Team-BHP

(

https://www.team-bhp.com/forum/)

Quote:

Originally Posted by smartcat

(Post 4363807)

For that, you need to invest regularly every month for something like 10 years or more. Like rental income, dividend income from a company too will rise over time.

|

Makes one think if you really need that new property as an investment. A 1cr flat or 1cr in any of such high dividend yield "decent" companies? :)

Quote:

Originally Posted by Dry Ice

(Post 4364108)

Makes one think if you really need that new property as an investment. A 1cr flat or 1cr in any of such high dividend yield "decent" companies? :)

|

I guess investment in Rs. 1 Cr apartment makes sense under certain circumstances.

- You have put Rs. 20 Lakhs as own capital

- You have taken a home loan for the remaining amt at 10% per annum

- You will receive rental income of Rs. 25,000 per month, and is expected to go up at the rate of 5% per annum

- You expect the apartment value to appreciate at a rate higher than interest rate on home loan. Say 15% per annum.

But the biggest disadvantage of the above is that it sucks all your liquidity. Most of you salary goes into EMI payments, and you won't have anything left for other investments. Plus, if there is a job loss, there is that additional stress of EMI payments.

With investment in high dividend yield stocks, your commitment can be as low or as high as you want. If there is a job loss, you can stop monthly investments. You can even sell some stocks every month so that your cash flows are maintained. For somebody who is worried about job loss and looking at generating multiple sources of income, this is what I would recommend -

1) Put 50% of monthly savings in Fixed Deposit or debt mutual fund. You generate interest income. Funds in FDs can also be used in case of medical or financial emergencies.

2) Put 50% of monthly savings in high dividend yield stocks. You generate dividend income plus capital appreciation.

3) Stay in a rented house for atleast 15 to 20 years. This ensures that job loss does not devastate your finances, and you have ample monthly savings in highly liquid financial assets (stocks + FD).

4) After 15 or 20 years, use the funds available in FDs for apartment downpayment. Take loan for remaining amount.

5) After paying EMIs, continue putting 50% of monthly savings in stocks and the remaining 50% in reducing the outstanding home loan amount. This ensures that you become debt free in a very short period of time.

6) After clearing home loan debt, start building a FD kitty again.

Quote:

Originally Posted by smartcat

(Post 4363807)

Go to www.screener.in and in 'Query Builder', type the following -

Market Capitalization >100 AND

Dividend yield >4 AND

Dividend Payout Ratio >15 AND

Dividend Payout Ratio <100

This lists out all stocks with dividend yield of 4% or above. From the automobile sector, the following stocks offer high dividend yield -

HPCL 5.1%

BPCL 5.1%

IOC 5%

Greaves Cotton 4.3%

.

|

Smartcat, why doesn't it show Coal India when I run this query? Screener otherwise shows a healthy 6.44% Dividend yield.

I bought Maruti shares when they were below 900. My dielma is whether to sell half of them now and keep the other half or sell all at one go and buy them back when the shares dip a bit (I know they won't go back to the level that I bought). I feel the first option is better. Need some advice from experts here.

Quote:

Originally Posted by desiaztec

(Post 4364176)

Smartcat, why doesn't it show Coal India when I run this query? Screener otherwise shows a healthy 6.44% Dividend yield.

|

That's because of a filter I have used - dividend payout ratio has to less than 100%. Many times, companies payout large one time dividend which is greater than the company's profits. We don't want to invest in such companies because dividend payout has to be sustainable. In Coal India's case, the company is paying out dividend from its reserves (because div payout ratio is 130%). However, it is still a decent dividend play.

Quote:

Originally Posted by Ketan T

(Post 4366056)

I bought Maruti shares when they were below 900. My dielma is whether to sell half of them now and keep the other half or sell all at one go and buy them back when the shares dip a bit (I know they won't go back to the level that I bought). I feel the first option is better. Need some advice from experts here.

|

If there is NO market crash, it is unlikely that Maruti stock will fall significantly. Worst case scenario for an expensive but high quality stock like Maruti is that it might be stuck in a range for 3 to 5 years. Basically, the stock might wait for earnings to catch up. So if your intention is to sell now and buy back at a lower price, then it is not such a great idea. If there is a big bear market, Maruti stock could fall, say 50%, but you will also find opportunities in other stocks.

