Team-BHP

(

https://www.team-bhp.com/forum/)

I was tempted to get the Axis Magnus card, but finally decided against it.

I have HDFC Infinia currently, which is my primary card.

While choosing credit cards, it is important not to get carried away by the points or rewards - it is important to ask how will you use those rewards? Will you use those because you would have spent the money anyways or simply because the rewards are there and you need to use those to feel rewarded. Infinia rewards and redemption options are super simple and I never felt to do anything out of my normal spends to use those rewards. I think for Axis Magnus, you need to be smart to play the Airmiles or hotel membership game and transfer the reward points etc. to reap maximum benefit.

Secondly, though my annual credit card spends are >15 lakhs, my monthly spend doesn't exceed 1 Lakh regularly. So, I wont have been able to get the 1 Lakh milestone rewards always. I feel for personal use, spending 1 lakh/month is difficult on a regular basis unless paying rent or something similar .

Quote:

Originally Posted by adimicra

(Post 5553117)

I was tempted to get the Axis Magnus card, but finally decided against it.

I have HDFC Infinia currently, which is my primary card.

While choosing credit cards, it is important not to get carried away by the points or rewards - it is important to ask how will you use those rewards? Will you use those because you would have spent the money anyways or simply because the rewards are there and you need to use those to feel rewarded. Infinia rewards and redemption options are super simple and I never felt to do anything out of my normal spends to use those rewards. I think for Axis Magnus, you need to be smart to play the Airmiles or hotel membership game and transfer the reward points etc. to reap maximum benefit.

Secondly, though my annual credit card spends are >15 lakhs, my monthly spend doesn't exceed 1 Lakh regularly. So, I wont have been able to get the 1 Lakh milestone rewards always. I feel for personal use, spending 1 lakh/month is difficult on a regular basis unless paying rent or something similar .

|

I still recommend opting for the Magnus card because, as you mentioned, your expenses are below 15 lakhs. With the Magnus card, you can easily achieve a minimum of 15% returns in terms of miles. Even if you only meet the milestone for 4 months in a year, it still offers significant value. During these 4 months, you will receive a bonus of 1 lakh Edge Rewards (25,000 x 4) along with 24,000 Edge Rewards (6,000 x 4) through the Edge Rewards program. Additionally, if you spend at least 3x to 5x on Gyfter, you can accumulate 1,20,000 Edge Rewards (24,000 x 5x). In total, you will have 2,20,000 Edge Rewards (1,00,000 + 1,20,000), which can be converted to approximately 1,76,000 miles at a ratio of 5:4. These 1,76,000 miles are more than sufficient to cover a return trip in business class for two people from India to Europe. Therefore, even if you spend 4 lakhs over 4 months, you will receive substantial returns. I understand that this may seem too good to be true, but enjoy the benefits while they last.

Quote:

Originally Posted by drdaga

(Post 5553775)

I still recommend opting for the Magnus card because, as you mentioned, your expenses are below 15 lakhs. With the Magnus card, you can easily achieve a minimum of 15% returns in terms of miles. Even if you only meet the milestone for 4 months in a year, it still offers significant value. During these 4 months, you will receive a bonus of 1 lakh Edge Rewards (25,000 x 4) along with 24,000 Edge Rewards (6,000 x 4) through the Edge Rewards program. Additionally, if you spend at least 3x to 5x on Gyfter, you can accumulate 1,20,000 Edge Rewards (24,000 x 5x). In total, you will have 2,20,000 Edge Rewards (1,00,000 + 1,20,000), which can be converted to approximately 1,76,000 miles at a ratio of 5:4. These 1,76,000 miles are more than sufficient to cover a return trip in business class for two people from India to Europe. Therefore, even if you spend 4 lakhs over 4 months, you will receive substantial returns. I understand that this may seem too good to be true, but enjoy the benefits while they last.

|

You calculation is quite off here. Also impractical considering you've put all spends via Gyfter. Also return Business for 2 pax is very very improbable with1.7 Lakh points, also you should know getting two tickets on the same flight , in business , via the points , doesn't work most of the times.

That said, Magnus is still a great card.

Quote:

Originally Posted by Karan_n8

(Post 5554236)

You calculation is quite off here. Also impractical considering you've put all spends via Gyfter. Also return Business for 2 pax is very very improbable with1.7 Lakh points, also you should know getting two tickets on the same flight , in business , via the points , doesn't work most of the times.

That said, Magnus is still a great card.

|

I booked 4 Business Class seats on Singapore Airlines A380 from Singapore to Mumbai for just under 1.10 Lakh points last year before the devaluation.

