News

Luxury car sales analysis in India for F.Y 21-22

The Indian luxury car market is going through a recovery phase after COVID-19 induced massive de-growth in 2020. Luxury car prices have also gone through the roof in the recent past.

BHPian pqr recently shared this with other enthusiasts.

FY 2021-22 Indian luxury car market analysis

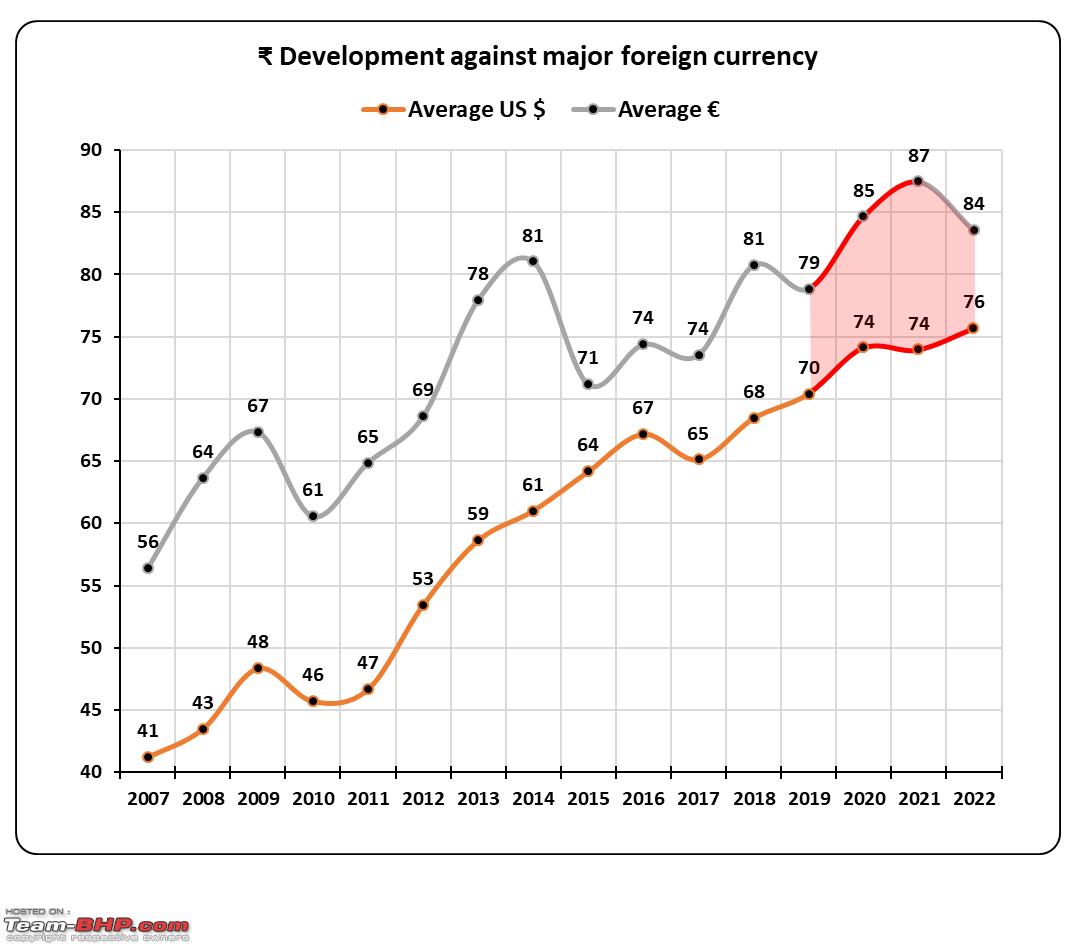

The Indian luxury car market is going through a recovery phase after COVID-19 induced massive de-growth in 2020. Luxury car prices have also gone through the roof in the recent past. Adverse foreign exchange rate development in the recent past is one of the major reasons, as all luxury cars in India comes through CKD (completely-knocked-down) or CBU (completely-built-unit) route. Impact for different players is different, based on the currency their parent company chose to bill cars in India and the effective currency hedging policy their treasury department adopt. Euro has cooled down in 2022 but USD is still on the boil.

On top of that, input cost inflation in recent times and the rise in the price of precious metals used in emission control equipment added to the misery. Chip shortage added to supply-side constraints as well. However, despite all adversities, demand came back in the luxury car segment as well and most players are doing well.

FY 2021-22 Industry players

Note: Data for this analysis was shared by BHPian CEF_Beasts. Many thanks to him for sharing the data.

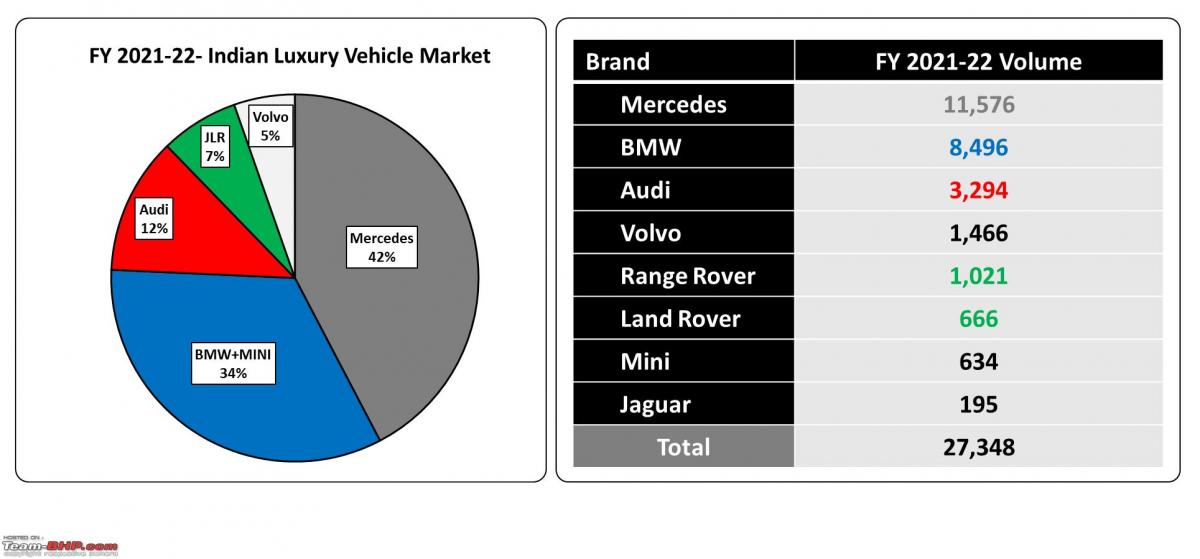

- Mercedes and BMW have an upper hand due to the availability competitively priced diesel engine products in the BS6 era

- Mercedes commands lion share of the Indian luxury car market with dominance in the sedan and SUV segment

- Despite similar product line up as Mercedes and diesel engines availability, BMW+MINI is distant #2 in the market

- Audi with petrol sedans, some CBU products and generous discounts was able to capture a 12% market share

- Within the JLR portfolio – Jaguar is struggling, Range Rover sold more cars than the Land Rover brand

- Volvo with petrol only strategy transition with refreshed product line up stood at a respectable 5% market share

Top 20

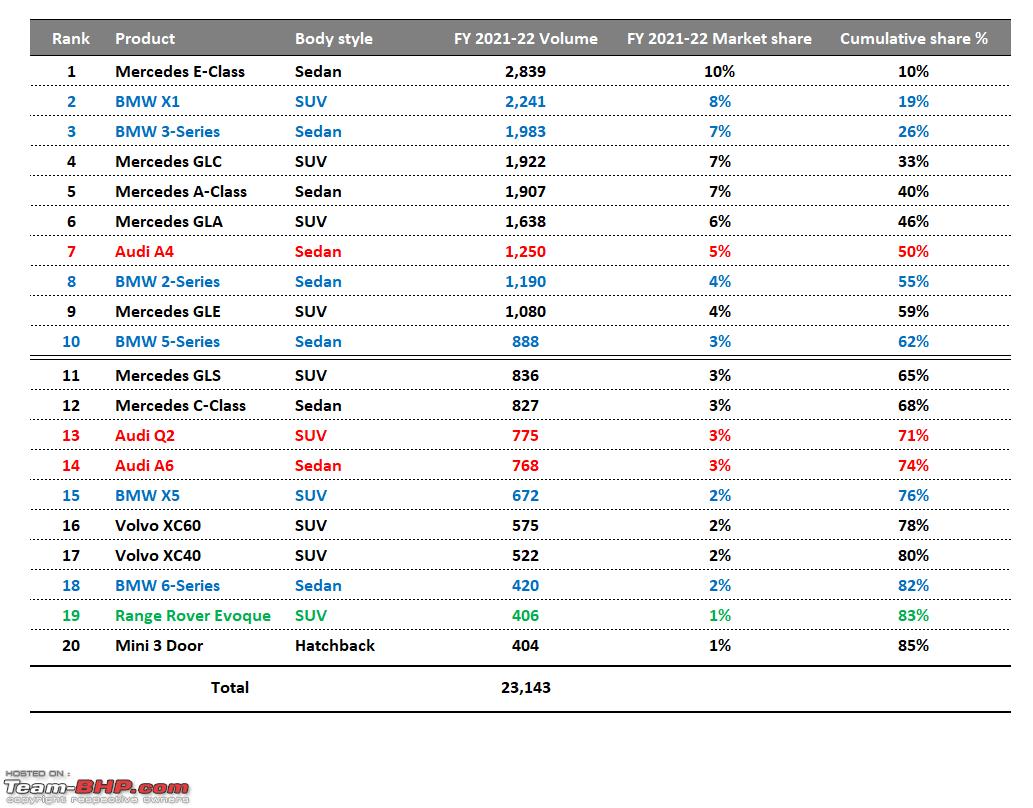

- The top 10 products cover 62% market and the top 20 together 85%

- Mercedes E-Class LWB is best-selling product in the Indian market, way ahead of everyone

- BMW fielding twin products under 3-Series nameplate has 7% market share with #3 position