This is what I would recommend -

- Hold on to the stock for now

- Let's assume you had invested Rs. 1 lakh in Maruti and it is now worth Rs. 10 Lakhs

- Let's say you come across a cheaply valued stock in May 2018.

- Sell just enough Maruti stocks to raise Rs. 1 Lakh, and invest this amount in the newly discovered stock.

Quote:

Originally Posted by smartcat

(Post 4366347)

.

If there is NO market crash, it is unlikely that Maruti stock will fall significantly. Worst case scenario for an expensive but high quality stock like Maruti is that it might be stuck in a range for 3 to 5 years. Basically, the stock might wait for earnings to catch up. So if your intention is to sell now and buy back at a lower price, then it is not such a great idea. If there is a big bear market, Maruti stock could fall, say 50%, but you will also find opportunities in other stocks.

This is what I would recommend -

- Hold on to the stock for now

- Let's assume you had invested Rs. 1 lakh in Maruti and it is now worth Rs. 10 Lakhs

- Let's say you come across a cheaply valued stock in May 2018.

- Sell just enough Maruti stocks to raise Rs. 1 Lakh, and invest this amount in the newly discovered stock.

|

Yeah, that would work well. I will wait till I find a good stock to invest in.

@Smartcat:

What's your opinion on Tata motors? I have put in a considerable amount on this black horse but it looks like their turnaround plans are reflecting only in sales figures and balance sheets - but not on market sentiments.

If you advise to hold, then for how long or till what price?

Quote:

Originally Posted by VKumar

(Post 4366713)

What's your opinion on Tata motors?

|

1) Valuations are good

2) Debt is manageable on consolidated level.

3) JLR continues to make profits

4) Indian division has turned around, started reporting profits

5) GST + expected CV scrappage policy means trucking business is expected to grow at 15% CAGR over the next 3 years.

Quote:

I have put in a considerable amount on this black horse

|

If your Tata Motors holding is more than 5% of your portfolio, reduce your holdings. Keep it at max 5%.

Quote:

but it looks like their turnaround plans are reflecting only in sales figures and balance sheets - but not on market sentiments. If you advise to hold, then for how long or till what price?

|

You got it right in the first half. Keep an eye only on sales figures and improving balance sheet numbers. The price action will follow eventually.

Smartcat,

I am wondering why a company like Bosch is floundering in the stock markets. I always considered Bosch as a company with a moat. They have the technology for the fuel pump systems and with the proposed transition to BS6 they should be doing good. The company has also said their consumer facing business in the EV space will be through the listed business. I have seen only a Bosch fuel pump with diesel engines.

Welcoming others also to add their perspective. Planning to add to portfolio.

Quote:

Originally Posted by biju1971

(Post 4367675)

Smartcat, I am wondering why a company like Bosch is floundering in the stock markets. I always considered Bosch as a company with a moat. They have the technology for the fuel pump systems and with the proposed transition to BS6 they should be doing good. The company has also said their consumer facing business in the EV space will be through the listed business. I have seen only a Bosch fuel pump with diesel engines.

|

Maruti, Motherson Sumi and Bosch are all high quality automobile companies. But between 2013 and 2015, Bosch stock went up 3x and was trading at a PE of 60 in 2015.

But when you look at the past history of Bosch, it has grown profits at an average of 15 to 20% per annum. Ideally, if you want the best margin of safety on your investment, you should always buy such a stock at a PE of 15 to 20. Those who are bought the stock in 2015 at peak valuations are sitting on a minor 25% loss in 2 years.

What's happening here is that the stock is waiting for earnings to catch up.

Even now, stock is trading at 40 PE levels which is expensive for 15 to 20% per annum growth company. If you like Bosch, you have two options -

Option 1: Wait for earnings to catch up a bit more. And buy only when it starts trading at PE of 20 or less. Problem with this strategy is that an expensive stock could remain expensive for 5 years or more. You might not get a chance to buy the stock at all.

Option 2: I have mentioned this before - buy a small amount now and add more for every 10% fall. For a high quality stock like Bosch, it is not a big risk because it won't crash like Gitanjali Gems or Punjab National Bank.

