Team-BHP

(

https://www.team-bhp.com/forum/)

Quote:

Originally Posted by hondafanboy

(Post 4801678)

I wonder whether the market really gives any meaningful returns to the average investor over the long period. E.g. the freefincal guy managed to get only 2.75% returns after 12 years of investing. He is more than an average investor.

|

If you are following the fincal guy, you would already know that just equity is not a good idea. It is about goal based investment through the right diversification across multiple asset classes - debt, equity, commodities.

The way I see it, investment is a gamble that you cannot do away with. You win some, you lose some.

I am new to mutual funds. Only started investing because I came across them in PhonePe and Paytm Money.

My investments are all debt funds. Because I was checking the fund performances in Paytm money and debt funds had a comparatively better outcome over the last 3 years compared to equity funds.

My investments as of now are

4 lump sum investments:

1. Aditya Birla Sun Life liquid fund - ₹5000

2. Edelweiss banking and psu debt fund direct - growth -₹5000

3. Nippon India gilt securities fund direct - growth -₹5000

4. Idfc banking and psu debt fund direct - growth -₹5000

1 SIP

1. ICICI prudential long term bond fund direct plan -₹1000

Im 31 and still kind of a student. Ill pass out in 2021 and start my career then. So these investments were like a trial run. Im recently married and dont have children.

My goals are to provide for childrens education and that I have money for my retired life assuming I retire at 65.

How should I proceed from here? Whats the best way to save?

I’ve gone through the last many pages and the advice posted by SmartCat and others have been quite beneficial. I’m sitting on a small lump-sum right now as I had taken out my money out of the equity market a few months before the crash. I’m planning to invest in this/coming weeks and then keep investing a major chunk of my salary hereon.

Based on the advice shared (and since it makes sense to me), I’ve decided to invest 50:50 in debt and equity MFs.

Below is how I want to split it amongst the debt and equity funds.

Debt: Liquid (30%), Overnight (10%), Gilt (45%), Banking & PSU (15%).

Investment thesis: I want to keep a low balance in my savings account equivalent to a few months of basic costs. I want 40% of my debt funds to be easily accessible in case of emergencies whereas the rest 60% is for long-term investments (7-10 years, at the very least).

The liquid bonds offer a slightly higher % return and the liquid debt funds that I’ve selected have a large AUM and high % of SOV and AAA bonds, due to which it seems to be as safe as the overnight funds.

Equity: Large-cap (30%), multi-cap (10%), mid-cap (30%), Sectoral – Pharma (10%), International (20%).

Investment thesis: Large-caps and mid-caps have offered good CAGRs over the longer period and hence I want to make majority of my investments into these funds. I want to avoid small-cap funds since I believe that the risk to returns ratio is not that great. I am bullish about pharma as a sector because of the prevailing times and healthcare/medicine is one thing that people don’t compromise on in general. I also want a small exposure towards international funds for diversification, expecting that these markets will do well in long-term. My entire exposure towards equity is for my long-term goals (at least 7-10 years).

Questions:- Any advise regarding the weightages in each of the instruments?

- If you had to invest in the market today, would you still follow a 50:50 split or go with a 40:60 (debt: equity) split as the market has crashed significantly

- Because of the market dynamics, would you consider investing into MFs that invest in Chinese companies?

- Other suggestions/recommedations, if any

Apart from these investments, I would slowly start investing in stocks (which will come out of the equity MF chunk). I do not have other investments except EPF and I don’t want to invest in instruments that have a mandatory lock-in.

Quote:

Originally Posted by prateekm

(Post 4801788)

If you had to invest in the market today, would you still follow a 50:50 split or go with a 40:60 (debt: equity) split as the market has crashed significantly

|

Avoid taking a call based on Nifty levels. 50:50 between equity and debt is the simplest strategy. For better results, disable SIP and make investments once a month manually. Invest in an asset that has lower value (weightage) at the time of investing.

Quote:

Any advise regarding the weightages in each of the instruments?

|

Any further tweaks you make to the strategy (like weightage of each type of fund among debt and equities) will

NOT significantly alter your risk or rewards. I'd recommend multicap funds and g-sec funds primarily. But yeah, it does make sense to allocate some chunk of your debt portfolio to either fixed deposits or overnight/liquid funds because they offer "linear" returns.

Quote:

Other suggestions/recommedations, if any

|

If you want to add some

masala to the mix, you could allocate some percentage (say 10% each?) of your portfolio to international funds and gold funds. However -

- International equity mutual funds have so far performed poorly. It is probably due to high fixed costs. You pay the fund house in India and also the foreign fund house (that actually invests your money)

- Gold has done very well over any time frame, and it especially does well during an economic crisis. After the crisis, it does not fall much in value either.

