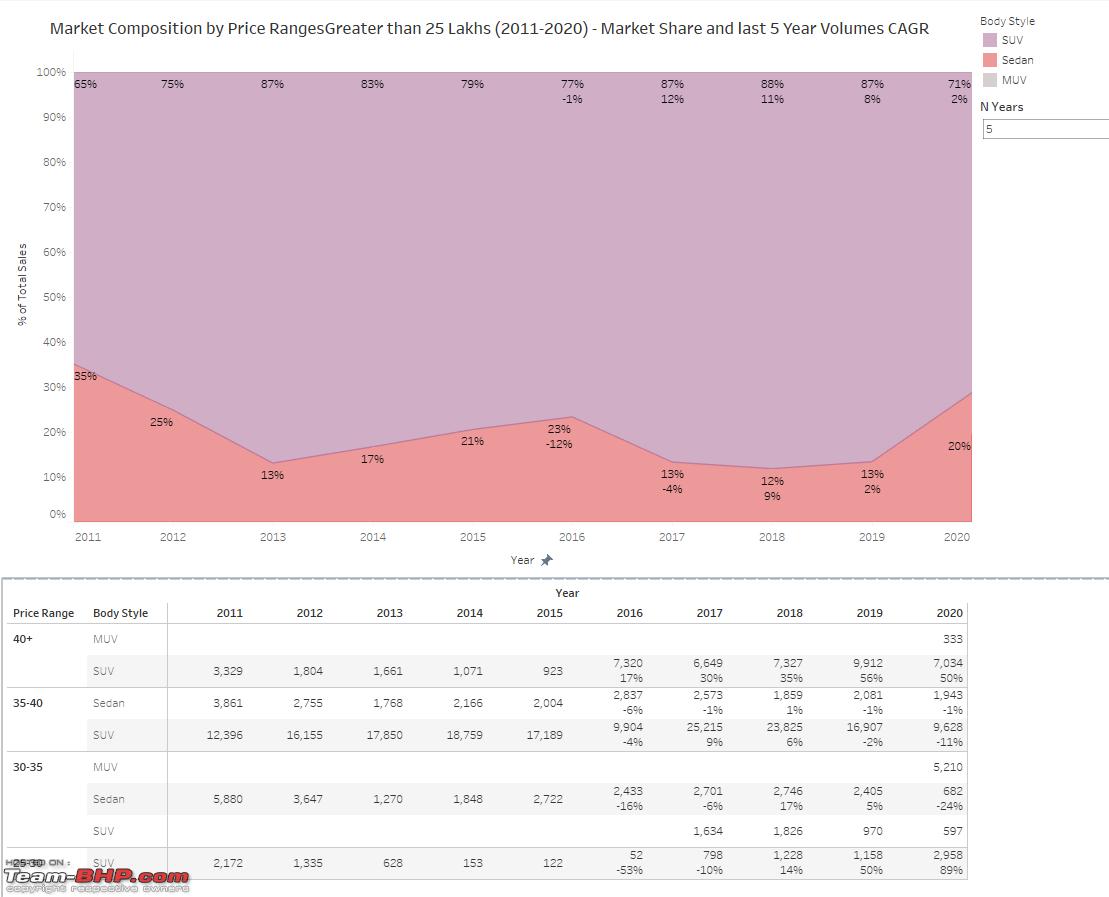

5. This is the domain of the SUVs which hold a share of 71% with the main players being the Ford Endeavor, Hyundai Tucson, MG Gloster, Skoda Kodiaq, the Toyota Fortuner, and the likes. The Kia Carnival is a recent entrant in this segment as a MUV. Having been introduced only in 2020, you don't see it prominently in the charts. The Octavia, Superb, Camry and Sonata are players in the sedan segment in these higher price brackets. Though the volumes here are low at just around 28k, what is delightful to know is that the higher segment SUVs in the 40+ lakh brackets are showing a 5 year volume CAGR of 50%. The Endeavor, Gloster and the Fortuner are the main players here.

Conclusions

1. The SUV is "the" form factor that is driving big time demand across all the price segments. Whether we like it or not, any car that has a raised stance including the S-Presso and the Kwid are seen in the SUV sentiment by consumers and sales personnel too sell them as such. I apologize to the purists who would despise seeing this category getting adulterated so badly! Of the SUVs it is the 4 meter SUV that is showing massive growth of almost 50% volumes CAGR. This is causing issues to the other form factors as well as to the other SUVs as well.

2. Across price segments the biggest loser is the sedan segment. Car companies that are heavily dependent on this form factor for their sales like Honda need to introspect on their portfolio lineups. Even the 4 meter sedans which showed so much promise are now getting compromised heavily because of the demand for the 4 meter SUVs and Maruti which is a leader in this segment with the Dzire should beware. Its 5 year CAGR in 2020 has been an alarming -12%. The segment itself has shown a -11% CAGR in 2020. Though 2020 has been a bad year, the 4 meter SUVs have shown a 5 year CAGR of 50% including this year. This shows the resilience of this form factor in the Indian car markets. This segment breathed life back into the moribund Nissan group which has hit paydirt with the Magnite and Renault with the Kiger. Though many may see this as early days, the segment has been on fire for the last 2-3 years and the numbers below bear raw testimony to the fact. 4 meter SUVs don't show CAGR numbers for 2016 and 17 because the form factor was introduced by the Ford EcoSport in 2013.

3. The safest form factor is the MUV segment which has seen steady growth and a stable market share for almost the entire decade.

Caveat: Earlier models like the Tata Sumo, Nissan Micra etc which found favour in the early part of this decade have not been taken into account. The numbers don't vary beyond a percentage here or there due to these omissions.

Check out BHPian comments for more insights and information.

- Tags:

- Indian

- Other

- Sales & Analysis

- Sales

Find Car News

Just News

About Us