- The top 10 slots are occupied by 6 sedan products and 4 SUV

- Mercedes has 5 products in the top 10 rankings each commanding a significant chunk

- BMW is just behind Mercedes with 4 products in the top 10 categories

- The highly discounted Audi A4 was able to occupy a single slot for Audi in the top 10 ranking

Products

Mercedes

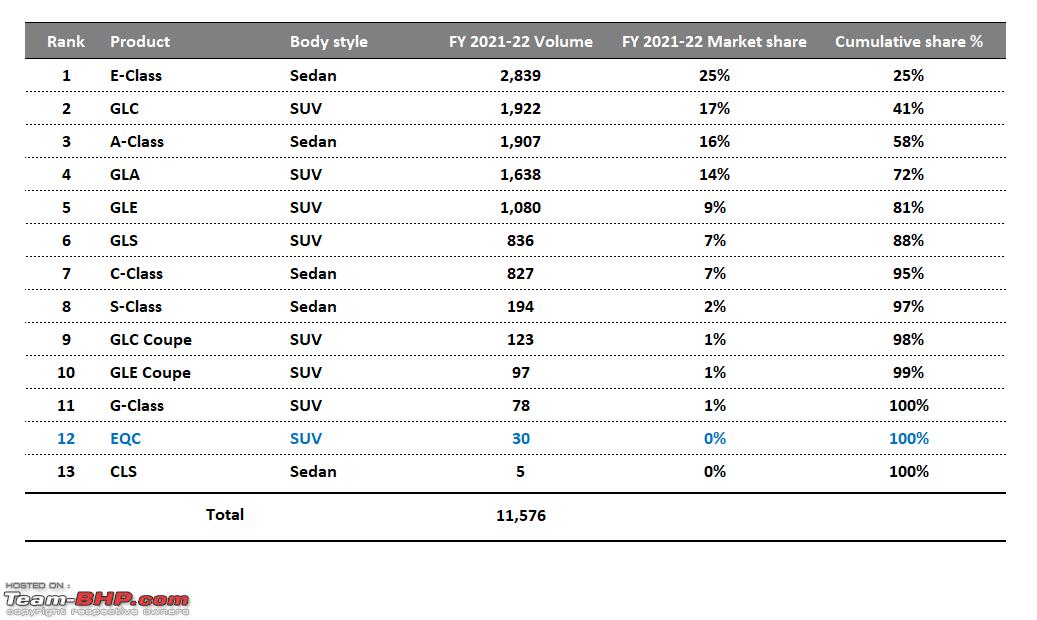

Mercedes has quite a good lineup of products in the Indian market, competitively priced diesel engine products and nearly every product is doing quite well. C-Class despite in its fag end of PLC sold in good numbers. No wonder why Mercedes Benz India MD is bullish on historically selling the most number of cars in 2022. The absence of diesel-powered Audi SUVs and sedans is also helping Mercedes's cause here. Overall it seems in India - people prefer luxury and in-cabin space over the sportiness attribute of products.

- E-Class is the anchor product with the highest portfolio share of 25%

- Nearly 6 year old GLC is doing quite well

- New A-Class has got good traction with a longer wheelbase

- GLA 2nd-generation is doing better than its predecessor

- GLE and GLS are the respective sub-segment leader

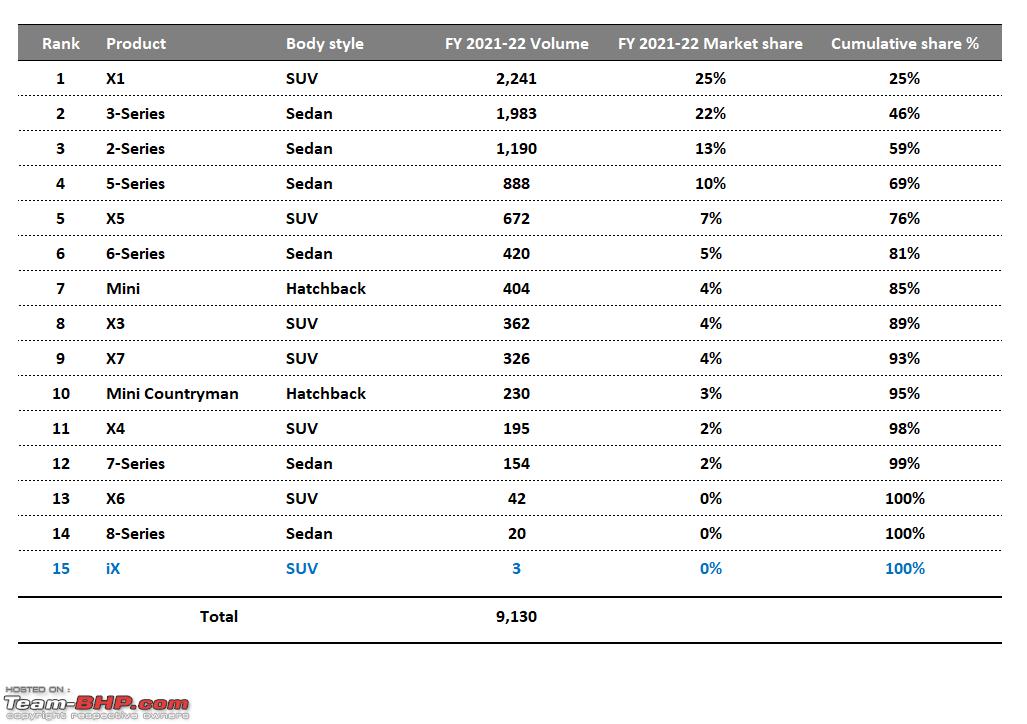

BMW+MINI

Unlike Mercedes, the BMW portfolio’s higher slots are occupied by lower-priced entry-level products. Does it also indicate that chauffeured Indian audiences prefer luxury quotient over sportiness credentials? If so then BMW needs to focus on a softer suspension setup in the Indian market.

- Despite age, X1 contributes 25% of BMW’s portfolio

- Just like the predecessor 3 Series GT, LWB 3 series contribute massively to BMW’s portfolio

- BMW’s SUV products don’t have much steam in numbers, with the expensive X5 doing better than X3 and X4

- Mini is doing pretty well in the niche segment cut out for self

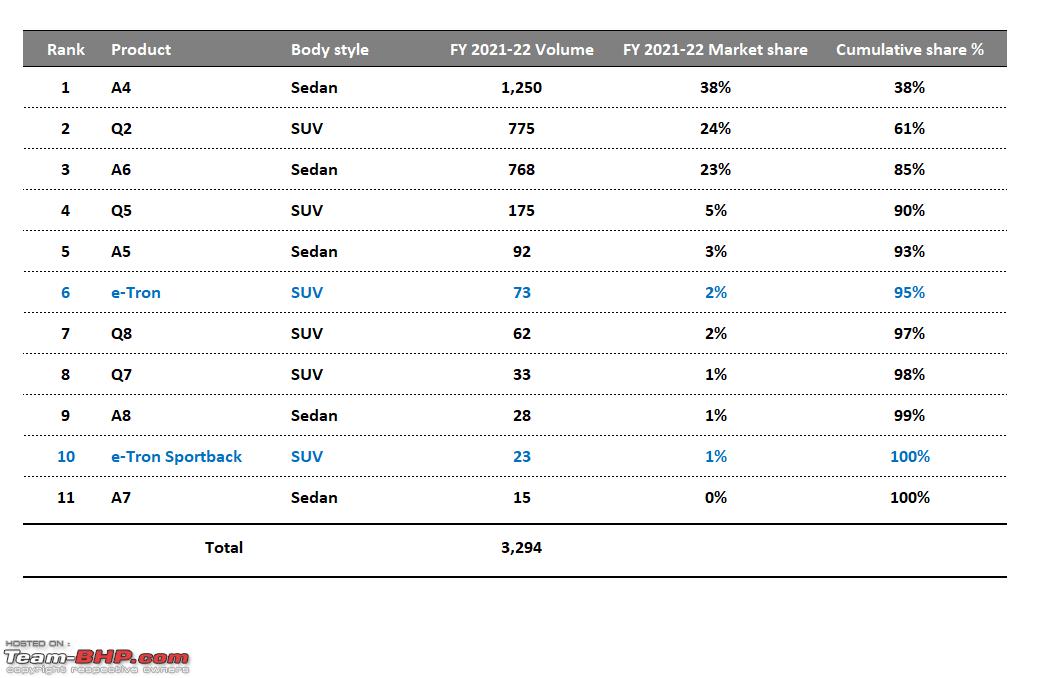

AUDI

Audi was struggling throughout the year with its exorbitant priced CBU Q2 and petrol-only A4 and A6 being sold at huge discounts. The absence of Q5 and Q7 for the larger part of 2021 also compounded the problem. So nothing much to conclude from Audi’s weak position in the Indian market, which is apparent.

The only solace for Audi was the good acceptance of BEV products. Audi has better potential in BEV segment, only if they bring entire BEV SUV products through the CKD route before others, as it already has a competitive BEV SUV portfolio globally, with good technology in every improvisation cycle with partners like Porsche and Rimac.