However, it is impossible to calculate the "fair value" of Gold. You pay the price that is quoted. Nobody can tell you if Gold at Rs. 45,000 per 10 grams is cheap, fair value or expensive

Quote:

Because of the market dynamics, would you consider investing into MFs that invest in Chinese companies?

|

Traitor!! :eek:

No, just kidding. But still, Chinese stocks have not done well because of constant interference in the markets by the Chinese Govt. Till last year, foreigners were not allowed to invest in mainland China (only Hong Kong listed shares were allowed). In a way, the Chinese stock market is a bit primitive - short selling is not allowed and there is no derivatives trading.

But hey, you can give it a shot and let us know how it goes.

Quote:

Apart from these investments, I would slowly start investing in stocks (which will come out of the equity MF chunk).

|

Invest in stocks only if you are interested in the stock picking process. That involves reading up about a company, its financials, valuation, quarterly results and annual report. Most likely, stock picking will

NOT generate higher returns than an equity mutual fund. It's a bit like self-driving (aka stock picking) vs hiring a cab (aka MF investing). At the end of the day, you will get to your destination at around the same time.

But if you are still interested, start from here:

https://www.team-bhp.com/forum/india...ve-sector.html

Quote:

Originally Posted by SmartCat

(Post 4801904)

Avoid taking a call based on Nifty levels. 50:50 between equity and debt is the simplest strategy. For better results, disable SIP and make investments once a month manually. Invest in an asset that has lower value (weightage) at the time of investing.

|

Yes, I plan to manually invest and rebalance the portfolio every month.

:D

Quote:

No, just kidding. But still, Chinese stocks have not done well because of constant interference in the markets by the Chinese Govt. Till last year, foreigners were not allowed to invest in mainland China (only Hong Kong listed shares were allowed). In a way, the Chinese stock market is a bit primitive - short selling is not allowed and there is no derivatives trading.

|

Planing to invest in this international fund:

https://www.valueresearchonline.com/...nd-direct-plan

They invest Chinese companies via a JP Morgan fund (JPMorgan Funds - JF Greater China Fund) which has a bronze rating by Morningstar and a 6000cr AUM. The returns over a 7Y period also seem good.

https://am.jpmorgan.com/lu/en/asset-...d-lu0456846285 Quote:

Invest in stocks only if you are interested in the stock picking process. That involves reading up about a company, its financials, valuation, quarterly results and annual report. Most likely, stock picking will NOT generate higher returns than an equity mutual fund. But if you are still interested, start from here:

https://www.team-bhp.com/forum/india...ve-sector.html

|

Yes, have been following this thread too and also the stock market thread on how to pick stocks. Thanks!

Quote:

Originally Posted by SmartCat

(Post 4801904)

- International equity mutual funds have so far performed poorly. It is probably due to high fixed costs. You pay the fund house in India and also the foreign fund house (that actually invests your money)

|

This is applicable to FoF only as there is a double charge of FMF. International funds directly dealing in target equity markets have comparable expenses as per what I have understood. This is not gauranted though.

Quote:

Originally Posted by prateekm

(Post 4801909)

Planing to invest in this international fund: https://www.valueresearchonline.com/...nd-direct-plan

They invest Chinese companies via a JP Morgan fund (JPMorgan Funds - JF Greater China Fund) which has a bronze rating by Morningstar and a 6000cr AUM. The returns over a 7Y period also seem good.

|

Try to avoid FoF so that you can have lower FMF. Helps in gaining a bit of extra 0.5-1.0% in retuns.

International funds are desirable only from a diversification point of view. Otherwise these are still 'equity'. One benefit that we may gain here is the depreciation of the Rupee against the $. This is given as long as India remains a net importer, which I do not see changing any time in future.

Greater China fund might be looking good as per the current statistics but focusing on only one international country is not what I will prefer. Recently after China was able to supposedly control the pandemic within its borders, their markets have given good returns (for 2020).

Check for something that has a wider basket to choose from - may be an Asia specific fund. Asia has multiple markets of different sizes and a good variety of companies/sectors as well. As SmarCat has put, transperancy and maturity of the Chinese market is a question mark and you can get caught off-guard.

Quote:

Originally Posted by hondafanboy

(Post 4801678)

I have not spent enough time in Equity market but sometimes I wonder whether the market really gives any meaningful returns to the average investor over the long period. E.g. the freefincal guy managed to get only 2.75% returns after 12 years of investing. He is more than an average investor.

|

That was an interesting observation. Out of curiosity, I calculated XIRR for my own investments most of which were made in last 4 years. I am at -1%, which doesn't look so bad considering the fall in equity markets.