If you check the current requirements for the same route, you will find it is 43k per head one way, which makes 1.70 Lakh points for 2 people on return journey.

Regarding availability, it is always a hit or miss just like finding cheap fares on the route, but it is a fair point.

Quote:

Originally Posted by drdaga

(Post 5553775)

I still recommend opting for the Magnus card because, as you mentioned, your expenses are below 15 lakhs. With the Magnus card, you can easily achieve a minimum of 15% returns in terms of miles. Even if you only meet the milestone for 4 months in a year, it still offers significant value. During these 4 months, you will receive a bonus of 1 lakh Edge Rewards (25,000 x 4) along with 24,000 Edge Rewards (6,000 x 4) through the Edge Rewards program. Additionally, if you spend at least 3x to 5x on Gyfter, you can accumulate 1,20,000 Edge Rewards (24,000 x 5x). In total, you will have 2,20,000 Edge Rewards (1,00,000 + 1,20,000), which can be converted to approximately 1,76,000 miles at a ratio of 5:4. These 1,76,000 miles are more than sufficient to cover a return trip in business class for two people from India to Europe. Therefore, even if you spend 4 lakhs over 4 months, you will receive substantial returns. I understand that this may seem too good to be true, but enjoy the benefits while they last.

|

Thanks for your response.

I dont think I will be spending so much on Gyftr.

As I said, if someone can maximize the airmiles benefit (till they last), it is great. But I am not in that game, and I dont see anuy major trips for the next 2 years. And by the time 2 years is over, I will be surprised if there is no major devaluation. So, it is not that attractive for me, but I understand that it might be for some other people.

In my previous post, I wanted to point out that I have seen some people get carried away by the rewards game and make unnecessary expenses just to cash in the rewards, which I think does not make sense - it is no longer savings, its actually additional expense. For example, someone say booked a trip to Vietnam or Bali using points mostly for air tickets and hotel. The question is - would he/she booked the trip even without all those points? If the answer is YES, then great. If no, then ...??

Quote:

Originally Posted by adimicra

(Post 5554750)

Thanks for your response.

I dont think I will be spending so much on Gyftr.

As I said, if someone can maximize the airmiles benefit (till they last), it is great. But I am not in that game, and I dont see anuy major trips for the next 2 years. And by the time 2 years is over, I will be surprised if there is no major devaluation. So, it is not that attractive for me, but I understand that it might be for some other people.

In my previous post, I wanted to point out that I have seen some people get carried away by the rewards game and make unnecessary expenses just to cash in the rewards, which I think does not make sense - it is no longer savings, its actually additional expense. For example, someone say booked a trip to Vietnam or Bali using points mostly for air tickets and hotel. The question is - would he/she booked the trip even without all those points? If the answer is YES, then great. If no, then ...??

|

Actually, I posted on Gyftr about how far we can go. I don't expect to spend all my points on Gyftr, but at least in 12 months, we can spend that amount and enjoy some good redemption options. Additionally, domestic options are also great. For example, today I booked a Pune to Delhi flight in business class for just 12,500 Turkish Airmiles and 558 in taxes, whereas a normal economy flight would have cost around 15,000. So, currently, I am 100% sure that this Axis extra benefit will last a maximum of 6 months because banks cannot provide such huge benefits for the long term.

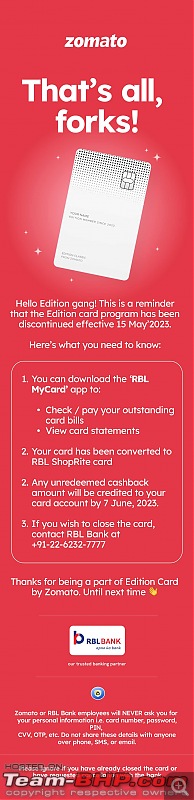

RBL Bank & Zomato end their Zomato Edition Card and all existing Edition cards get converted to RBL Shoprite card.

It was only out of curiosity that I had applied for the Zomato Edition Credit Card when it was launched on the Zomato app. At that point in time, I didn't know RBL bank was the Credit Card's issuing bank. I had a pathetic experience with this joke of a bank while requesting them to correct my name in their records(which was entirely their mistake). The customer care was pathetic and eventually, they asked me to visit the nearest RBL bank branch to get my name corrected (which was in Mysore - nearly 300 kms away). Not seeing any point continuing further, I closed the credit card within two months of its issuance.