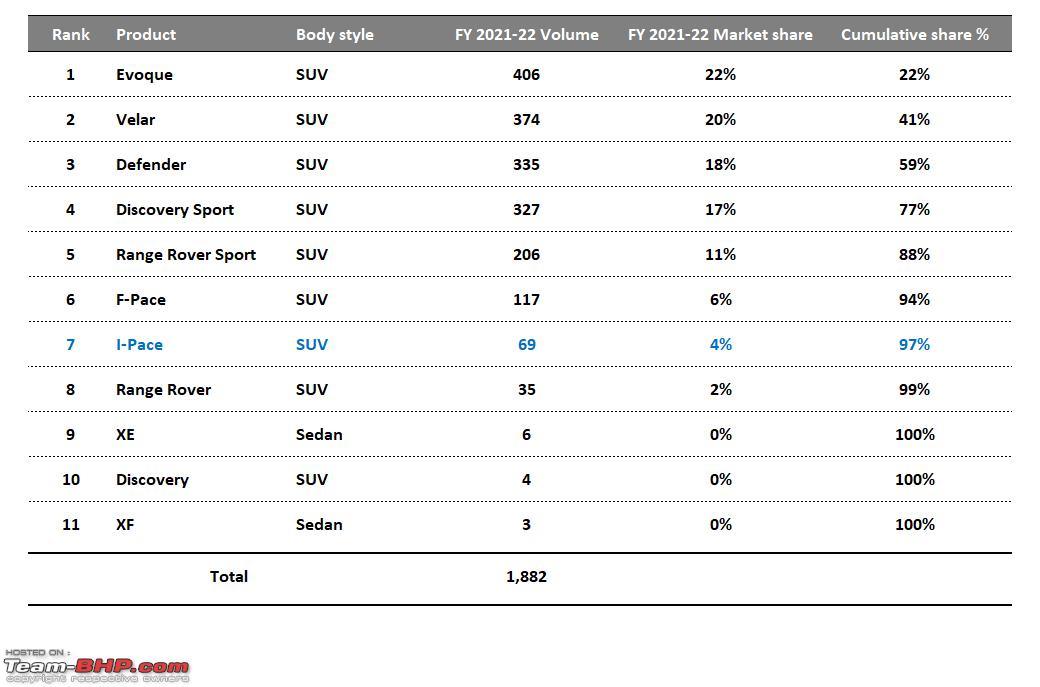

JLR

JLR is kind of lost in Indian market. Jaguar sedans are in dire straits with discontinued XE (unofficially) and CBU only XF. However, Range Rover products have shown good potential among Indian audience craving for luxury. Range Rover brand became new darling of celebrities from movie and cricket world. Despite high price, Range Rover Evoque and Velar are regarded as luxury accessories in urban India.

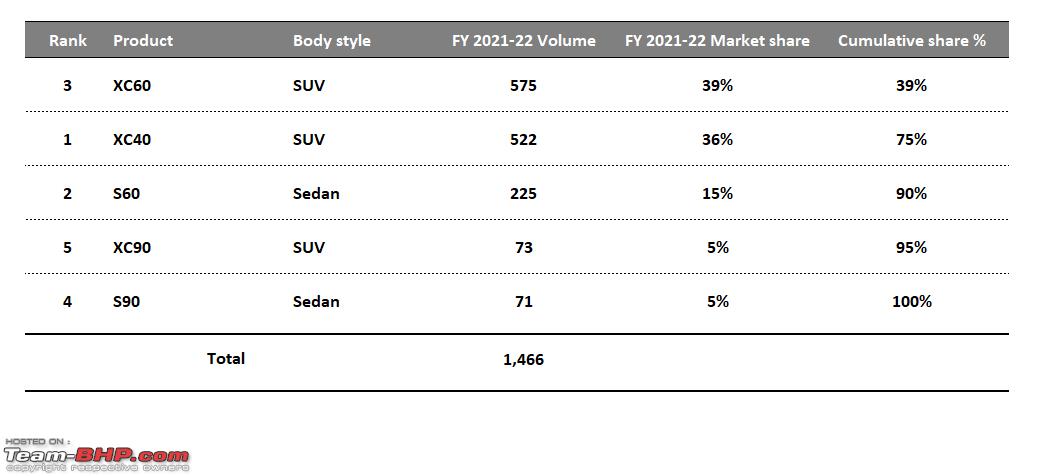

Volvo

Volvo was in the petrol engine transition phase and now has all petrol-powered cars in India. New design language makes them a looker and helps in better acceptance among an urban elite. Volvo is the only luxury car maker in India to offer ADAS features from entry-level XC40. Still, they have a lot of catching up to do with Germans in terms of outright performance and interior finesse. They also need to be more vocal in marketing, their cars have ADAS features, but never gone aggressive with its marketing.

- SUV products are doing better than sedans

- The expensive XC 60 is selling more than the entry-level XC40

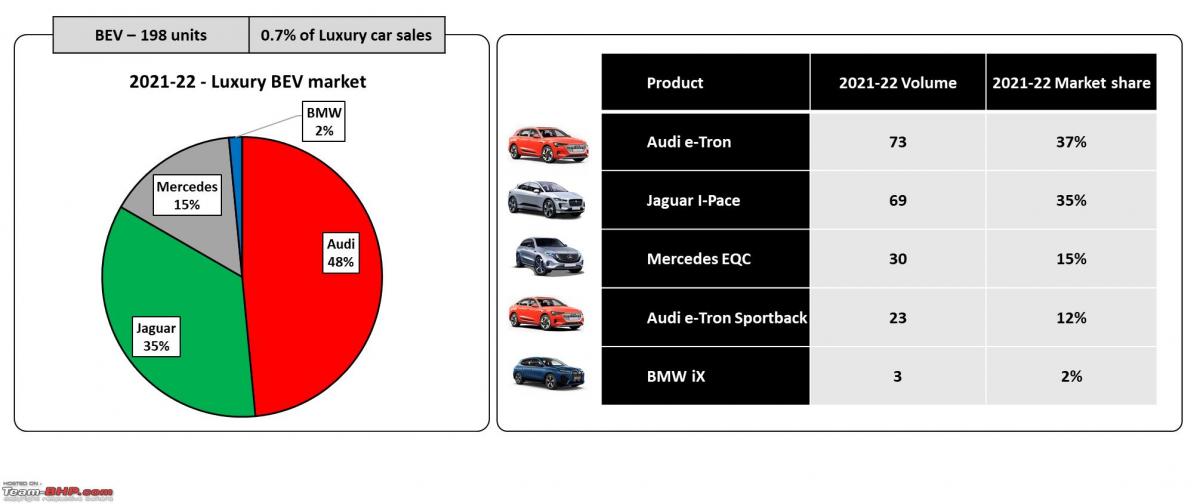

BEV Products

- Luxury carmakers sold 198 CBU BEV in India that contributes 0.7% of the Indian luxury car market

- Audi has an edge in the race of luxury BEV with 96 cars sold in just under 9 months

- Jaguar too had a considerable share of 35% with I-Pace available in three variants

- Mercedes started feeling the heat with the arrival of other competent BEV products and were able to sell a mere 30 low slung, uninspiring EQC

- That’s the reason why Mercedes silently reduced the price of EQC in January 2022

- BMW sold a mere three iX since launch in December 2021 till March 2022, which seems to be cars for launch and media drive activity

- It seems as if it was a quick BEV namesake launch and they are not ready to deliver cars to customers in India as yet

- In the BEV market nobody has a first-mover advantage, the best product will take the cake irrespective of the timing

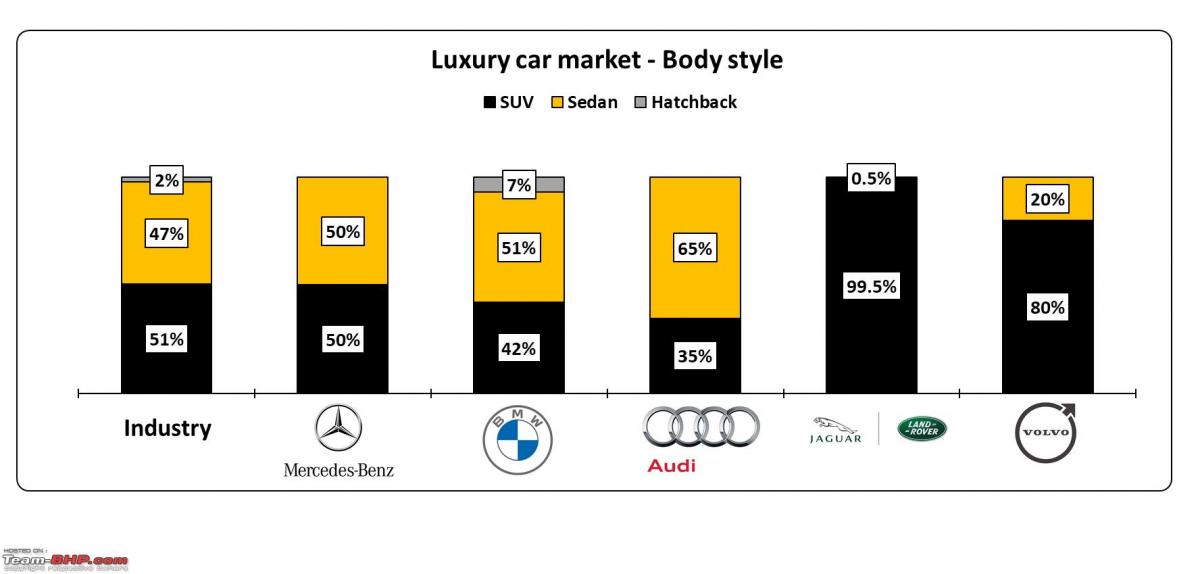

Body-style

- Unlike mass-market segment, chauffeured around sedan body-style still hold quite a big share in luxury car market

- Mercedes’s body style split is 50-50 due to strong sedan portfolio

- Besides X1, other SUV don’t have big contribution in BMW’s otherwise strong looking SUV lineup

- Audi was largely relying on CKD A4 and A6 in 2021, and Q5 and Q7 production started quite late in 2021

- Jaguar’s sedan portfolio is nearly dead with a handful of XF sales, recently with a complete switchover to the CBU route