Quote:

Originally Posted by biju1971

(Post 4367675)

Smartcat,

I am wondering why a company like Bosch is floundering in the stock markets. I always considered Bosch as a company with a moat. They have the technology for the fuel pump systems and with the proposed transition to BS6 they should be doing good. The company has also said their consumer facing business in the EV space will be through the listed business. I have seen only a Bosch fuel pump with diesel engines.

Welcoming others also to add their perspective. Planning to add to portfolio.

|

Market primarily pays for growth (earnings). For Bosch, the numbers are:

Growth Trends: 10Yr 7Yr 5Yr 3Yr TTM

Sales Growth 10% 12% 6% 6% 6%

OPM 17% 17% 18% 18% 19%

PAT Growth 12% 17% 9% 25% -21%

Avg. PE 28.6 31.2 35.9 42.2 39.5

Long term growth is around 10% while in last few years its just 6%. Meanwhile, PE has grown to around 40 now. That is an unsustainable PE for this kind of growth.

Any future appreciation in price should come from sales and earnings growth now as scope for PE expansion is not there. You can read the Annual Report of the company and check if anything there suggests for an upswing in sales growth.

Quote:

Originally Posted by joslicx

(Post 4367684)

Growth Trends: 10Yr 7Yr 5Yr 3Yr TTM

PAT Growth 12% 17% 9% 25% -21%

|

Great post. Lots of people ignore PE ratio (and hence valuations).

In Bosch's case, when you look at 5 year profit growth, it is 9% CAGR. But when you look at 7 year profit growth, it is 17% CAGR. This happens when profit growth is uneven.

In such cases, you need to look at growth in book value or networth or reserves - because that will be more linear. The growth in networth will be roughly equal to profit growth over a very long period of time. The key assumption here is that dividend payout ratio has not been tinkered with by the company. Growth in networth is Warren Buffet's favorite parameter.

https://www.investopedia.com/stock-a...e-bke0608.aspx

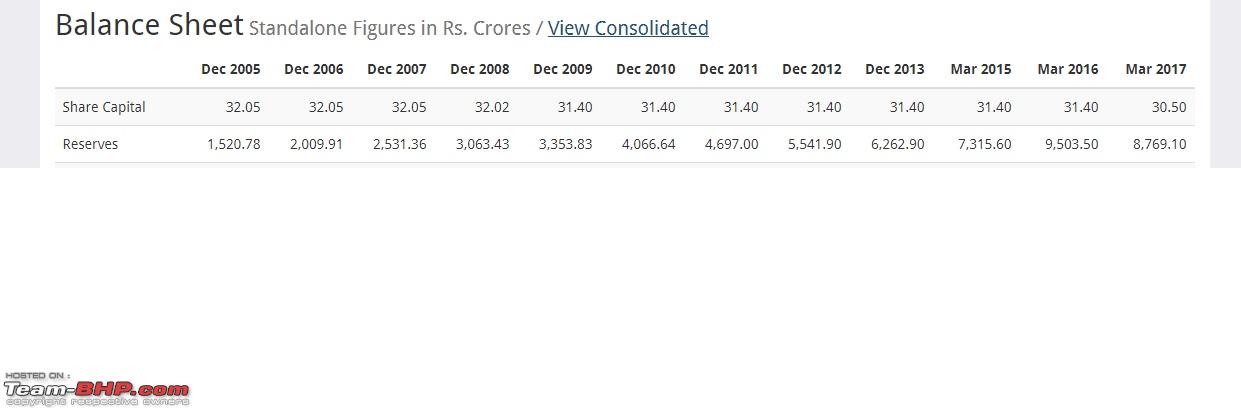

In Bosch's case, reserves have gone up from Rs. 1,520 Cr to Rs. 8,769 Cr. This works out to be a growth of 17% per annum over 11 years. That's why Bosch should ideally be bought at a PE below 20.

Quote:

Originally Posted by smartcat

(Post 4367691)

Great post. Lots of people ignore PE ratio (and hence valuations).

In Bosch's case, when you look at 5 year profit growth, it is 9% CAGR. But when you look at 7 year profit growth, it is 17% CAGR. This happens when profit growth is uneven.