I had used four of five times and the cashback was decent on food orders on the Zomato app. And now I see this product itself has been discontinued. I wonder if the pathetic customer service of the issuing bank was the reason behind Zomato ending their partnership or if the cashback rewards was proving to be a loss for Zomato.

Folks who have IndusInd's EazyDiner credit card: How much points does one earn on Grocery and offline restaurant spends ?

And how about Fuel refills - do we earn any points on that or not.

Tips and suggestions on using this card most efficiently welcome.

Quote:

Originally Posted by skanchan95

(Post 5556368)

RBL Bank & Zomato end their Zomato Edition Card and all existing Edition cards get converted to RBL Shoprite card.

|

Did you have your new card shipped/delivered?

Mine says was shipped on 24th May with AWB#, but when tracking on Delhivery it says pickup pending.

Initially after launch it was the best card which offered (If I remember, 5% cashback on all hotel/restaurant spends), but due to some RBI rule they capped it to 1% making it useless, kept it anyway since it was a lifetime free card.

----

Also here's a summary of other cards I've used,

Onecard - Good as a conversation piece, since made of metal attracted attention. Was lifetime free, but replacement cost was 3000 (Had my wallet stolen when I came to know it'll cost 3K to replace this, decided to cancel it alltogether). Reward catalogue wasn't so great, I think they offered 0.5-0.75% in terms of points which could be used to pay off the card bill.

Amazonpay ICICI - Good card with 1% cashback on all spends, 5% on amazon spends if you're a prime member & 3% for non prime. 2% on utility bill spends. Lifetime free so not much of a hassle.

Amex Rewards - Holding it for quite some time but planning to close it as I calculated reward in the form of points is 0.5% (Very poor). Acceptability remains a major issue as many vendors deny taking Amex. The reward catalogue is excellent but too painful to accumulate points. They have a 4.5 or 5.5K yearly fee which can be waived if spending 1.5L in a year

Flipkart Axis (Spouse uses) - Good for shopping on Myntra/Flipkart which offers 5% unlimited cashback. 4% on Uber/Swiggy and a few more apps. Strangely bank gave her the card & denied my multiple applications (not sure why, since I have a decent credit score + age)

I am interested in the Airtel Axis Bank Credit Card - looks like one cannot apply for this card via Axis Bank website or via their agents but rather via Airtel. Anyone who has this card - how did you go about applying for this card?

I have a HDFC Regalia for a while now. Seems there is no upgrade card for me as I am not eligible for the next in line INFINIA / Diners club.

HDFC is offering me upgrade to HDFC Regalia gold which does not look good enough.

Can you guys suggest any other card? - no specific sector spends but reward points wise.

Quote:

Originally Posted by StepUP!

(Post 5556474)

I have a HDFC Regalia for a while now. Seems there is no upgrade card for me as I am not eligible for the next in line INFINIA / Diners club.

HDFC is offering me upgrade to HDFC Regalia gold which does not look good enough.

|

I am also in similar situation. Have Regalia since many years, was offered diners, but declined due to issues in acceptance, especially overseas.

I am keenly wanting to upgrade to Infinia, however yet to be successful in that.

Based on my usage, I feel only Infinia or Axis Magnus are desirable.

Quote:

Originally Posted by vsrivatsa

(Post 5556466)

I am interested in the Airtel Axis Bank Credit Card - looks like one cannot apply for this card via Axis Bank website or via their agents but rather via Airtel. Anyone who has this card - how did you go about applying for this card?

|

They do have a mechanism to apply via the Airtel Thanks App I've heard (If you are an existing customer), a popup or banner should come up stating you're eligible, give it a try. Hard to get these co-branded cards from bank's site.

Quote:

Originally Posted by mpksuhas

(Post 5556481)

Based on my usage, I feel only Infinia or Axis Magnus are desirable.

|

At the risk of sounding melodramatic, sab maya hai. Get a couple of cards that are useful for your regular spends (fuel, travel, online buying etc.) and then forget about it. In the end these are banks that issue you the credit card. They are going to extract their pound of flesh whichever way.

Quote:

Originally Posted by montsa007

(Post 5556377)

Did you have your new card shipped/delivered?

Mine says was shipped on 24th May with AWB#, but when tracking on Delhivery it says pickup pending.

|

I had cancelled my Edition card within two months of issuance and that was probably in January '23 or December '22 because they were unwilling to correct my name without putting into the inconvenience of travelling upto Mysore and wasting my entire day. So no question of me receiving the converted Shoprite card.

| All times are GMT +5.5. The time now is 11:07. | |