- Volvo has a good SUV lineup now and so is the strong SUV mix in the portfolio

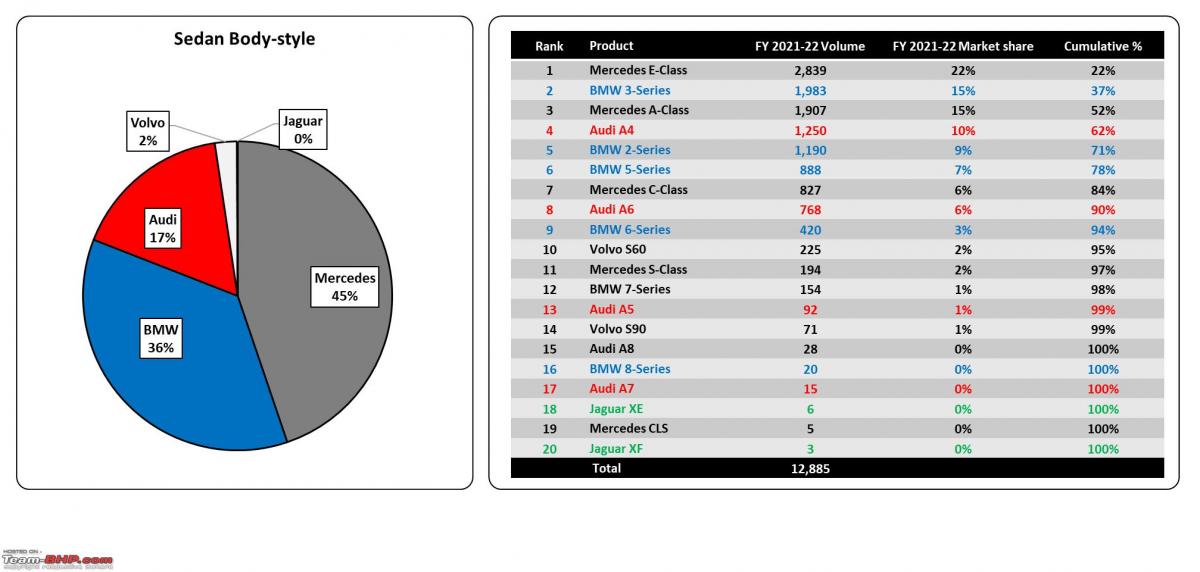

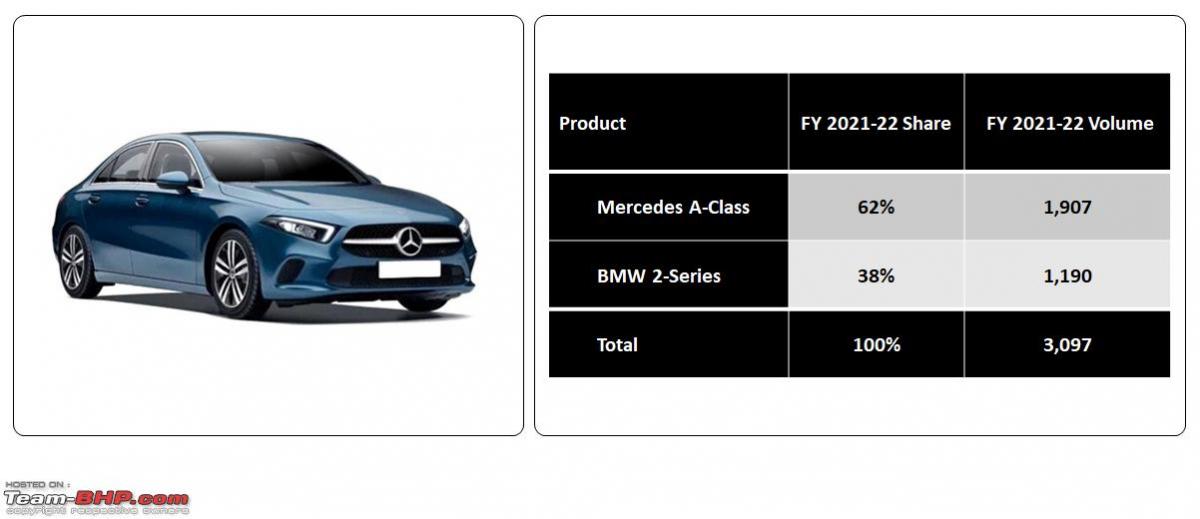

Sedan

The car that started the luxury car phenomena in India is the king of the sedans – the E-Class

- 3-Series LWB is the flag bearer for BMW in the sedan segment

- A-Class got its 3rd position due to extended wheelbase

- Audi secured 4th position by stretching A4’s price point and discounts

- Lack of space at the rear limits the BMW 2-Series' appeal

- 5-Series seems to be struggling to keep up with the LWB E-Class

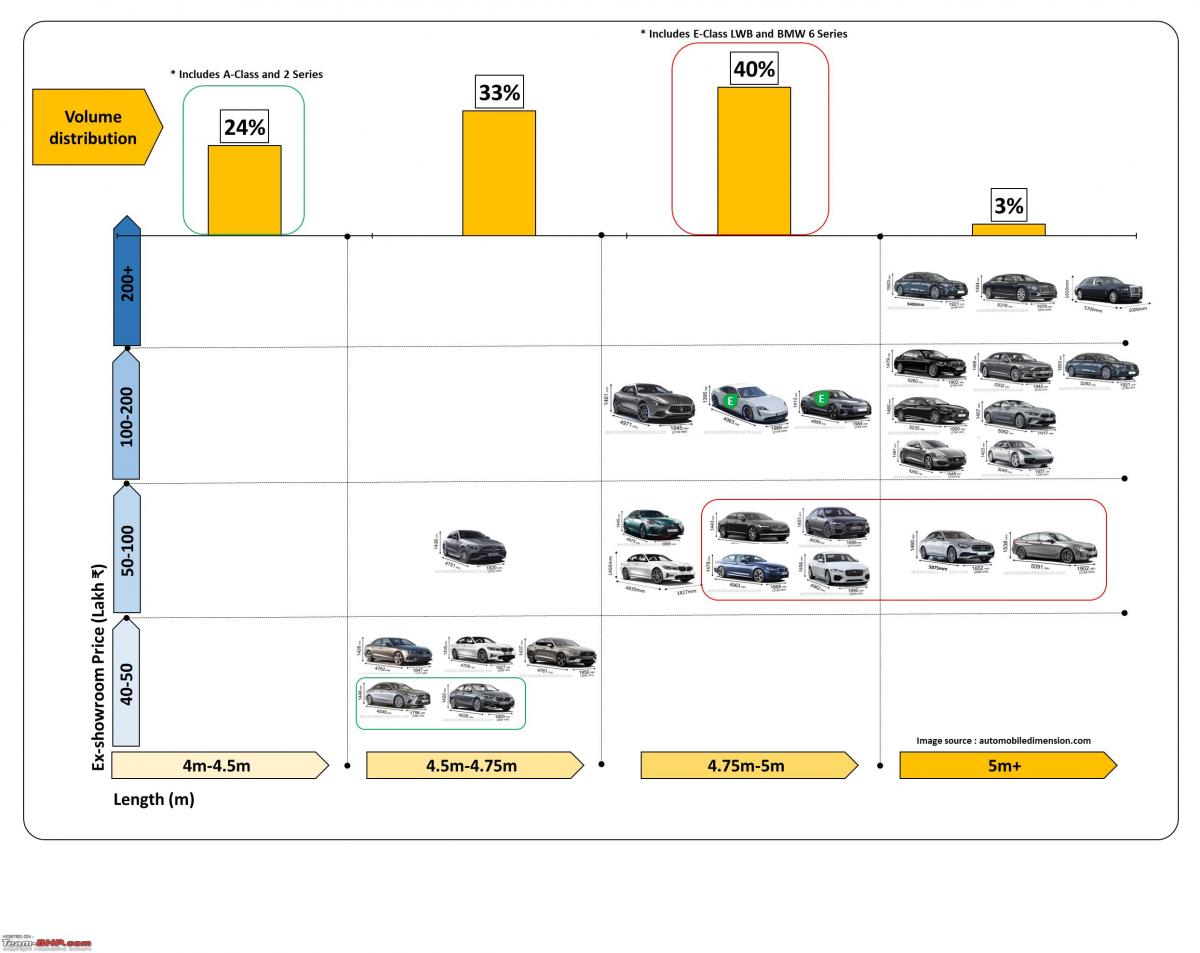

Sedan segments

To get better understanding of the sub segments, a two dimension array was created. Ex-showroom price on Y-axis to show positioning and length on X-axis as proxy to in-cabin space. Some products are still misfits, and some products deliver extra value by being different as in the case of Mercedes Benz E-Class. In case of sedan higher priced but bigger sedans have a major market share, and the majority of them are chauffeured.

Sedan sub-segment

- A-Class with a longer wheelbase than its predecessor has an edge over 2-Series

- Change value proposition means better traction for A-Class

- BMW has fielded two products -3 Series and its LWB version to counter Mercedes

- Petrol A4 is underpowered to take on 3-series so it has to make up with hefty discounts

- C-Class in the last phase of PLC shows up better fight with its well-aged exterior design

- Volvo S60 remains quite well equipped and underrated car in the segment

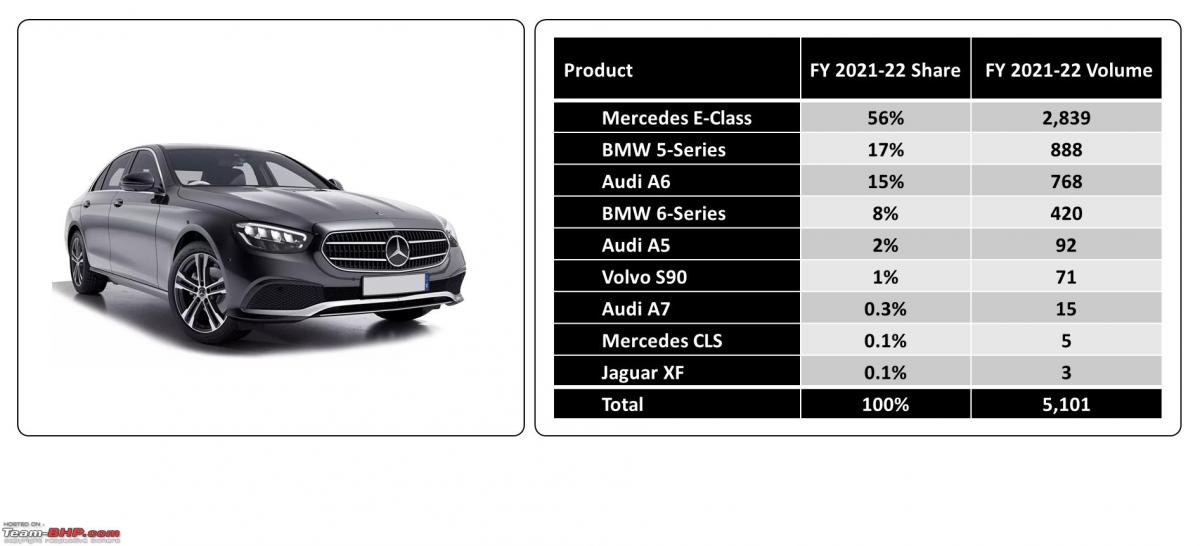

- E-Class LWB was a game-changer, and it maintains its leads with a 56% share

- BMW has to field two products - 5-Series and 6-Series GT to counter E-Class LWB, but in vain