One observation I have is that, one needs to do regular rebalancing of portfolio allocations, which is especially important in volatile markets. It automatically means you would redeem some equity funds when their valuations are high and move to liquid/debt. This helps to 'lock in' some of the profits early on instead of waiting forever.

Quote:

Originally Posted by SmartCat

(Post 4801904)

- International equity mutual funds have so far performed poorly. It is probably due to high fixed costs. You pay the fund house in India and also the foreign fund house (that actually invests your money)

|

I think the top few international funds have done reasonably well if we compare their recent performance (3-5 years) with domestic equity funds, but sample size is too small for any meaningful comparison.

Quote:

Originally Posted by SmartCat

(Post 4801904)

Avoid taking a call based on Nifty levels. 50:50 between equity and debt is the simplest strategy. For better results, disable SIP and make investments once a month manually. Invest in an asset that has lower value (weightage) at the time of investing.

|

I have a small doubt. What's a lower value asset? How do I identify them?

Quote:

Originally Posted by professor.march

(Post 4801746)

I’m 31 and still kind of a student. I’ll pass out in 2021 and start my career then. So these investments were like a trial run. I’m recently married and don’t have children. My goals are to provide for children’s education and that I have money for my retired life assuming I retire at 65. How should I proceed from here? What’s the best way to save?

|

Quote:

Originally Posted by professor.march

(Post 4802335)

I have a small doubt. What's a lower value asset? How do I identify them?

|

- Let's assume you have Rs. 2 Lakhs for investment.

- Invest Rs. 1 Lakh in equity funds and Rs. 1 lakh in debt funds.

- Let's say you can save and invest Rs.10,000 per month.

- Remember that equity funds can be volatile while debt funds are mostly docile. If stock market falls, your equity fund value could become Rs. 90,000. But your debt fund value could be Rs. 102,000.

- So now, your equity fund portfolio value is lower than debt fund portfolio value.

- At the end of the month, invest Rs. 10,000 (your monthly savings) in equity funds and zero in debt funds.

- Continue doing this till current value of equity and debt funds is equal.

- If debt:equity portfolio value is equal at the end-of-the-month, invest equal amounts in debt funds and equity funds

Sometimes, equity funds can go up significantly over a period of time. In that case, deploy all your end-of-the-month savings into debt funds till the current value of debt portfolio is equal current value of equity portfolio. This strategy ensures that you will always buy equities cheap. You will never buy equities at the peak.

Let's say you want allocation to be 50-50, but at the time of monthly investing the current weightage is at 48-52. Then you must invest new funds in the lower value asset (which is at 48) to bring it back to 50-50. If you still have spare funds left, then you must invest them equally. I guess this is what SmartCat is suggesting.

Quote:

Originally Posted by SilentEngine

(Post 4802348)

Let's say you want allocation to be 50-50, but at the time of monthly investing the current weightage is at 48-52. Then you must invest new funds in the lower value asset (which is at 48) to bring it back to 50-50. If you still have spare funds left, then you must invest them equally. I guess this is what SmartCat is suggesting.

|

Correct. No need to do rebalancing by selling one asset and buying another. Rebalancing can be done over time with fresh investments.

However, for retired individuals who have no income, rebalancing has to be done by selling the asset that has gone up in value and buying the asset that has gone down in value. This generates cash flow too (but can have tax implications).

Quote:

Originally Posted by SmartCat

(Post 4802350)

Correct. No need to do rebalancing by selling one asset and buying another. Rebalancing can be done over time with fresh investments.

However, for retired individuals who have no income, rebalancing has to be done by selling the asset that has gone up in value and buying the asset that has gone down in value. This generates cash flow too (but can have tax implications).

|

If I may add to the 50:50 strategy - it is very important for everyone to move money once in a while from debt/equity investments to lower risk instruments (Example - FD, PPF, liquid or arbitrage funds, etc). When and how much would depend on individuals impending milestones/goals like wedding, college fees, etc but this is a point which is often overlooked.

If you need 30 lacs for college in June 2025, then do not have your money invested into equity and GILT funds till the very last moment. Keep cashing out to make sure that market or interest rate fluctuations do not spoil your party.

