News

Booked a Maruti Suzuki Jimny: Do I take a loan or make upfront payment?

I have the cash for an upfront payment, but does it make better sense to park that money in an FD and take a loan instead?

BHPian mathur2012 recently shared this with other enthusiasts.

I have booked Jimny which is going to be the third car purchase in the last three years. Both of the previous cars were bought on full cash payment.

Although for Jimny I do have the money to buy it at cash payment but I was calculating whether parking that money in FD and taking a loan will be better or buying it at full cash.

I did some calculations and it seems buying a car on loan is better, though I am not sure.

For sake of calculations:

- The car price has been set to Rs 10 lakhs. Also, say I have Rs 10 lakhs in hand to buy the car in cash

- Salary = Rs 1 lakh

- Salary Return = 2.7%(Savings account Return)

- Car Loan Interest = 8.55%,

- FD Interest Rate = 6.5%

- Tenure = 5 years

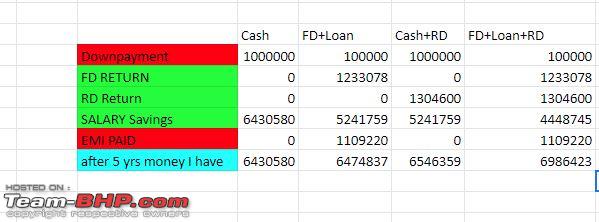

With a down payment amount of Rs 1 lakh, the loan amount will be Rs 9 lakh. Thus EMI for 5 years is Rs 18,487.

Edit: Sorry the last row got obstructed by the watermark, well it states "Money I have with me after 5 years".

You can see at end of 5 years I have 40K more in my hand if I purchase the car on loan, not to mention that this is a minimum return. The actual returns can be better e.g. at the moment I am getting 6.75% FD ROI for 5 years( But I only used 6.5% in my calculations)

In fact, this money can also be invested in MF for much better returns. Also the fact of having Rs 9 lakh in hand and not being broke.

As per the above calculations, loan over cash seems better but I have a feeling I am wrong somewhere, Can anyone shed some light on where I am miscalculating anything?

PS: There's no issue of any tax on FD return here as the FD is/will be in an account which doesn't come under taxable income. So the returns will be tax-free.

Edit: What if FD+RD+Loan?

Well, here it is;

Seems like a car loan is the better financial decision what do you guys say?

However, we if buy the car in cash and instead of paying EMI we use that EMI money to invest in RD then it's a different story.

Here's what BHPian Lobogris had to say on the matter:

There seems to be an error in the calculations. Firstly, you will have to pay Rs 1 lakh as down payment. So you will only have 9 lakhs left to invest in the said FD. So that will reduce the return on the FD. When you are getting 6.5% but paying 8.5% to the bank, how can you expect to earn more by paying an extra 2% in interest? If you simply kept paying yourself each month, you will do better and not have to deal with the hassle of a loan. Personally, I never take a loan to buy a car or even a home as the hassle is not worth it for me. Even if I somehow end up saving 40k over several years, that is a relatively small amount considering the hassle. The only exception is if you are trying to build up your credit status or have no other funds available and thus want to keep those 9 lakhs as a cash reserve. Personally, I would still use those 10 lakhs and start building up my reserve again each month.

BHPian mathur2012 replied to this with:

I too also thought there must be some mistake in calculations but it seems there aren't.

Firstly about the 1 lakh down payment and 9 lakhs left for FD, you said. Well the FD returns are calculated on 9 lakhs only.

2nd I also thought how can I get more return when I get 6.5% on FD and pay 8.5% on loan. The answer to this is that a 6.5% return is on 9 lakhs which remains constant for 5 years. Whereas the loaned amount(principal) on which 8.5% I need to pay interest keeps decreasing every year. Thus if we calculate CAGR for overall loan tenure it comes to around 4.5%-5% whereas I am getting a 6.5% return.

That 40k is the least amount saved, with the current 6.75% FD rate or investing in long-term MF we can get much more savings.

But, I agree with you, just for sake of mental peace and no hassles and liabilities I too have never opted for a loan in my life.

Here's what BHPian red_nemesis had to say on the matter:

Thanks for sharing this interesting analysis, but I beg to defer.

There are 2 fundamental flaws in your comparison.

First, you are comparing FD returns against the loan repayment but you are not paying off the loan from the FD amount.

You should compare the loan option against the source of your EMIs, which would be salary as per my understanding of your post. Hence, you should compare the post-tax returns on the equivalent amount from salary if you had invested it instead of paying the EMI (which is RD in your case). So, in the case of RD, if you calculate returns considering an upfront payment of 1 lakh and interest loss on that it would come out about negative 40-60k as you calculated. Hence, not better financially.

Second, you are totally disregarding the time value of money. 10 lakhs in hand at the end of 5 years could mean anything. It could be 0 until 4 years and 10 lakh at 5-year mark OR 9 lakh at end of year 1 and the tenth coming only in the 5th year. Both are drastically different from each other.

So basically, paying cash might be better financially (only because your alternate returns are less than the loan rate). But loan gives you extra cash at hand which can come in handy in an emergency, or can be invested in other options to earn better returns than a loan.

I would personally go with a loan, probably with a little more down payment (30-40%) of value with an option to prepay and enjoy the assurance that comes with extra liquidity.

But to each his own.

Check out BHPian comments for more insights and information.

Find Car News

Just News

About Us

Buy & Sell

USED CARS