- A6 though not too old, has to live with discounts

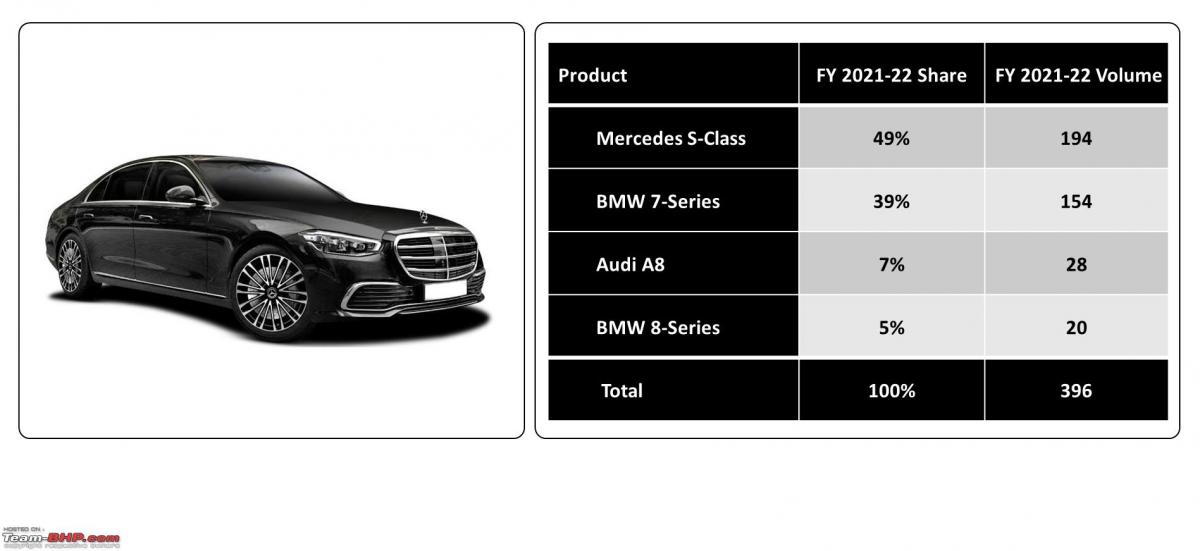

- Best car in the world – S-class new generation was launched in October 2021, thus losing some volume in transition, remain the segment leader

- BMW 7-Series came close but will find it difficult in next full year run

- CBU A8 is just a drop in the ocean

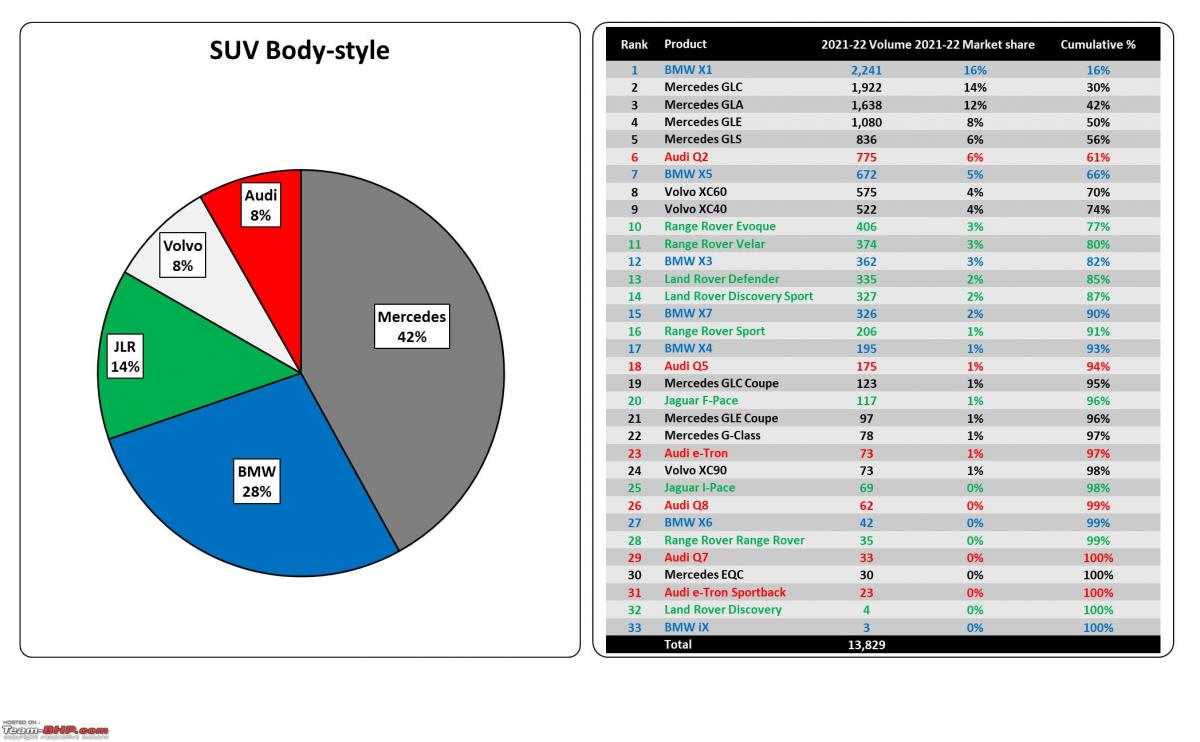

SUV

- BMW X1 remains the best-selling luxury SUV in the country

- Rest all the slots are competitively occupied by Mercedes

- Volvo got a toehold in the top 10 SUV slot

- Range Rover made it much farther than the poor man’s Land Rover

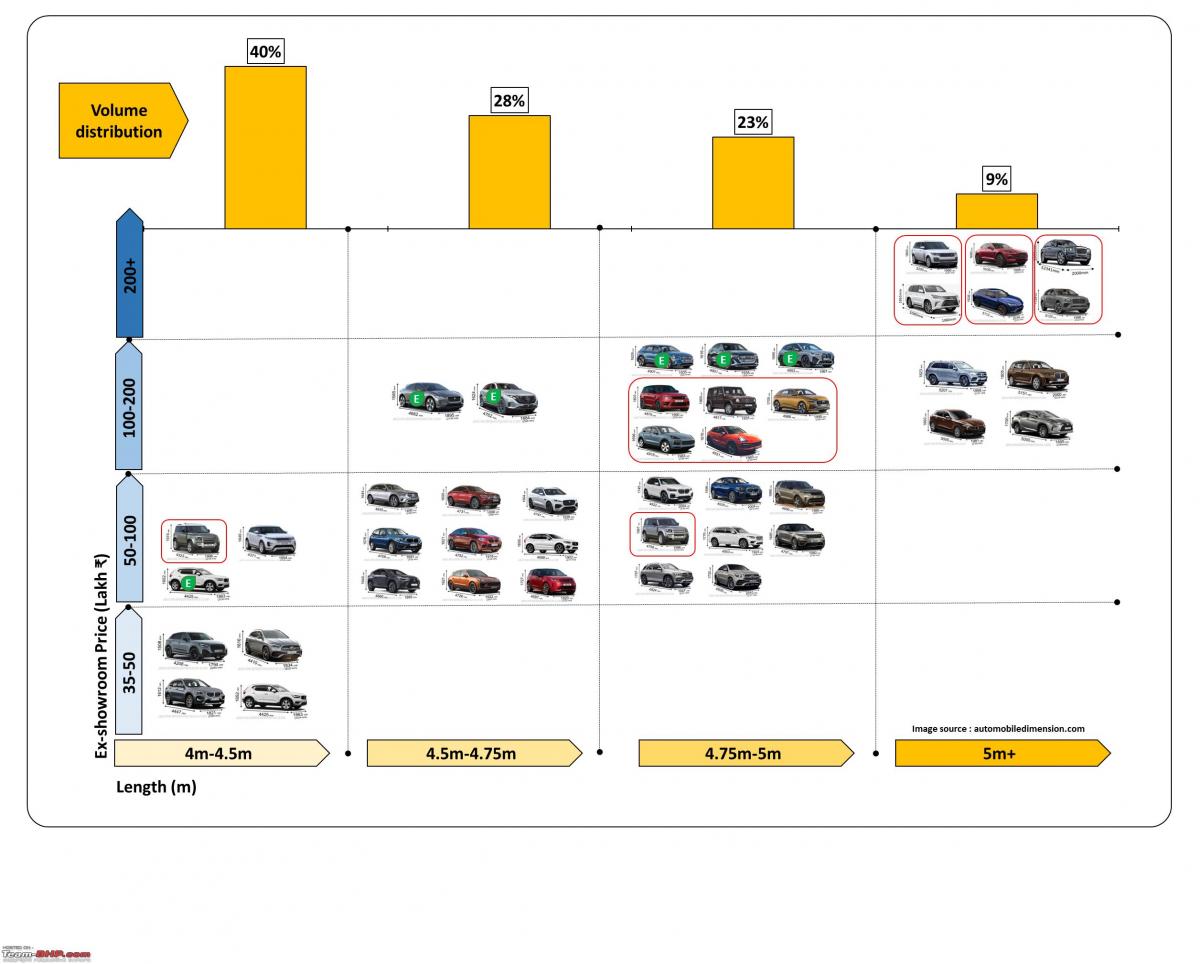

SUV segment

SUV segments are a little trickier than the sedan segments, so viewer discretion is advised. Many products seem to be a misfit in a particular quadrant. Here one thing needs to be understood, this is product classification and not the segmentation approach used in marketing. In marketing, the end-user is segmented and products are designed to meet the needs of that end-user segment. For example, look at the top right quadrant, each group of product in the red box represent a different customer segment – Lamborghini Urus or Aston Matin DBX will appeal to rich kids and Bentley Bentayga or Rolls Royce Cullinan to their rich dad.