In such cases, you need to look at growth in book value or networth or reserves - because that will be more linear. The growth in networth will be roughly equal to profit growth over a very long period of time. The key assumption here is that dividend payout ratio has not been tinkered with by the company. Growth in networth is Warren Buffet's favorite parameter. https://www.investopedia.com/stock-a...e-bke0608.aspx Attachment 1739009

In Bosch's case, reserves have gone up from Rs. 1,520 Cr to Rs. 8,769 Cr. This works out to be a growth of 17% per annum over 11 years. That's why Bosch should ideally be bought at a PE below 20.

|

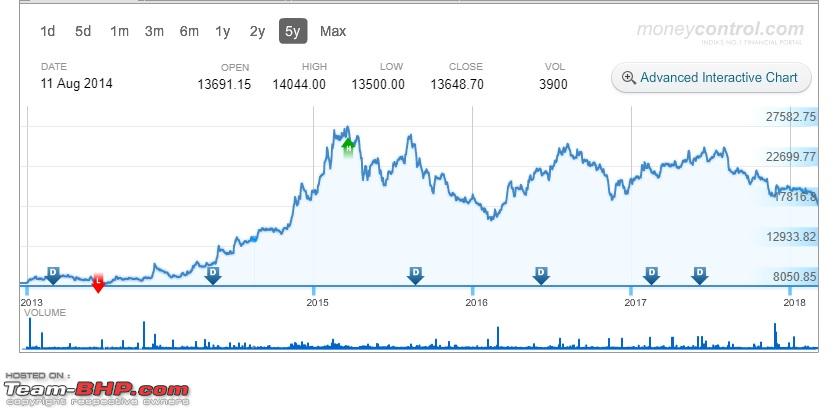

Hi Smartcat, I have invested in Greaves cotton with an average of 133 per share. I am seeing the stock totally underperforming in the current market. Also there isn't much news about the company. I am unable to figure out the present status of the company or the future ahead. Can you please tell me where I can get more information about the company and the stock?

Quote:

Originally Posted by Kratos453

(Post 4370709)

I have invested in Greaves cotton with an average of 133 per share. I am seeing the stock totally underperforming in the current market.

|

Yeah, this has not exactly been hot stock. :)

Quote:

Also there isn't much news about the company. I am unable to figure out the present status of the company or the future ahead. Can you please tell me where I can get more information about the company and the stock?

|

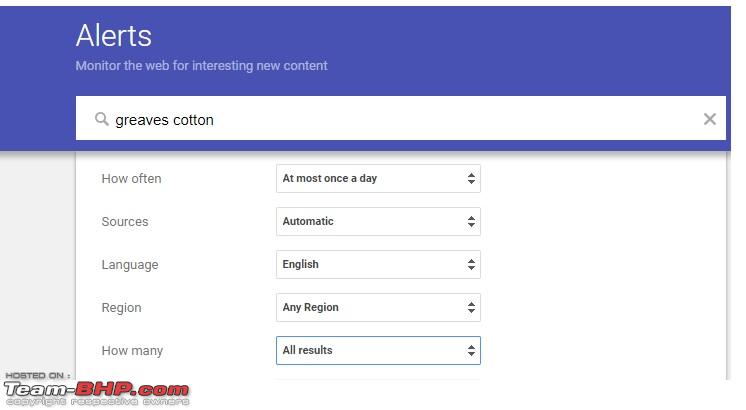

When you are invested in little known stocks like Greaves Cotton, first thing you need to do is sign up for

GOOGLE ALERTS. Set a news alert for "Greaves Cotton" and in options drop down list, select 'All Results'. Whenever there is a product launch, news, results, analyst report or a blog post about Greaves Cotton, you will get an email with all the links.

Your second source of company news is their website. For example, you will discover that company is working on electric mobility solutions and engine oils

Every quarter, go to the company website and check out press releases, management conference calls and investor presentations. Not all companies will such information though.

There is an upcoming IPO of an automobile OEM called "SANDHAR TECHNOLOGIES" opening on March 19th. Any views on this?

The company has a P/E of 43 at the upper band but has total borrowings of close to 5100millon and expects to retire 2750million with the IPO proceeds.

| All times are GMT +5.5. The time now is 08:32. | |