Quote:

Originally Posted by warrioraks

(Post 4802477)

If I may add to the 50:50 strategy - it is very important for everyone to move money once in a while from debt/equity investments to lower risk instruments (Example - FD, PPF, liquid or arbitrage funds, etc). When and how much would depend on individual’s impending milestones/goals like wedding, college fees, etc but this is a point which is often overlooked. If you need 30 lacs for college in June 2025, then do not have your money invested into equity and GILT funds till the very last moment. Keep cashing out to make sure that market or interest rate fluctuations do not spoil your party.

|

Interest rate fluctuations are not a major factor if the gilt mutual fund is held for the long term. To figure out approximately how much you will receive if the fund is held for the long term, you need to look at 'average maturity' and 'yield to maturity' of a gilt fund:

That is, if you invest now, you are guaranteed to get 6.5% CAGR returns in 10 years. But yes, the NAV might go up and down a bit during the journey.

I do agree that a couple of years before an investor's major goals like kids' higher education, children's marriage and home downpayment, it makes sense to pull out funds from both equity and debt funds, and move to overnight/liquid funds or fixed deposits because these offer 'linear' returns.

Quote:

Originally Posted by SmartCat

(Post 4802487)

I do agree that a couple of years before an investor's major goals like kids' higher education, children's marriage and home downpayment, it makes sense to pull out funds from both equity and debt funds, and move to overnight/liquid funds or fixed deposits because these offer 'linear' returns.

|

SmartCat - what is your take on arbitrage funds for linear returns? Because of falling FD rates, arbitrage funds seem to be an attractive option if someone needs to park money for a couple of years.

Quote:

Originally Posted by warrioraks

(Post 4802619)

SmartCat - what is your take on arbitrage funds for linear returns? Because of falling FD rates, arbitrage funds seem to be an attractive option if someone needs to park money for a couple of years.

|

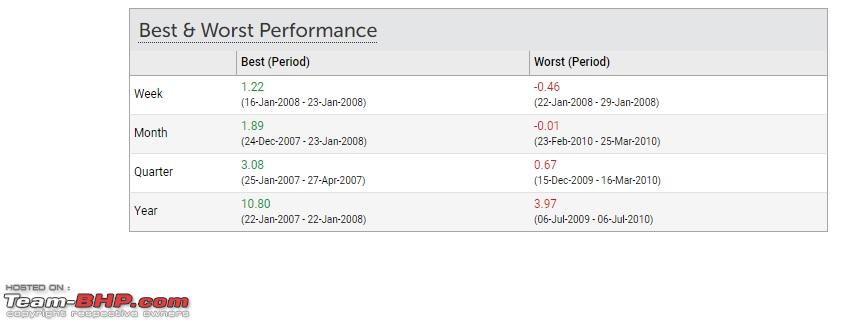

Hmm. It's been a while since I looked up this category of funds. If we look at its performance, the upside and downside in a year is similar to that of a short term bond fund. Eg: The largest arbitrage fund - Kotak Equity Arbitrage Fund - has returned up to 10% in 2007 and -4% in 2010, and around 7.5% CAGR over the long term.

https://www.valueresearchonline.com/...d-regular-plan

This happens because returns are dependent on the difference between stock futures price and stock spot price. The difference can be positive (called premium) or negative (called discount) depending on market conditions. If the difference is positive, the fund makes money. If the difference is negative, the fund loses money.

Meanwhile, let me explain how arbitrage funds works (for those who are new to arbitrage funds).

- One needs to have some understanding of derivatives market (futures) to figure out how arbitrage funds make money.

- Arbitrage funds offer debt fund like returns using equities and futures.

- Arbitrage funds are treated as equity funds for taxation purposes. Because the portfolio primarily consists of stocks (and its respective futures contracts).

- Theoretically, the returns are "risk free". There is no credit risk or interest rate risk, unlike debt funds. Although, these funds use equities and futures contracts, the fund will gain even if a stock falls 10% or goes up 10% in a day.

As mentioned before, returns are dependent on difference between spot and futures prices of a stock. For eg:

However, right now, there is

negative difference between futures and spot prices of most stocks (in this eg, RELIANCE. TCS has a slight positive difference). So the fund manager has no opportunity to make money. But usually, if RELIANCE is trading at Rs. 1588, RELIANCE FUTURES will be trading at Rs. 1592 (for eg). The fund manager will buy 1 share of RELIANCE stock and sell 1 share of RELIANCE FUTURES.

At the end of the month, spot and futures prices will converge. This way, the fund manager collects (1592 - 1588) = Rs. 4 per share as arbitrage. To understand this phenomenon, read this article:

https://www.investopedia.com/terms/c/convergence.asp

| All times are GMT +5.5. The time now is 00:56. | |