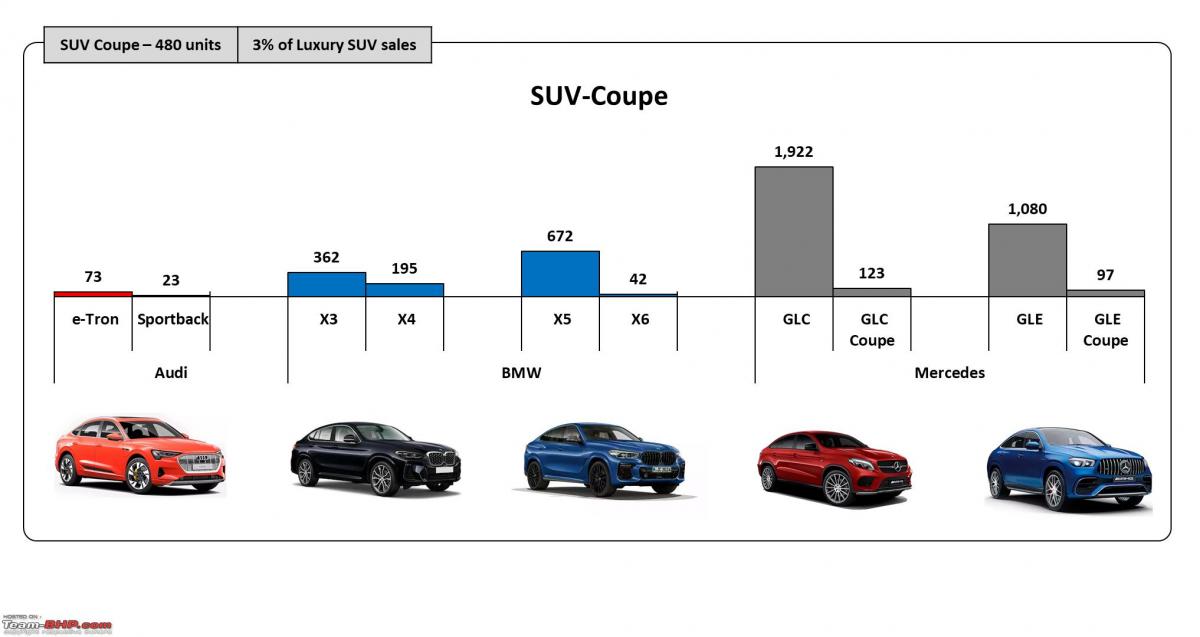

SUV Coupe

BMW X6 is credited to start this segment globally in 2008. SUV coupe, available only in luxury car segment, is catching up in India as well. All SUV coupe numbers put together commands 3% market share of luxury SUV category with considerable 408 units. This is significant, considering all SUV coupe price range starts over ₹ 70 lakhs.

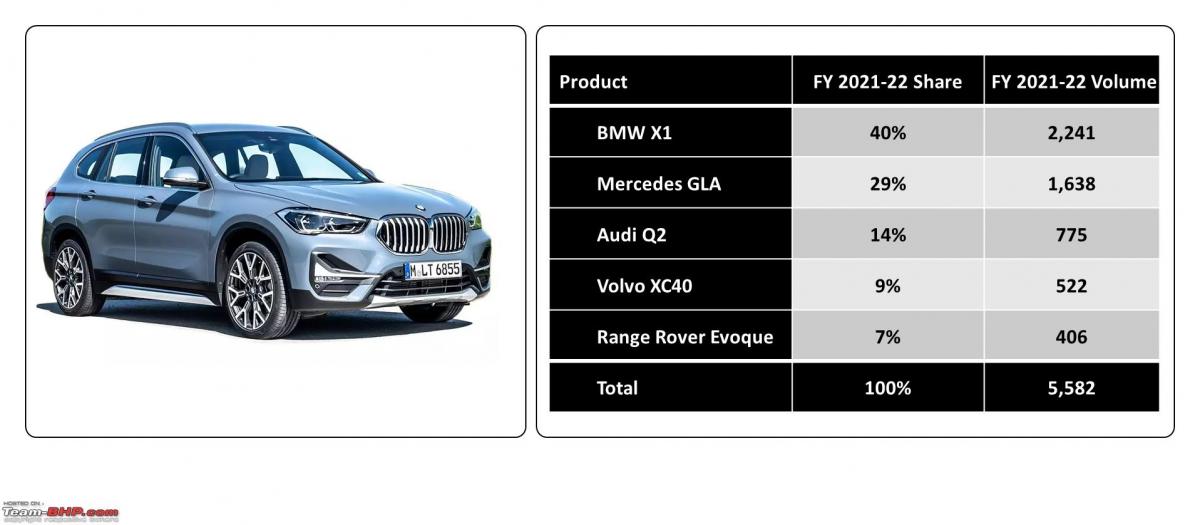

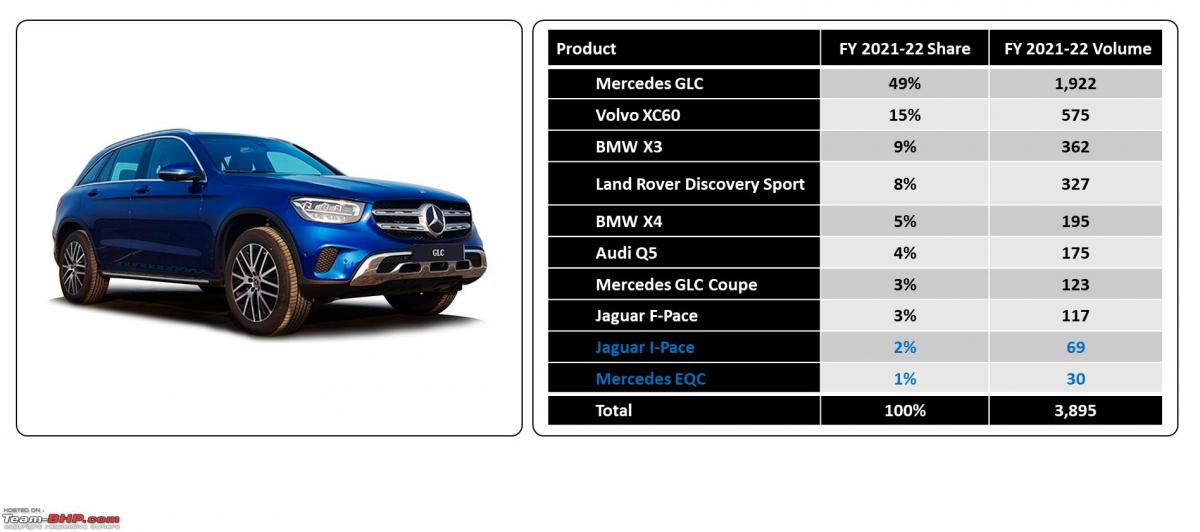

SUV sub-segment

- X1 has best exterior stance, so is selling well despite interiors age GLA stance and price is not helping to grab higher sales

- But GLA pricing did help BMW to jack up X1 prices in recent time

- CBU Q2 seems to be stop-gap arrangement for Audi

- XC40 is available in fully equipped single petrol variant, thus limits its appeal

- Range Rover Evoque sales number seems quite good despite being the most expensive car in the segment

- GLC is doing phenomenally well with 50% segment share

- Volvo’s best-selling car in India is also holding quite well in company of worthy competitors

- BMW seems to be lost in the segment

- Being entry level product in Land Rover world, Land Rover Discovery Sport always did well

- Audi Q5 was introduced quite late in the year, so needs time to catch up

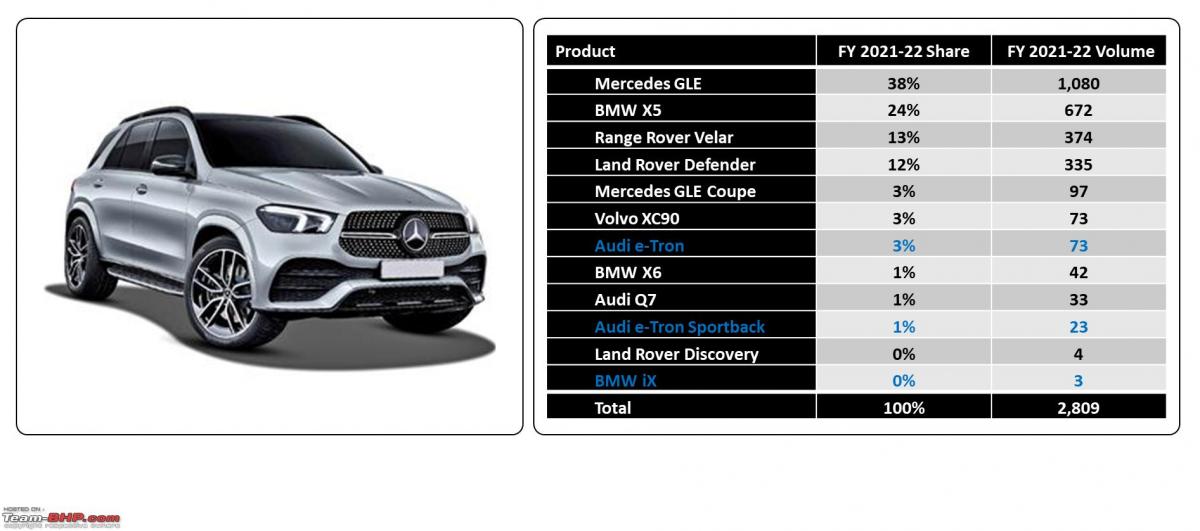

- Introduced in 2020, GLE is holding lead position quite well

- X5 has to play second fiddle again despite being quite a competitive package

- Range Rover Velar’s sleek design makes it quite a luxury accessory in the segment

- Audi Q7 is restarting new journey with petrol only engine that too quite late in the year

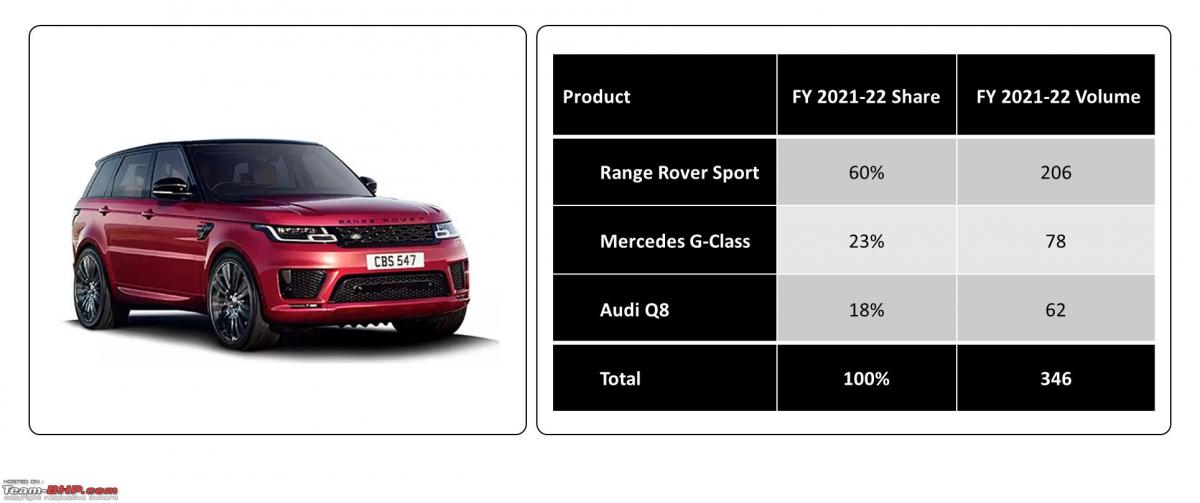

- This is quite a unique segment in itself appealing different audience

- Range Rover Sport is doing well with 60% share

- G-Class numbers looks good given the price tag it carries

- CBU Audi Q8 is neither here nor there kind of product in Indian market

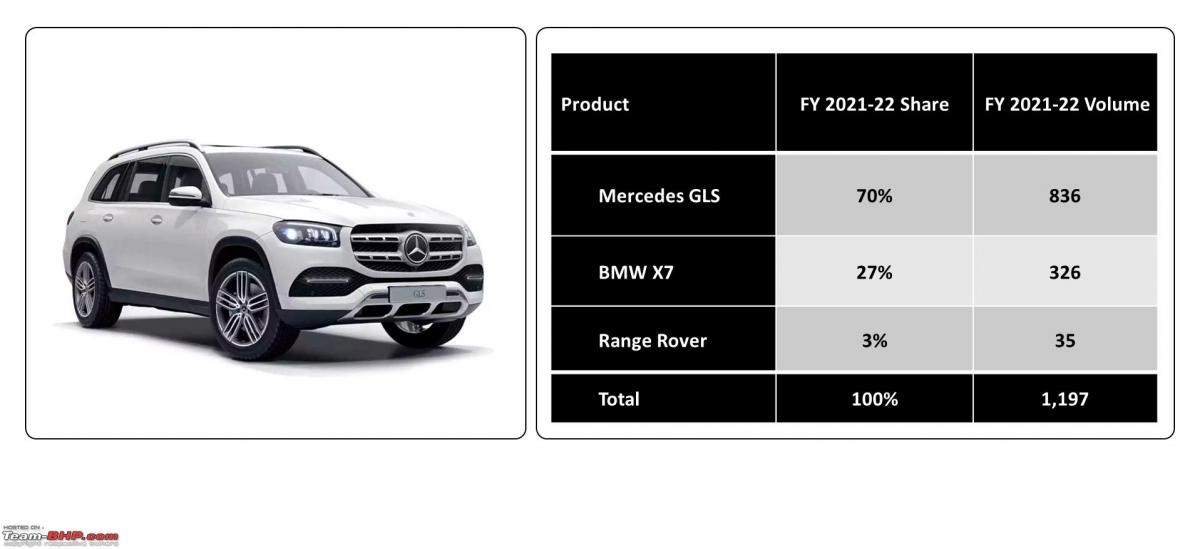

- GLS numbers are too good in the segment

- Seems BMW is not doing something good with competent X7

- Range Rover numbers seems little low

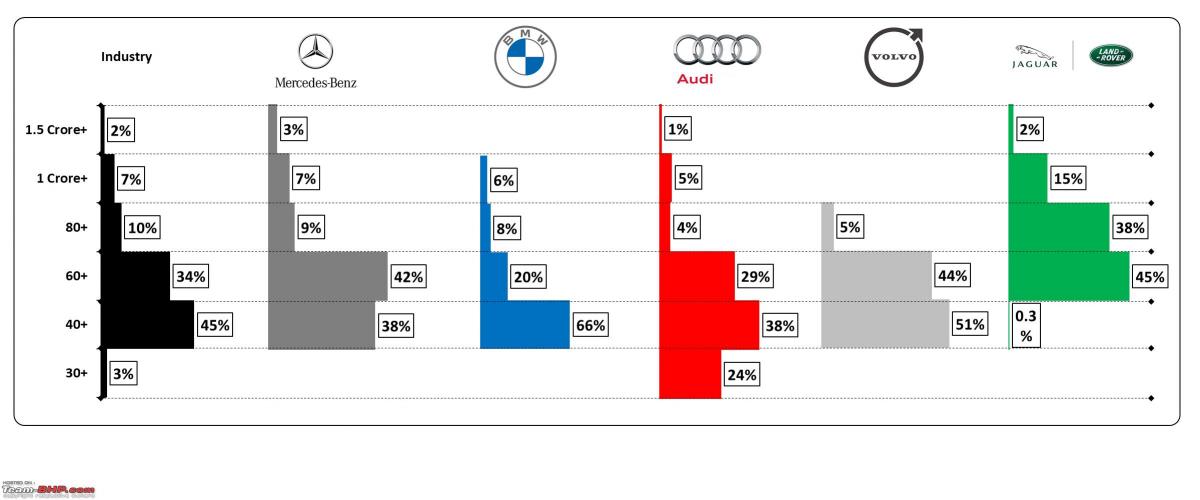

Volume distribution across Ex-showroom price range

This graph may seem little complex to understand, but it gives insight about brands positioning and purchasing power of Indian customer.

- For industry 80% sales comes from cars priced between ₹40 lakhs to ₹80 lakhs

- Volume tapers sharply as prices goes up

- Mercedes gets more revenue from higher priced cars

- BMW gets major revenue from lower priced products

- Audi has actually moved down in revenue yield ladder

- Volvo is concentrated in ₹40 lakhs to ₹80 lakhs bracket

- JLR revenue quality is much richer

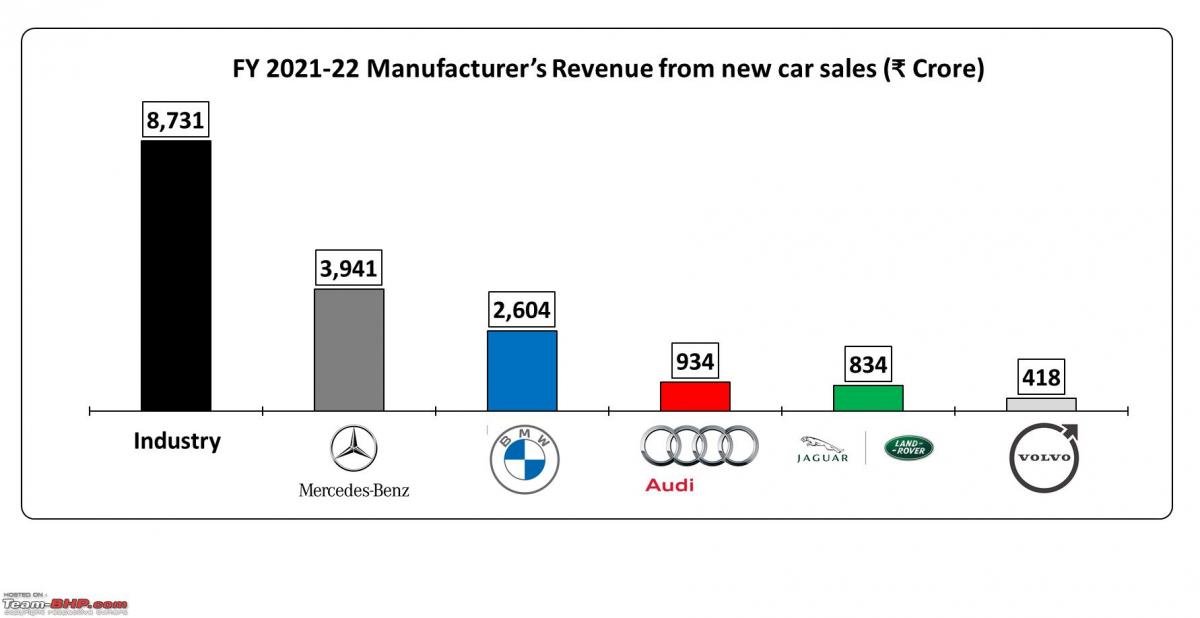

Estimated revenue from new luxury car sales

- Luxury car market generated estimated ₹ 9,000 crores sales from new car sales during recovery phase

- Higher volumes and higher priced range cars means higher revenue for Mercedes

- High value JLR product sales brings its revenue collection closer to Audi

- Volvo is doing decently well in terms of revenue

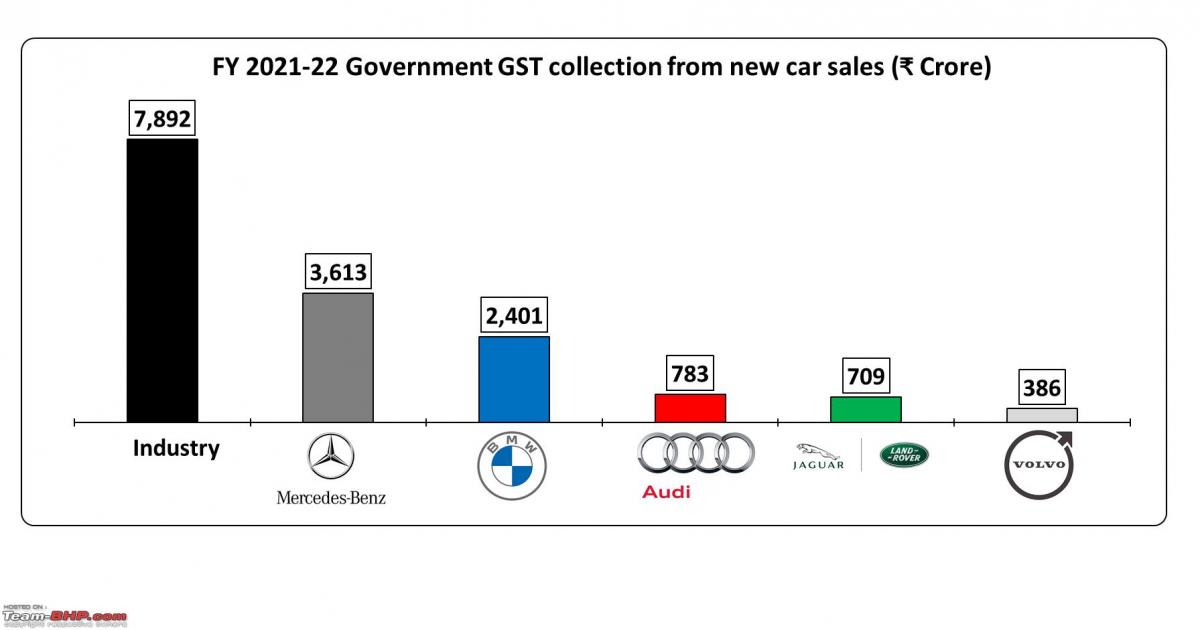

Estimated GST collection from new luxury car sales

- Overall GST contribution is estimated around ₹ 8,000 crores from new car sales

- Despite low volume, luxury cars contribute higher GST in value terms owing to higher price of luxury cars

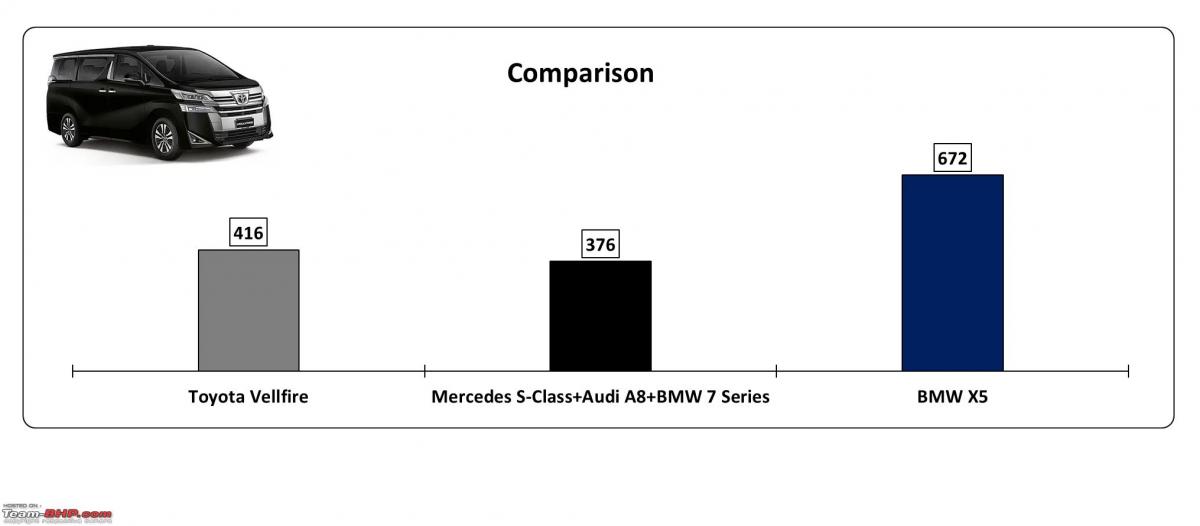

Comparison with interesting twist and turns

Toyota Vellfire

All imported Toyota Vellfire is priced over ₹ 90 lakhs ex-showroom and still sell in quite a large numbers. This speak a lot about premium imagery ‘T’ brand has and how phenomenal product is. This strange comparison shows how well Vellfire is selling, with BMW X5 is priced in similar price territory and the volume it is doing and volume most luxurious large luxury sedans together doing. Toyota now you tasted water, it is time to consider CKD assembly in India and sell even more Vellfire.

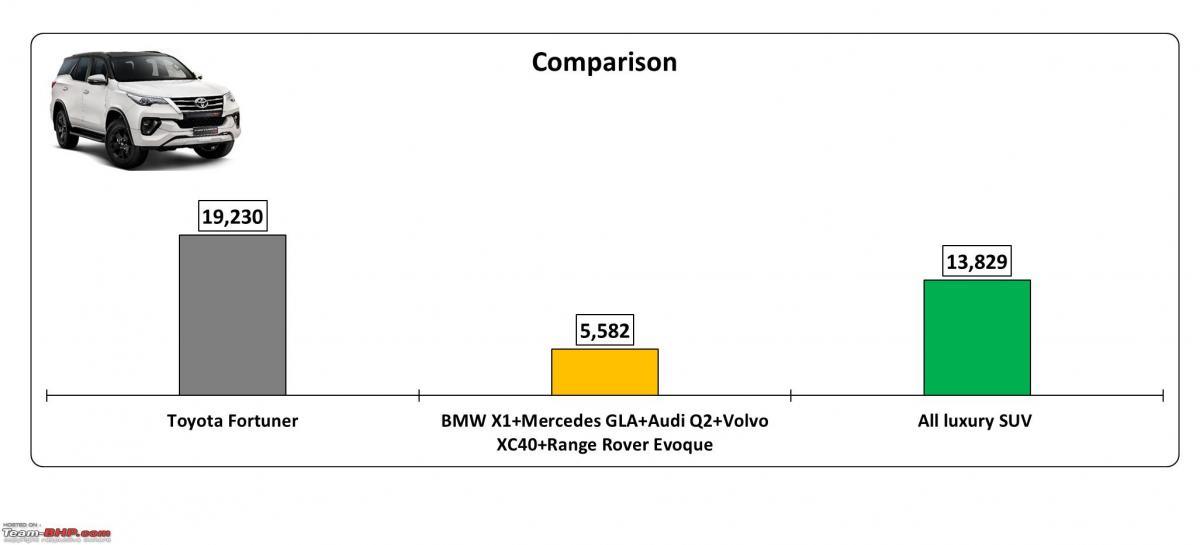

Toyota Fortuner

Toyota Fortuner now priced in territory of ₹34 to ₹48 lakhs (diesel 98% mix) is selling four times over than entire entry level luxury SUV put together. Indian market could be challenging for marketers for market sizing exercise.

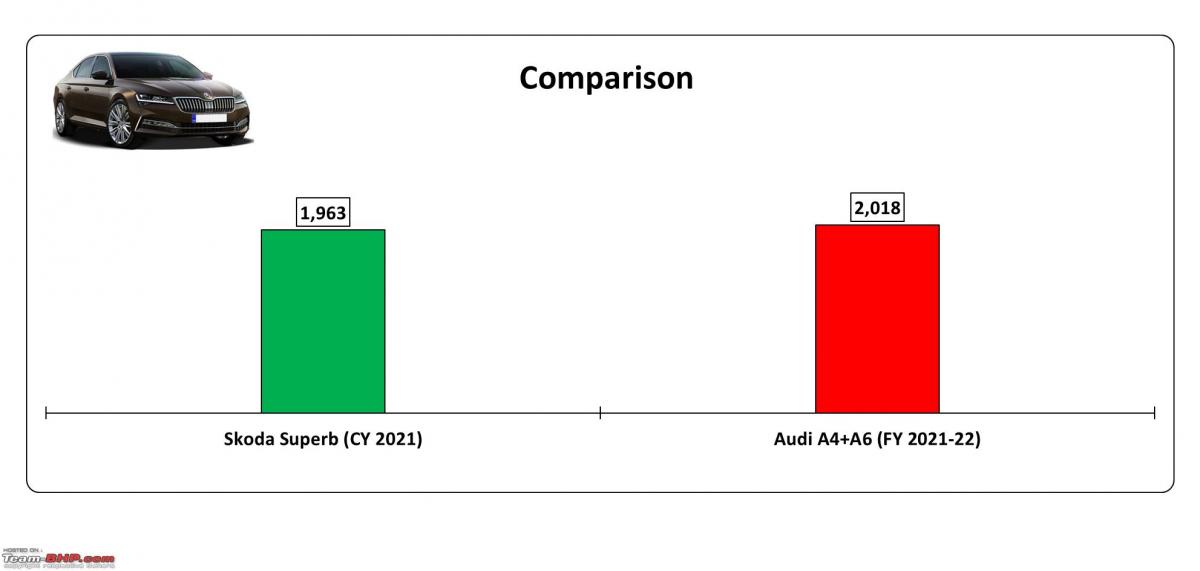

Skoda Superb

Skoda has nearly sold as many Superb as Audi A4 and A6 put together. It shows how well Superb is doing in this segment, despite being 6 years old and how underprepared Audi is with their products. Seems Audi need to borrow people from Sister Brand Skoda.

Read BHPian comments for more insights and information.

Find Car News

Just News

About Us

Buy & Sell

USED CARS